(Source: Shutterstock.com)

[Editor's note: A version of this story appears in the December 2020 edition of Midstream Business. Subscribe to the magazine here.]

Midstream is arguably a volume-driven business. More production means more volumes moving through pipelines, more natural gas and NGL to be processed, and more demand for new or expanded infrastructure. Growing volumes of oil, natural gas and NGL have underwritten significant growth in midstream over the last several years, prompting a massive investment in the buildout of infrastructure.

But does volume growth actually matter for midstream/MLP equity performance? Maybe not. To be clear, production volumes can impact cash flow expectations and fundamentals for companies, but as has been demonstrated in midstream, equities do not always trade on fundamentals.

Ties That Don’t Bind

The U.S. Energy Information Administration (EIA) is forecasting that U.S. oil and natural gas production will decline in 2021 on average. Though volumes are expected to see improvement in second-half 2021, production levels would still be well below the highs from the end of 2019, based on EIA estimates. The expectation for declining production in the near term is often cited as a headwind for midstream and a reason for investor caution.

While declining production can lead to pipeline overcapacity in some areas, fewer growth opportunities for certain types of assets and heightened recontracting risk as long-term agreements eventually expire, it does not necessarily lead to weak equity performance.

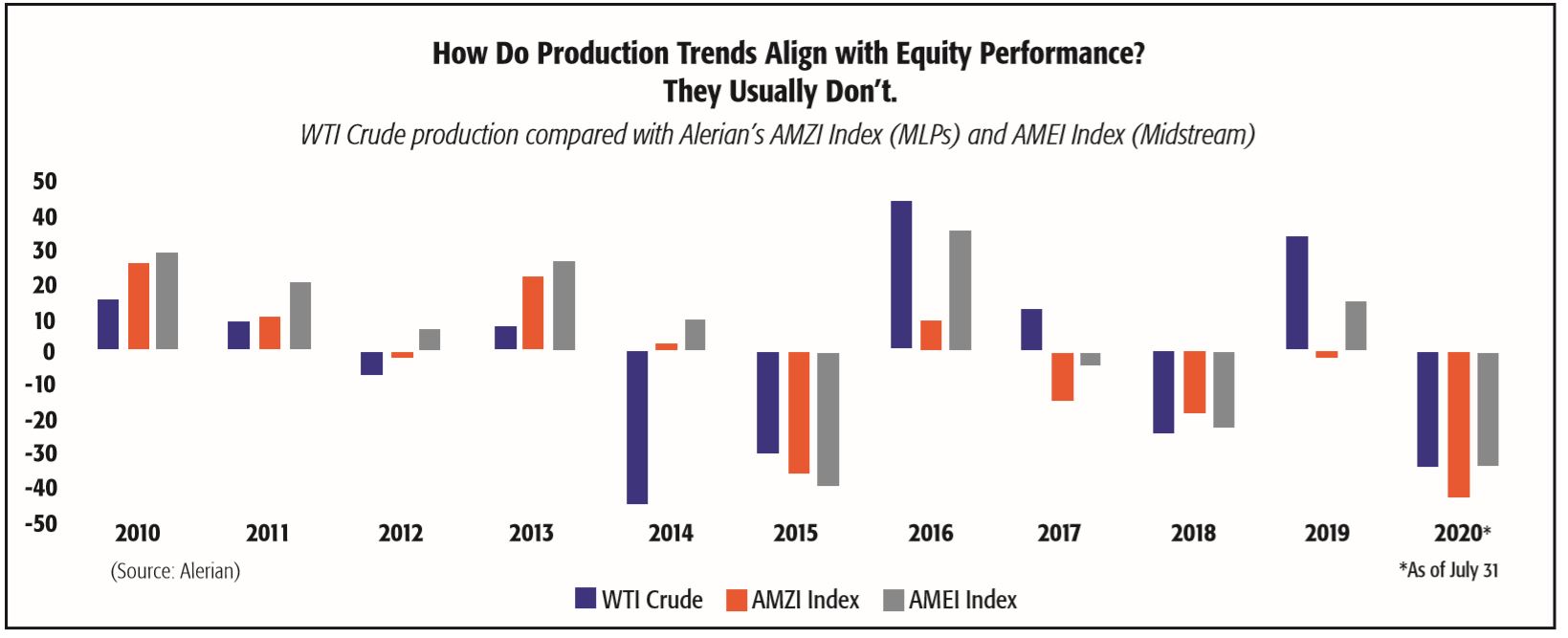

To evaluate the importance, or lack thereof, of production trends for equity performance, the chart looks at annual price performance for WTI crude oil, the Alerian MLP Infrastructure Index (AMZI) and the Alerian Midstream Energy Select Index (AMEI) compared to the annual change in U.S. oil and gas production.

On the surface, declining production would seem negative for midstream, but based on recent history, production trends in either direction do not seem to make much difference for midstream equity performance. For additional context, over the more than 10-year period shown in the chart, the correlation between AMEI performance and U.S. oil production is less than 0.2, and the correlation between AMZI performance and oil production is negative. For context, the correlations for the AMEI and AMZI over the same period with oil prices were approximately 0.5.

From 2017 up until the onset of COVID-19, fundamentals for midstream were strong with significant production growth over this time period and several new infrastructure projects crossing the finish line, adding steady cash flows for companies. Despite positive fundamentals, equity price performance remained weak over the same time period for the AMZI and the AMEI, with the exception of a 14.6% gain for AMEI in 2019.

Distribution cuts, the FERC policy change from March 2018, commodity price volatility, negative energy sentiment and other noise all contributed to weak equity performance despite very constructive production trends. If production growth was not a meaningful tailwind for stocks before, why should declining production in the near term be a material headwind, especially if it could be constructive for oil prices?

In fact, the last year of positive price performance for MLPs and the best annual performance for the AMEI was back in 2016 when oil and gas production fell but oil prices rebounded by 45%. Recall, oil reached a relative bottom in February 2016 of $26/bbl before recovering through the rest of the year.

Thus far, 2020 is looking like 2015 with weakness in crude prices and midstream/MLP stocks. Performance for 2014 reflects the initial resilience of midstream in the early innings of oil’s price decline, but macro headwinds ultimately weighed on midstream performance in 2015 similar to 2020.

Could 2021 look like 2016 with production declines but solid midstream equity performance? One notable advantage for midstream in 2021 relative to 2016 is the meaningful free cash flow companies are expected to generate next year—not to mention other positive changes made in recent years such as eliminations of incentive distribution rights by MLPs, the shift to equity self-funding and balance sheet improvements.

Why it’s A Good Thing

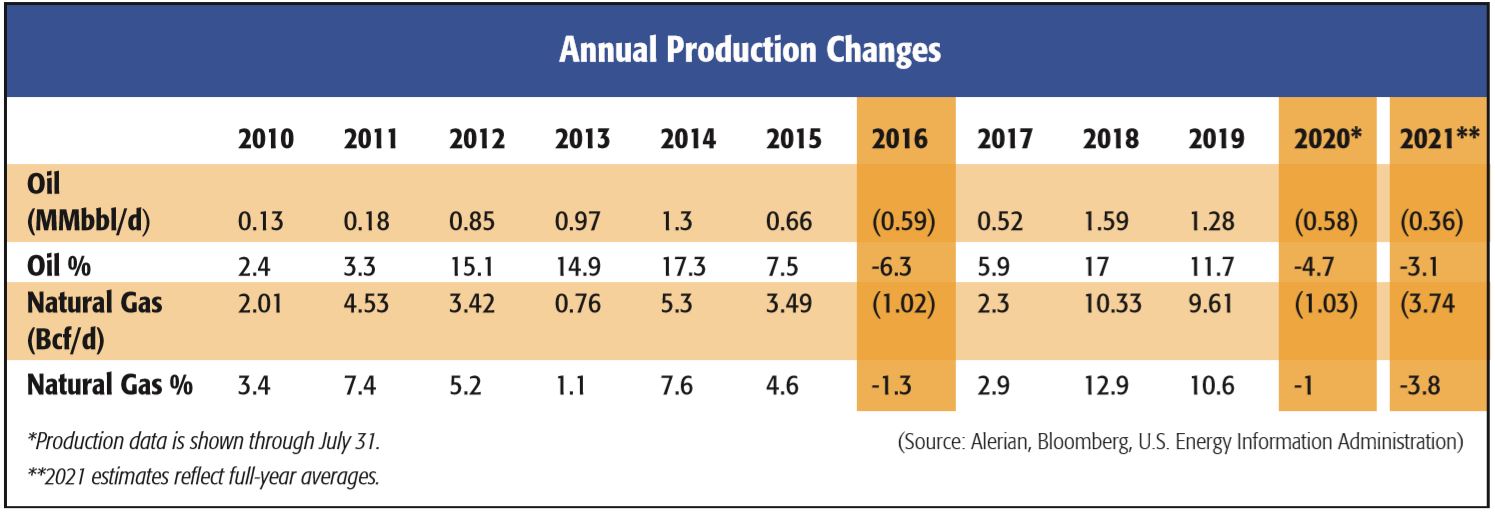

Setting aside the demand shock of COVID-19, U.S. oil production growth in recent years has more or less kept a lid on global oil prices. In 2018 WTI reached a relative peak of $76/ bbl on Oct. 3, but demand concerns and overwhelming U.S. production contributed to a 41% price decline into year-end, with WTI closing 2018 at just $45/bbl. U.S. oil production grew by a hefty 1.6 MMbbl/d on average for the year, which was not helpful for global oil prices or midstream equity performance.

With ongoing headwinds and lessons learned from the past, U.S. producers are more focused on returns than growth alone, with the most disciplined pledging to not grow production by more than a certain percentage even in a higher oil price environment.

In the presentation discussing the merger of Devon Energy Corp. and WPX Energy Inc., management indicated that the combined company would limit production growth to 5% in any year, even in a higher price environment.

Pioneer Natural Resources Co. has discussed 5% plus production growth for the next several years, but management specified on its second-quarter 2020 call that the company’s production growth would not change even if oil reached $60 or $70/bbl.

Talk is cheap, and religion is easily adopted in challenging times. That said, producer discipline could be very constructive for an oil price recovery. Clearly, much depends on improving demand and progress with a COVID-19 vaccine. Perhaps in this recovery, U.S. oil production will not overshoot to the detriment of prices.

So what?

In the near term, U.S. oil production declines could help to restore the balance in global oil markets, which was derailed by the demand destruction resulting from COVID-19. Given a higher correlation between midstream performance and oil prices than production trends, an oil price recovery would likely be more constructive for midstream equities than volume growth.

Recent years have demonstrated that significant volume growth on its own is not enough to support midstream equity performance. A recovery in U.S. oil and natural gas production and return to growth would be constructive for midstream beyond 2021, but that growth will require higher prices, which near-term production declines and producer discipline can help support. In other words, production declines are a necessary step toward an energy market recovery and could actually be good for midstream in the near term.

Stacey Morris is director of research with Alerian.

Recommended Reading

Analyst: Is Jerry Jones Making a Run to Take Comstock Private?

2024-09-20 - After buying more than 13.4 million Comstock shares in August, analysts wonder if Dallas Cowboys owner Jerry Jones might split the tackles and run downhill toward a go-private buyout of the Haynesville Shale gas producer.

The ABCs of ABS: Financing Technique Shows Flexibility and Promise

2024-07-29 - As the number of ABS deals has grown, so have investors’ confidence with the asset and the types of deals they are willing to underwrite.

Solaris Stock Jumps 40% On $200MM Acquisition of Distributed Power Provider

2024-07-11 - With the acquisition of distributed power provider Mobile Energy Rentals, oilfield services player Solaris sees opportunity to grow in industries outside of the oil patch—data centers, in particular.

Archrock Offers Common Stock to Help Pay for TOPS Transaction

2024-07-23 - Archrock, which agreed to buy Total Operations and Production Services (TOPS) in a cash-and-stock transaction, said it will offer 11 million shares of its common stock at $21 per share.

The ABCs of ABS: Financing Technique Shows Flexibility and Promise

2024-07-29 - As the number of ABS deals has grown, so have investors’ confidence with the asset and the types of deals they are willing to underwrite.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.