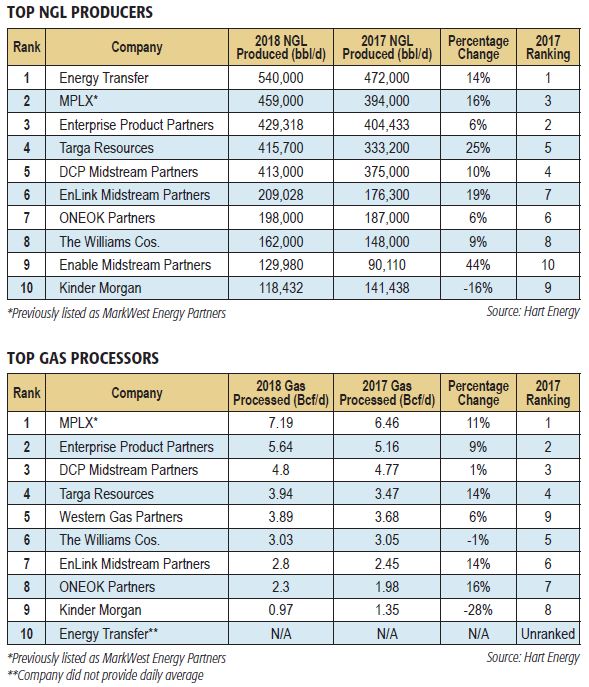

For the first time in three years, the top spots in Midstream Business’ annual rankings of the top gas processors and NGL producers have remained the same. Energy Transfer Partners retained its spot as the top NGL producer while MPLX’s gathering and processing segment (previously known as MarkWest Energy Partners) was once again the top gas processor in our rankings.

Hart Energy has made every reasonable effort to ensure the veracity of this information. Neither Hart Energy, Midstream Business nor parties involved in gathering and presenting this material will be held liable for any errors or emissions.

One-two punch

There was a great deal of volume growth from ranked companies, including those at the top of the lists. Energy Transfer’s NGL production rose by 14% to 540,000 barrels per day (Mbbl/d) for 2018. Energy Transfer also reported large increases in the amount of gathered natural gas within its system, which were due to ramped-up production out of the Permian, Northeast, and North Texas.

In fact, it’s likely that these increases pushed Energy Transfer into the top two in our natural gas processor rankings. However, the company did not supply processing figures. The company earned a ranking in our top- 10 processor rankings based on its gathering volumes and gas processing net capacity—but without specific figures we placed it tenth.

Energy Transfer’s biggest splash this year was the $5 billion acquisition of Tulsa, Okla.-based SemGroup Corp. This deal increases the company’s crude oil assets and enhances its NGL assets in the Denver-Julesburg and Anadarko basins, including several pipelines that will connect these regions to the Cushing, Okla., crude oil hub.

The Mariner East system is also a focal point for the continued growth of Energy Transfer, according to the company’s CFO, Thomas Long. “Since resuming operations on Mariner East 1 in late April, the combined Mariner East pipeline system has moved approximately 230 Mbbl/d of NGLs through Marcus Hook [Pa.] and we expect that volume to continue to ramp up when Mariner East 2X comes online later this year,” he said during the company’s recent conference call to discuss second-quarter earnings.

Between pipeline, truck and rail, Energy Transfer is moving about 300 Mbbl/d of NGLs through Marcus Hook.

The company with the biggest year-over-year NGL production growth was Enable Midstream Partners, which rose 44% to 129.9 Mbbl/d to go along with record volumes of natural gas gathered and processed, as well as record amounts of crude and condensate gathered. These results were driven by continued producer activity and strong well results.

Top processing spot

“2018 was a transformational year for MPLX,” Gary Heminger, the company’s chair and CEO, said during a recent earnings call. “In the gathering and processing segment, we added 11 new plants, which expanded our processing capacity by nearly 1.5 Bcf/d [billion cubic feet per day] and our fractionation capacity by 100 Mbbl/d.”

For the 2018 fiscal year, MPLX’s gathering and processing segment reported a 15% increase in earnings to $1.4 billion. This was largely driven by record levels of natural gas volumes gathered, processed and fractionated. The growth in processed volumes came out of the Marcellus Shale.

Heminger added that MPLX will focus on expanding its midstream assets through organic growth in order to further generate third-party revenue. MPLX anticipates adding about 800 million cubic feet per day (MMcf/d) of natural gas processing capacity and 100 Mbbl/d of fractionation capacity in 2019.

MPLX reported significant growth in processed volumes in the first-half of 2019, with a 15% increase to 7.8 Bcf/d in the second quarter, compared to the same time in 2018. Once again, the bulk of these volumes are due to growth in the Marcellus.

ONEOK surges

ONEOK Partners had the biggest increase on the gas processing side with a 16% year-over-year increase to 2.3 Bcf/d in 2018, due to greater producer activity in the Rockies and the Midcontinent.

“We continued to see strong producer activity and efficiency improvements across the Williston Basin and Powder River Basin, which is driving associated natural gas and NGL growth. NGL volume gathered on the Bakken Pipeline in 2018 increased 4% compared with 2017. Fourth-quarter NGL volumes gathered averaged 148,000 barrels per day, a 7% increase compared with the third-quarter 2018,” Kevin Burdick, ONEOK’s executive vice president and COO, told analysts in a recent earnings call.

These figures are expected to continue to increase, based on the number of capital growth projects in place for this year and next. ONEOK anticipates spending more than $4.4 billion in 2019 through the first quarter of 2020.

ONEOK anticipates a strong opening for several new assets in the Williston, which has more than 250 MMcf/d of natural gas currently being flared on its dedicated acreage in the region. Company officials expect the 200 MMcf/d Demicks Lake I natural gas processing plant to open full when it comes online in the fourth quarter. Another 200 MMcf/d plant, Demicks Lake II, is expected to be complete in the first quarter of 2020.

In the Rockies, well connections exceeded expectations in 2018 and are expected to be even higher during 2019.

ONEOK also reported increased activity out of its acreage in the Midcontinent for the 2018 calendar year. Natural gas processed through the company’s plants rose by more than 18% from the previous year, following the connecting of 138 wells.

Processed volumes should further increase in 2019 as the company completed the expansion of its Canadian Valley natural gas processing plant in the Stack play. This plant increased ONEOK’s processing capacity in Oklahoma about 1.1 Bcf/d.

“In our gathering and processing segment, we expect natural gas volumes processed to increase approximately 5% compared with 2018, primarily from growth in the Williston Basin. Additionally, with our Demicks Lake I plant coming online in the fourth quarter, we expect our 2019 exit rate for volumes processed in the Williston Basin to be approximately 20% higher than our current processed volume level,” Burdick added.

DCP down, up

One note of significant import is DCP Midstream Partners reaching its lowest place in our rankings in over a decade. From 2007 to 2015, DCP held the top spot in both of our rankings. Despite experiencing a 10% increase to 413 Mbbl/d of NGL produced, the company fell to No. 5 in top NGL producer rankings. It retained the No. 3 spot in the gas processor rankings after processed volumes rose 1% to 4.8 Bcf/d.

Since the downturn in oil and gas prices, the company altered its business model to reduce its sensitivity to commodity prices. The DCP 2.0 strategy, now in its fourth year, is focused on using technology to drive optimization and improve efficiencies throughout DCP Midstream’s portfolio of assets. These assets are located in some of the most prolific plays in the country, including the Permian Basin, Eagle Ford Shale, Scoop, and the D-J Basin. The D-J Basin in particular has been a standout play for the company this year as it experienced a double-digit year-over-year volume growth in the second quarter.

By the middle of 2020, the company anticipates having a total of nearly 1.7 Bcf/d of processing capacity in the D-J Basin. A large chunk of this new capacity results from the recently completed O’Connor 2 processing plant, which has a total capacity of 300 MMcf/d.

DCP officials also announced that the company is increasing NGL takeaway capacity on the Southern Hills Pipeline by 40 Mbbl/d, which will increase the system’s total capacity by about 20% to 230 Mbbl/d by the end of 2020.

While the company is in transition, one thing that remains the same is its commitment to its highly concentrated super-system strategy that allows the company to maximize its assets. By providing customers with multiple options in a single region, DCP ensures highly reliable services with minimum down time, it says.

The super-system strategy also makes for higher reliability when it comes to financials and investments.

“Looking at our overall portfolio growth, the vast majority of our investments are focused on fee-based logistics assets and combined with our existing premier footprint we are well-positioned to achieve our long-term strategic goals while also solving for needed capacity additions in these top tier regions,” said Wouter van Kempen, chairman, president and CEO.

Pushing boundaries

For much of DCP’s run at the top of our rankings, Enterprise Products Partners paced it for those top spots. However, Enterprise has remained remarkably consistent in its growth patterns. In fact, the only companies that have surpassed Enterprise in our rankings have been Energy Transfer and MPLX, which have both had unparalleled growth in their gas processing and NGL production operations.

What’s impressive about Enterprise’s figures is that the company has kept up with both of those companies while also changing its focus from a traditional midstream operator to, in many ways, being the segment’s trailblazer.

Enterprise has been one of the leaders at changing the definition of what a midstream company is by embracing all forms of oil and gas transportation, not just pipelines. The company was also at the forefront of the push towards exporting U.S. crude, NGL and gas

It’s hard to argue with the company’s strategy as it continues to regularly shatter internal records. In the fourth quarter of 2018 alone, Enterprise reported it broke eight operational financial records. These included liquid pipeline, gas pipeline and propylene production volumes.

According to Jim Teague, CEO of Enterprise, a big part of the company’s success with exports has been supply access for its terminals.

“Enterprise’s supply position coupled with our Houston-area storage and distribution network offers unmatched connectivity and supply aggregation,” he said during the company’s fourth quarter 2018 earnings call earlier this year.

Enterprise is one of the frontrunners in providing midstream services to petrochemical companies.

“We continue to write the book on midstream services to the petrochemical industry, which is growing faster on the Gulf Coast than any place in the world,” Teague added.

While the company has been helping to expand the definition of midstream services, Enterprise continues to invest heavily in traditional midstream assets. Nowhere is this more evident than in the Permian Basin, where Enterprise has committed more than $6 billion in capital growth projects.

These projects include gas processing and gathering systems, crude storage, as well as crude, liquids and gas takeaway. New projects include two new NGL fractionators at the big Mont Belvieu, Texas, NGL hub to handle production out of the Permian. Once these capital projects are completed in 2020, Enterprise will have more than 1.5 Bcf/d of gas processing capacity and more than 250 Mbbl/d of liquids production in the Permian.

Targa quietly growing

One company that has been quietly moving up our annual rankings for years is Targa Resources, which posted a 25% gain in NGL production to 415.7 Mbbl/d and a 14% increase in gas processing to 3.94 Bcf/d in 2018.

“Targa is in a special unique position. [We have] a franchise Permian gathering and processing position and diversity from other strong gathering and processing positions,” Joe Bob Perkins, Targa’s CEO, said during its fourth-quarter 2018 earnings call.

He added that Targa is one of the only integrated midstream operators that can boast a combination of strong gathering and processing, NGL transportation, Mont Belvieu fractionation, NGL exports, and other premium downstream markets. Perkins stated that this combination puts the company on a path to achieve greater growth than its peers, along with rapid deleveraging and dividend coverage improvement.

Outlook: more of the same

Inevitably, the top NGL producers and gas processor rankings will look much different in a decade, but it’s hard to see large changes in the immediate future. Energy Transfer and MPLX have such sizable leads over the companies behind them in the rankings that it’s unlikely either will be knocked out of the top spot in each category in the next year.

It is safe to say that we’re likely to see the top processors and producers still on this list in some form or another, but the forecast gets murkier the further out you look with potential headwinds and tailwinds that could alter production and demand levels. Many companies are also in the midst of new strategy plans and developing assets in areas that are expected to experience production growth.

_________________________________________________________________________________________________________________________________

Frank Nieto is a freelance writer based in Washington, D.C., with more than a decade of experience covering the energy industry.

Recommended Reading

Gulfport Energy to Offer $500MM Senior Notes Due 2029

2024-09-03 - Gulfport Energy Corp. also commenced a tender offer to purchase for cash its 8.0% senior notes due 2026.

ONEOK Offers $7B in Notes to Fund EnLink, Medallion Midstream Deals

2024-09-11 - ONEOK intends to use the proceeds to fund its previously announced acquisition of Global Infrastructure Partners’ interest in midstream companies EnLink and Medallion.

Kosmos to Repay Debt with $500MM Senior Notes Offer

2024-09-11 - Kosmos Energy’s offering will be used to fund a portion of its 7.125% senior notes due 2026, 7.750% senior notes due 2027 and 7.500% senior notes due 2028.

Upstream, Midstream Dividends Declared in the Week of July 8, 2024

2024-07-11 - Here is a selection of upstream and midstream dividends declared in the week of July 8.

Solaris Stock Jumps 40% On $200MM Acquisition of Distributed Power Provider

2024-07-11 - With the acquisition of distributed power provider Mobile Energy Rentals, oilfield services player Solaris sees opportunity to grow in industries outside of the oil patch—data centers, in particular.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.