Annual development spending by upstream oil and gas companies needs to rise to about $600 billion through the next decade, analysts say. (Source: Shutterstock.com)

With oil and gas demand set to continue growing during the next decade, companies will need to step up spending, according to an energy consulting firm.

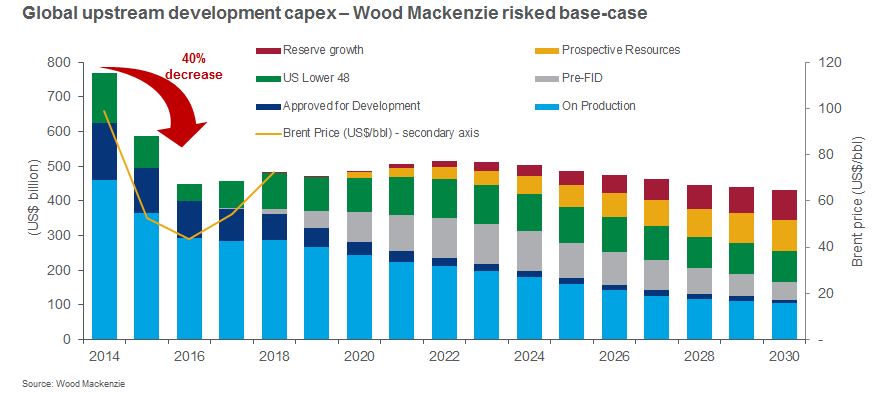

Wood Mackenzie says upstream oil and gas companies must invest 20% more to meet the world’s future energy needs. Annual development spending needs to rise to about $600 billion through the next decade.

That could prove a difficult task for some holding onto cash with not-too-distant memories of plunging oil prices, shelved projects, massive layoffs and other cuts. Additionally, companies are facing pressure today to use excess cash flow—thanks to improved market conditions and efficiency—for other purposes, including returning it to shareholders.

“Four years of deep capital rationing have had a severe impact on resource renewal, especially in the conventional sector,” Tom Ellacott, senior vice president of corporate research for Wood Mackenzie, said in a news release.

The firm pointed out that spend is rebounding post downturn but said sustainability is an issue.

“Not enough new high-quality projects are entering the funnel to replace those that have left,” Ellacott added.

The comments were shared as oil and gas companies kicked off their third-quarter earnings release season, sharing details on financial performance and operational highlights with some giving a peek into upcoming spending plans.

U.S. independent ConocoPhillips Co. (NYSE: COP), which has positions in the Bakken, Delaware Basin and Eagle Ford along with international assets, slightly increased its capital guidance for 2018 by $100 million to $6.1 billion due to partner-operated spend. Executives said its 2019 capital plan, which is set for release in December, will be roughly in line with this year’s.

Maintaining financial discipline remains a focus for ConocoPhillips and many other energy companies even as cash flows rise amid improved oil prices.

Equinor ASA (NYSE: EQNR), which reported this week third-quarter adjusted earnings jumped to $4.8 billion from about $2.3 billion a year earlier, slashed its 2018 budget by about 9% to $10 billion.

“Many companies will justifiably be concerned about committing substantial capital to long-term projects with peak oil demand and energy transition risks within the investment horizon,” Ellacott said. “There’s also a prevailing mindset of austerity designed to appease shareholders—investment is lower in the pecking order for surplus cash flow than dividends and buybacks.”

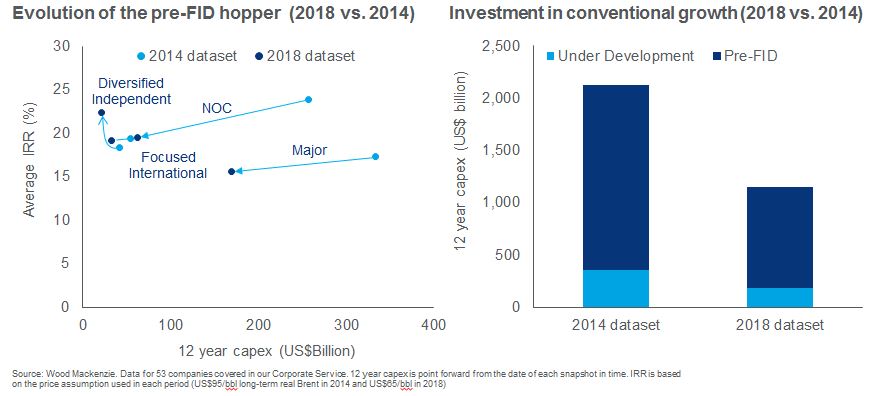

But conventional reserves have taken a hit since the market downturn.

“Global pre-FID [final investment decision] conventional reserves now only cover two years of global oil and gas production,” Wood Mackenzie said.

Investment has picked up as market conditions have improved as evidenced by a growing number of project sanctions in 2018—including the $8.3 billion Equinor-operated Bay du Nord project in the Flemish Basin offshore Newfoundland in the Atlantic Ocean. Near-term investment has also picked up in U.S. shale plays with a bevy of LNG projects from Australia, Canada, Mozambique, Papua New Guinea and the U.S. in the works.

Still, recent gains aren’t expected to be enough to meet post-2025 oil and gas demand, the firm said, noting investment in conventional, deep water, oil sands and U.S. shale gas remain below pre-downturn levels. The only area where consistent growth is foreseen in the near-term is U.S. tight oil.

Wood Mackenzie estimates development spending will rise 5% this year, following a 2% increase in 2017. Overall, investment is expected to grow to more than $500 billion in early 2020s, up from a low of $460 billion in 2016.

More exploration spending that will hopefully lead to big commercial discoveries and better economics, particularly for conventional projects, are needed, according to Wood Mackenzie.

“Around half of the reserves in our pre-FID project dataset need oil prices above US$60 per barrel to achieve a 15% return—in this disciplined world many companies are screening new projects on long-term oil prices well below spot,” the firm said. “Further progress in project re-scoping, digitalization and better fiscal terms will all need to play their part in getting these projects over the line.”

Velda Addison can be reached at vaddison@hartenergy.com.

Recommended Reading

Gulfport Upsizes Debt Offering to $650 Million

2024-09-04 - Gulfport Energy plans to raise $650 million in new senior notes to repurchase existing debts maturing in 2026.

Post Oak-backed Quantent Closes Haynesville Deal in North Louisiana

2024-09-09 - Quantent Energy Partners’ initial Haynesville Shale acquisition comes as Post Oak Energy Capital closes an equity commitment for the E&P.

Upstream, Midstream Dividends Declared in the Week of July 8, 2024

2024-07-11 - Here is a selection of upstream and midstream dividends declared in the week of July 8.

BPX’s Koontz: The Rise of a Shale Man

2024-07-02 - CEO Kyle Koontz takes the reins of BPX Energy’s rapid onshore growth amid big changes at BP.

Dividends Declared in the Week of Aug. 19

2024-08-23 - As second-quarter earnings wrap up, here is a selection of dividends declared in the energy industry.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.