TC Energy said that after a two-year strategic review, the $36 billion company would best serve stockholders by spinning off its liquids pipelines business into a standalone publicly traded company. (Source: Shutterstock.com)

Canada’s TC Energy Corp. said July 27 its board has approved plans to split TC Energy into separate, publicly listed companies with one focused on natural gas transmission and the other on liquids.

The decision comes as a result of a two-year strategic review by the $36 billion company. TC Energy said it anticipates completing the transaction on a tax-free basis by the second half of 2024.

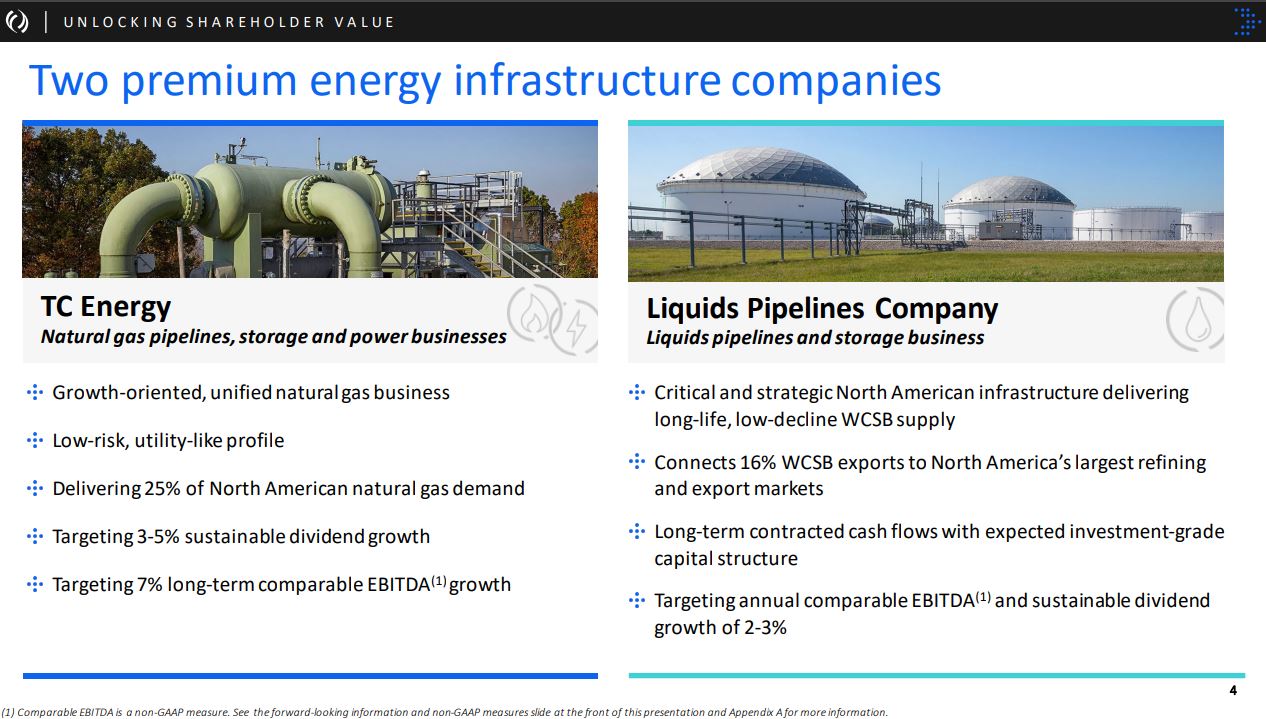

Once completed, the spinoff would result in two high-quality, focused energy companies.

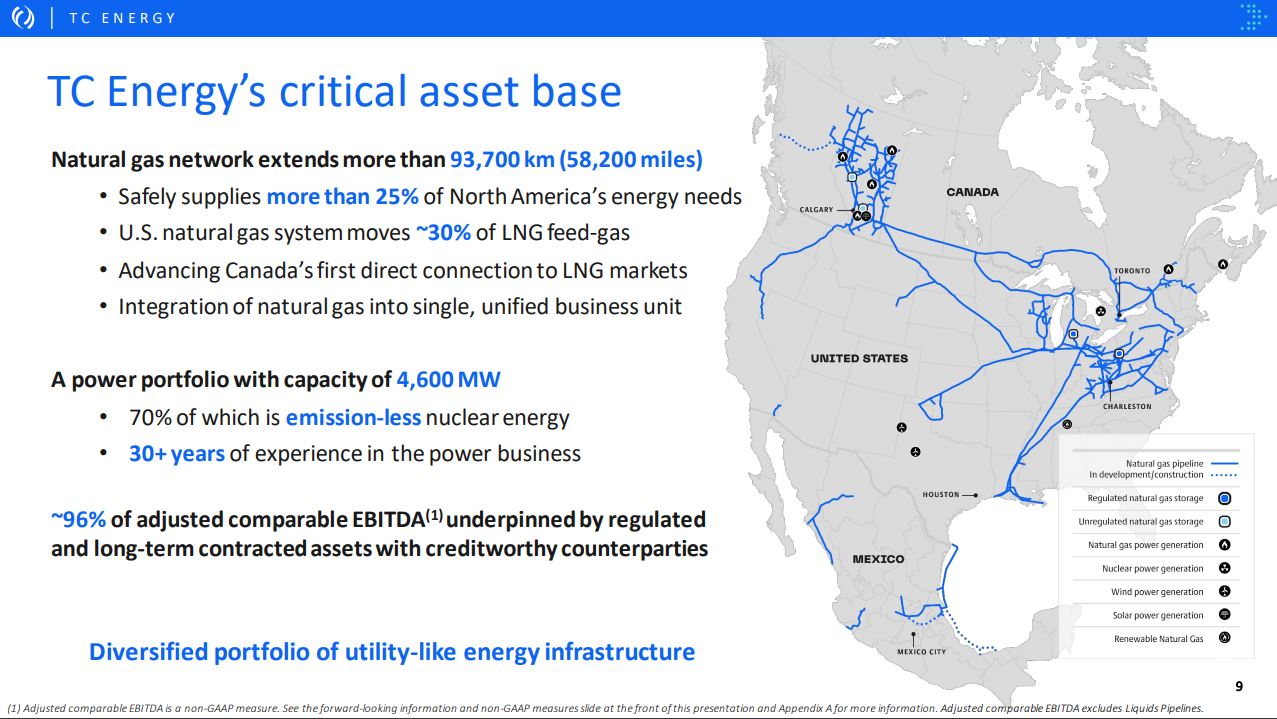

The move would create one company focused on natural gas and power and energy solutions. That portion of TC Energy’s business generated comparable 2022 EBITDA of CA$8.5 billion, which is expected to grow at a 7% CAGR through 2026.

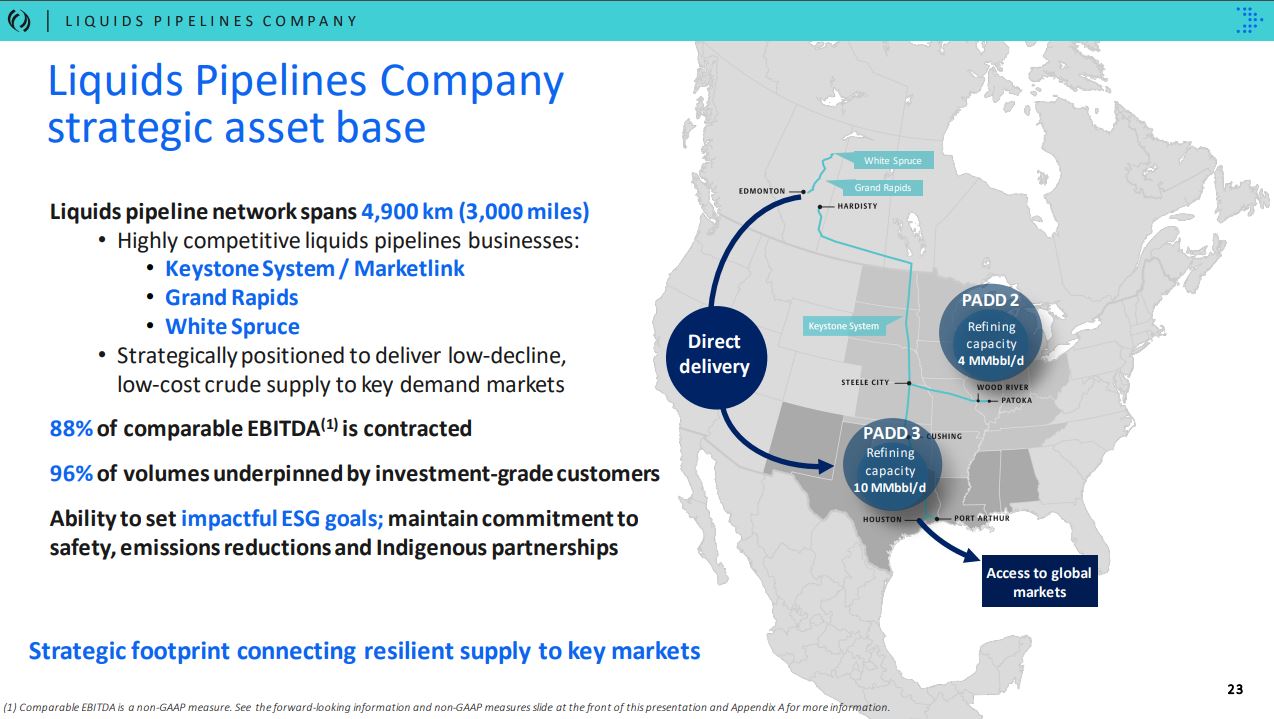

The liquids pipeline business would focus on strategic assets that serve high-demand markets in North America. For 2022, that business generated a comparable 2022 EBITDA of CA$1.4 billion, which is expected to grow at a 2% to 3% compound annual growth rate through 2026.

The company said the spinoff will unlock shareholder value by providing both companies with the flexibility to pursue their own growth objectives through disciplined capital allocation, enhancing efficiencies and driving operational excellence.

“This transformative announcement sets us up to deliver superior shareholder value for the next decade and beyond,” said François Poirier, TC Energy’s president and CEO. “Fundamentals have always driven our strategic direction, and as a result, we have grown into a premier energy company with incumbency across a wide range of energy infrastructure platforms. As we have become the partner of choice for a magnitude of accretive, high-quality opportunities, we have determined that as two separate companies we can better execute on these distinct opportunity sets to unlock shareholder value.”

The announcement comes after TC Energy on July 24 said it would sell a 40% interest in its Columbia Gas Transmission and Columbia Gulf Transmission pipelines in a deal with Global Infrastructure Partners (GIP) for $3.9 billion.

Under the terms of the proposed transaction, TC Energy shareholders would retain their current ownership in TC Energy’s common shares and receive a pro-rata allocation of common shares in the new liquids pipelines company.

The transaction is expected to be tax-free for TC Energy’s Canadian and U.S. shareholders. The determination of the number of common shares in the new Liquids Pipelines Company to be distributed to TC Energy shareholders will be determined prior to the closing of the proposed transaction.

TC Energy expects to seek shareholder approval of the transaction at a meeting of shareholders in mid-2024. In addition to TC Energy shareholder and court approvals, the transaction is subject to receipt of favorable tax rulings from Canadian and U.S. tax authorities, receipt of necessary regulatory approvals and satisfaction of other customary closing conditions. TC Energy expects that the Transaction will be completed in the second half of 2024.

Recommended Reading

PrairieSky Adds $6.4MM in Mannville Royalty Interests, Reduces Debt

2024-04-23 - PrairieSky Royalty said the acquisition was funded with excess earnings from the CA$83 million (US$60.75 million) generated from operations.

JMR Services, A-Plus P&A to Merge Companies

2024-03-05 - The combined organization will operate under JMR Services and aims to become the largest pure-play plug and abandonment company in the nation.

New Fortress Energy Sells Two Power Plants to Puerto Rico

2024-03-18 - New Fortress Energy sold two power plants to the Puerto Rico Electric Power Authority to provide cleaner and lower cost energy to the island.

Kimmeridge Fast Forwards on SilverBow with Takeover Bid

2024-03-13 - Investment firm Kimmeridge Energy Management, which first asked for additional SilverBow Resources board seats, has followed up with a buyout offer. A deal would make a nearly 1 Bcfe/d Eagle Ford pureplay.

SilverBow Rejects Kimmeridge’s Latest Offer, ‘Sets the Record Straight’

2024-03-28 - In a letter to SilverBow shareholders, the E&P said Kimmeridge’s offer “substantially undervalues SilverBow” and that Kimmeridge’s own South Texas gas asset values are “overstated.”