The Double E pipeline is set to deliver gas to the Waha Hub before the Matterhorn Express pipeline provides sorely needed takeaway capacity, an analyst said. (Source: Shutterstock.com/ Summit Midstream)

Summit Midstream Partners announced an open season for capacity on its Double E Pipeline, a currently underutilized transport that will play a key role in the Permian Basin’s future, an analyst said.

The open season commenced April 1 and closes at 2 p.m. Central Time on April 29.

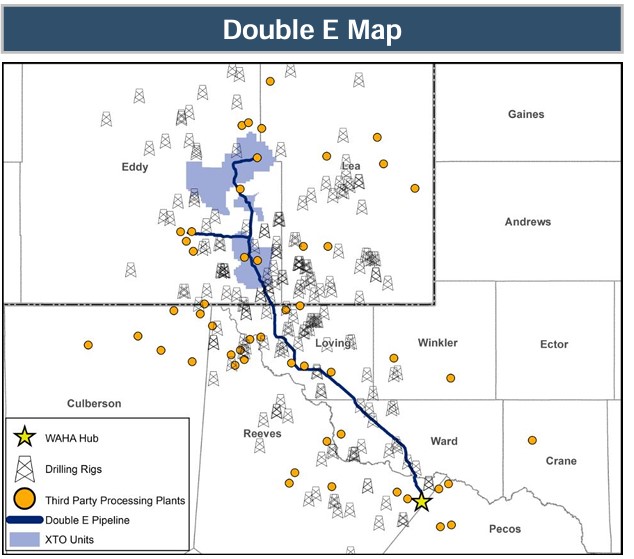

Double E begins at the Summit Lane gas processing plant in New Mexico and terminates about 135 miles away at the Waha Hub near Pecos, Texas.

Recently, gas has been so plentiful at the Waha Hub that spot prices have dipped into negative territory.

However, that should change once Matterhorn begins to take gas away from the Waha Hub sometime later this year.

“It will be important for Double E to be able to deliver more gas into Waha and other points before Matterhorn starts up next quarter,” Jack Weixel, senior director of East Daley Analytics, wrote in an email to Hart Energy. “I think the idea is that Matterhorn will take away 2 Bcf/d of gas from Waha, so there will be more space at Waha to deliver gas into.”

Double E is soliciting non-binding bids for the firm transportation service rate schedule of Double E’s tariff, according to the press release from Summit Midstream.

“Double E is an interesting pipe,” Weixel said. “It is currently severely underutilized.”

According to East Daley’s tracking numbers, during the last quarter of 2023 the line carried an average 386 MMcf/d. The line’s capacity is 1.35 Bcf/d. Weixel said the line will receive some incremental volumes of about 300 MMcf/d from the EOG Resources' Janus plant by second-quarter 2025, but still has much more room to carry gas.

Meanwhile, gas producers in the Permian are anxious for the opening of the Matterhorn Express.

“The market has been eagerly waiting on Matterhorn because capacity out of the Permian is so tight,” Weixel said. “It’s so tight that even the slightest disruption to outbound capacity results in negative prices.”

Last month, two maintenance periods on two lines — Kinder Morgan’s Permian Highway and El Paso’s North Mainline — caused the Waha Hub price to dip into the negatives twice.

From April into May, maintenance on the jointly-owned Gulf Coast Express pipeline is expected to lower Waha prices again.

“All of these maintenance events effectively cut capacity out of the basin, bottle up supply and send prices tumbling,” Weixel said. “Matterhorn is super important to relieve this condition and Double E wants to take advantage.”

The Permian is second to the Marcellus/Utica Basin in U.S. gas production. However, while the Appalachian basins are gas-focused, natural gas from the Permian is a byproduct of crude oil production called associated gas.

Permian gas production is consequently driven by the price of crude, rather than the price of gas, which nationally has been under $2 per MMbtu since February.

Recommended Reading

Enbridge Announces $500MM Investment in Gulf Coast Facilities

2024-03-06 - Enbridge’s 2024 budget will go primarily towards crude export and storage, advancing plans that see continued growth in power generated by natural gas.

Enbridge Fortifies Dominant Role in Corpus Christi Crude Transport

2024-03-20 - Colin Gruending, Enbridge executive vice president and president for liquids pipelines told Hart Energy the company’s holdings in South Texas are akin to a “catcher’s mitt” for Permian and Haynesville production.

Enbridge Sells Off NGL Pipeline, Assets to Pembina for $2.9B

2024-04-01 - With its deal to buy Enbridge’s NGL assets closed, Canada's Pembina Pipeline raised EBITDA guidance for 2024.

Early Startup of Trans Mountain Pipeline Expansion Surprises Analysts

2024-04-04 - Analysts had expected the Trans Mountain Pipeline expansion to commence operations in June but the company said the system will begin shipping crude on May 1.

Enterprise’s SPOT Deepwater Port Struggles for Customers

2024-04-25 - Years of regulatory delays, a loss of commercial backers and slowing U.S. shale production has Enterprise Products Partners’ Sea Port Oil Terminal and rival projects without secured customers, energy industry executives say.