Transocean’s Deepwater Atlas, an eight-generation ultra-deepwater drillship capable of 20,000 (20K) psi operations. (Source: Transocean)

Even as operators tighten budgets, they are earmarking funds for deepwater, ultra-deepwater and frontier drilling.

According to Rystad Energy research, operators are expected to be quite active on the drilling front in 2024. Frontier regions in particular are fueling optimism for drilling activities in 2024, particularly deepwater projects in the Atlantic Margin, Eastern Mediterranean and Asia, Rystad said.

During the company’s Feb. 20 earnings call, Transocean President and COO Keelan Adamson expressed optimism about expected rig contracts for drilling operations in Brazil, the Gulf of Mexico (GoM) and West Africa.

During a Feb. 22 call discussing the company’s fourth-quarter 2023 earnings, TechnipFMC Chairman and CEO Doug Pferdehirt observed that operators are shifting more capital to offshore projects this year.

SLB CEO Olivier Le Peuch, during a January earnings call, said offshore rig counts are rising in response to a strong pipeline of final investment decisions (FIDs) for both shallow and deepwater.

“We think across this wide base load of activity, a significant portion is taking place offshore, where capital expenditure will continue the growth momentum in 2024,” Le Peuch said.

He noted there has been an “explosion” of activity offshore.

“It is broad and it's here, in my opinion, to stay because the economics of offshore have improved significantly over the last couple of cycles,” he said.

Halliburton CEO Jeff Miller said during a January investor call that the company is seeing an increase for 2024 and beyond in “service intensity everywhere we operate—whether it’s longer laterals in North America, smaller and more complex reservoirs in mature fields or offshore deepwater—customers require more services to develop their resources, not fewer.”

Clay Williams, NOV chairman, president and CEO, said during a February earnings call that 2023 saw continuing momentum in offshore and international markets underpinning the steady upcycle that he believes will continue to unfold over the next several years.

Throughout 2023, operators renewed deepwater activity and exploration in places like Namibia and Suriname, along with brownfield developments offshore Norway and West Africa and in the GoM and greenfield developments offshore Brazil, Guyana and Australia, he said.

“There are so many areas that look so strong,” he said.

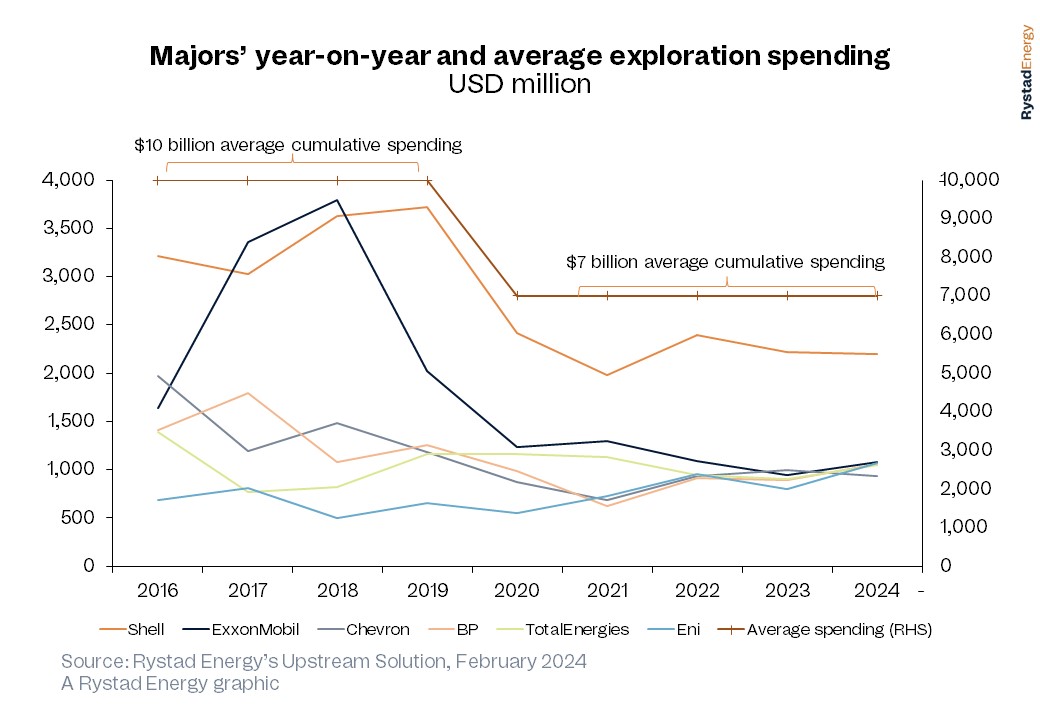

Between 2020 and 2024, Exxon Mobil, Shell, Chevron, BP, TotalEnergies and Eni will have spent on average a combined $7 billion each year, according to Rystad. That is a drop from the previous four-year period, during which average total spending was $10 billion, Rystad said.

Going deeper

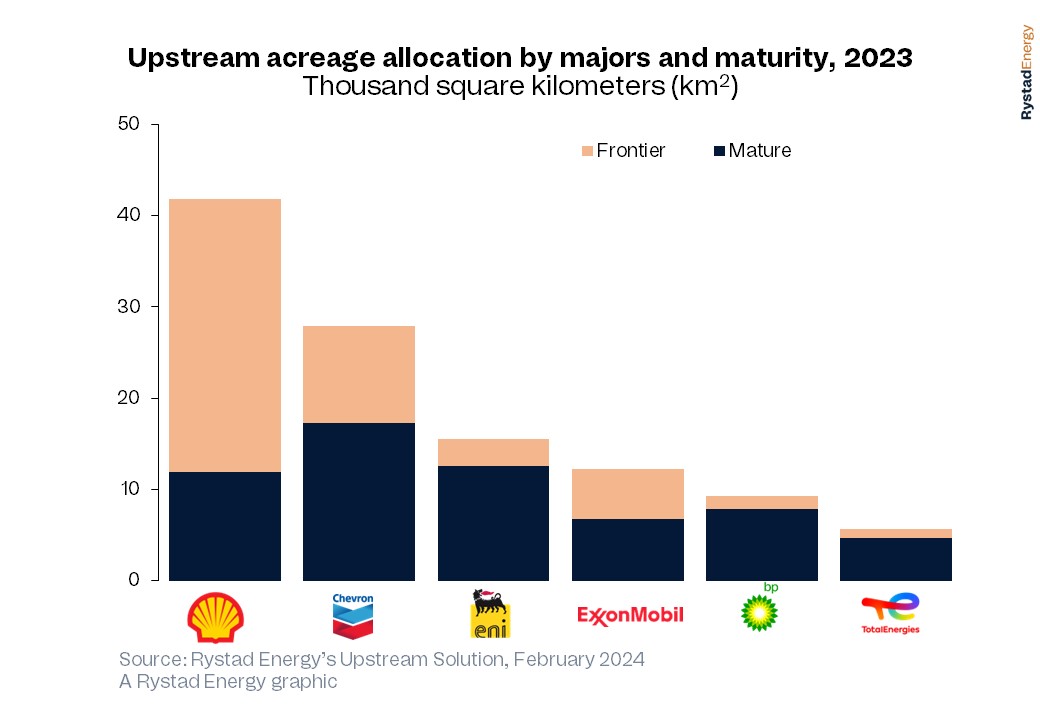

During 2023, 112,000 sq km of offshore acreage was awarded to major players, with 39% of that acreage on the shelf, 28% in deepwater and 33% in ultra-deepwater. The acreage awarded to majors in 2023 was 20% higher than acreage awarded to them in 2022.

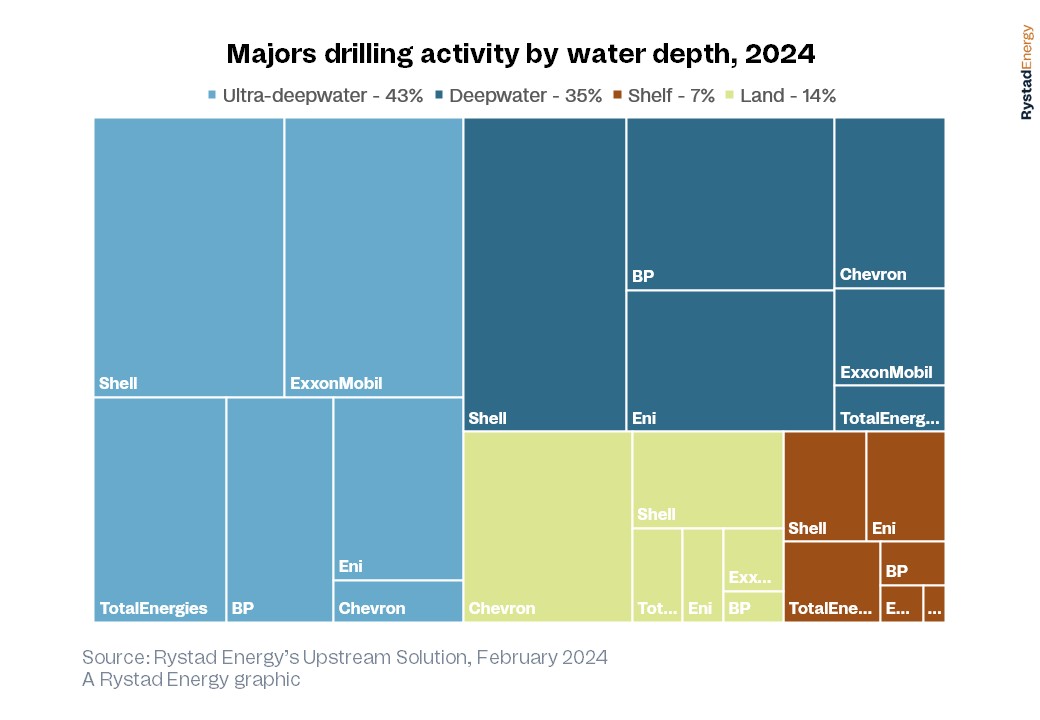

Rystad suggests this trend represents a significant push into deeper waters, and the firm predicts about 50 more deepwater and ultra-deepwater exploratory wells to be drilled in 2024 compared to 2023. About 27% of all offshore exploration wells drilled in 2023 were deepwater or ultra-deepwater, and for 2024, Rystad expects that percentage to rise to around 35%.

Familiar and frontier acreage

Santosh Kumar Budankayala, senior upstream analyst at Rystad, said majors are “cautiously” venturing into deeper waters and re-evaluating their approaches to frontier exploration.

“While we anticipate them to appraise and mature their frontier acreages, we also expect them to continue to focus on familiar territory—regions with established expertise and existing infrastructure that offer quicker monetization with lower risks,” he said in a press release.

Rystad noted that frontier basins generated 45% of 2022’s discoveries, but only 20% of 2023 discoveries. Additionally, the firm said, conventional discoveries dropped in 2023, with majors finding 1 Bboe, compared to 3 Bboe level in 2022.

In the face of that trend, Rystad suggested the future of oil and gas exploration might lie in venturing beyond the familiar into frontier and underexplored basins. Exploration in mature basins typically yields smaller finds that can quickly transition from discovery to start up by using existing infrastructure, while frontier and underexplored areas hold the allure of large, geographically concentrated prospects, the firm said.

Past frontier exploration yielded the discovery of gas in Area 1 and Area 4 off Mozambique between 2010 and 2013, gas finds off the coast of Mauritania and Senegal between 2015 and 2017, the Liza oil discovery in Guyana in 2015 and the Sakarya gas field in Turkey's Black Sea sector in 2020. The Brulpadda and Luiperd discoveries in South Africa in 2019 and 2020 and Venus and Graff in Namibia, both in 2022, have led to the opening of new hydrocarbon plays.

2024 plans

Shell secured 42,000 sq km of frontier acreage offshore Uruguay in 2023. Rystad noted Shell has significant projects in Southeast Asia, Africa and the Americas slated for this year. Currently, Shell is drilling the ultra-deep prospect Pekaka on Block SB 2W offshore Sabah, East Malaysia. This prospect shares similarities with the 2022 Tepat discovery in deepwater Block M and holds substantial potential for a gas-condensate discovery, aligning with Shell's gas-focused portfolio strategy in Malaysia, the firm said.

Following Pekaka, Shell is expected to pursue more ultra-deepwater exploration on Block SB X with the Bijak prospect, Rystad said. Shell secured these blocks in Malaysia’s 2021 bid round. Additionally, exploration drilling is anticipated in the shelf region of Sarawak, East Malaysia. Shell is also continuing appraisal activity in Namibian waters to further prove the extent of its discoveries there, including Graff, Rystad said.

BP’s deepwater exploration plans in Africa and the Americas comprise of multiple wells in Egypt, including appraisal drilling at the Raven gas and condensate field, as well as wildcat exploration drilling in the King Mariout offshore concession in the Western Mediterranean, Rystad said. BP’s Pau-Brazil well marks its first operated well in the Santos Basin off Brazil, expanding its presence beyond the Campos Basin, where it was previously a non-operating partner with Petrobras.

Additionally, Chevron and Shell are collaboratively spearheading plans to drill off the coast of Suriname in Block 42, which contains the Walker carbonate prospect. Rystad said a discovery in Block 42 has the potential to catalyze further exploration efforts in Suriname.

Argerich-1, Argentina’s first offshore ultra-deepwater well, in which Shell has a 30% nonoperating stake, if successful, also could spur deepwater exploration in that region, Rystad said.

Recommended Reading

Chord Buying Enerplus to Create a Bakken Behemoth

2024-02-22 - Chord Energy said Feb. 21 it will acquire Enerplus Corp. for nearly $4 billion in a stock-and-cash deal to potentially create the largest producer in the Williston Basin.

Williston Warriors: Enerplus’ Long Bakken Run Ends in $4B Chord Deal

2024-02-22 - Chord Energy and Enerplus are combining to create an $11 billion Williston Basin operator. The deal ends a long run in the Bakken for Enerplus, which bet on the emerging horizontal shale play in Montana nearly two decades ago.

Ohio Oil, Appalachia Gas Plays Ripe for Consolidation

2024-04-09 - With buyers “starved” for top-tier natural gas assets, Appalachia could become a dealmaking hotspot in the coming years. Operators, analysts and investors are also closely watching what comes out of the ground in the Ohio Utica oil fairway.

Chord, Enerplus’ $4B Deal Clears Antitrust Hurdle Amid FTC Scrutiny

2024-04-08 - Chord Energy and Enerplus Corp.’s $4 billion deal is moving forward as deals by Chesapeake, Exxon Mobil and Chevron experience delays from the Federal Trade Commission’s requests for more information.

EIA: E&P Dealmaking Activity Soars to $234 Billion in ‘23

2024-03-19 - Oil and gas E&Ps spent a collective $234 billion on corporate M&A and asset acquisitions in 2023, the most in more than a decade, the U.S. Energy Information Administration reported.