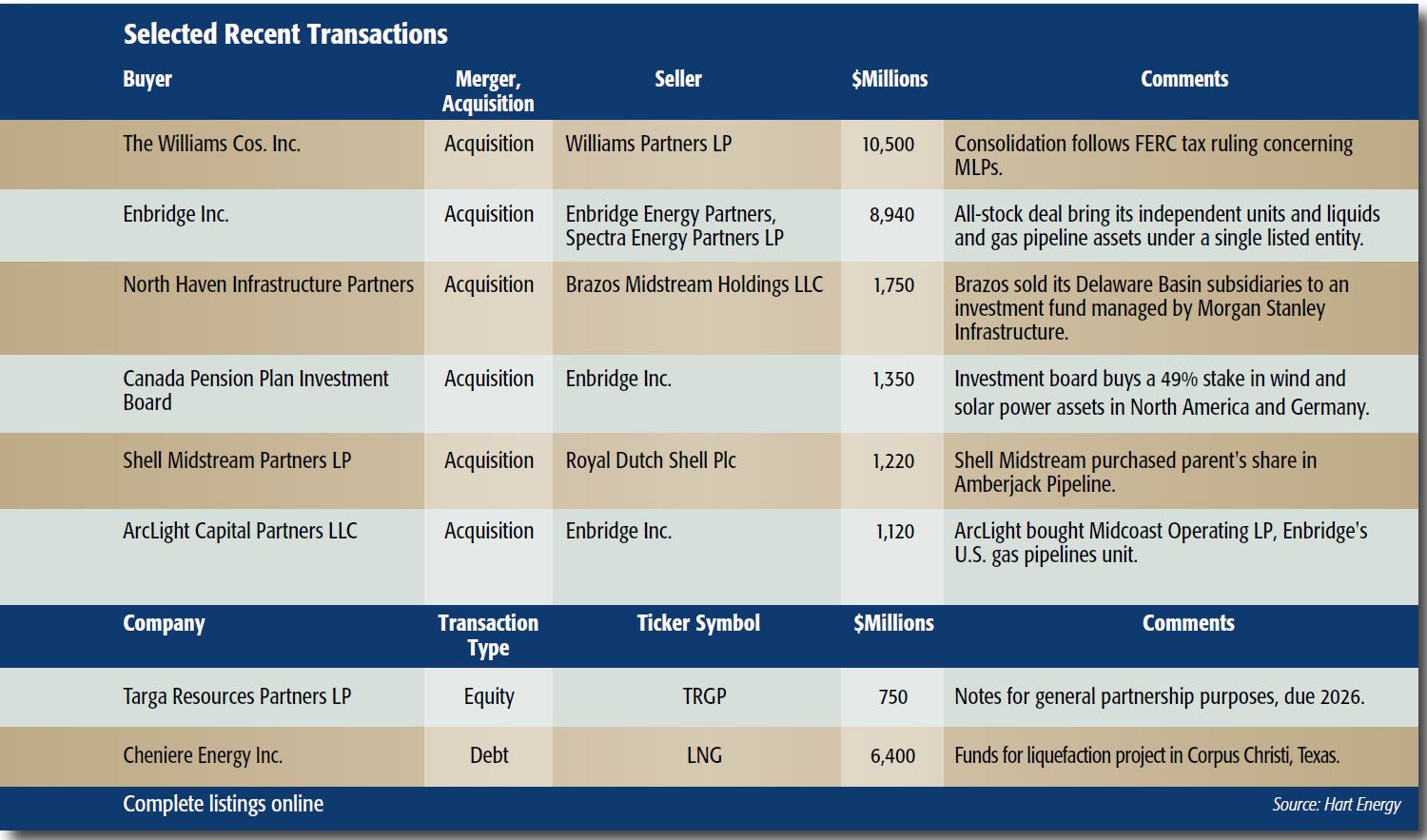

The Federal Energy Regulatory Commission’s (FERC) tax ruling on March 15 removed certain benefits for MLPs. But it is more likely that the decision merely sped up, rather than forced the recent consolidations, of MLPs formed by Enbridge Inc. and The Williams Cos. Inc.

Michael Underhill, chief investment officer of Pewaukee, Wis.-based Capital Innovations LLC, viewed the May announcements by the two midstream majors as part of a continuing trend.

“The FERC ruling accelerated the consolidations,” Underhill said. “When Kinder Morgan departed the MLP space on Aug. 10, 2014, this was viewed as an anomaly—I was quoted as stating that this was a precursor of things to come. Recently, Kinder Morgan was joined by ONEOK Inc. and Targa Resources Corp. as they have bought in their MLPs.”

Enbridge ranks No. 1 on the current Midstream Business Midstream 50 list of the sector’s largest publicly held firms. Williams ranks No. 6.

FERC based its decision on a ruling by the U.S. Court of Appeals for the D.C. Circuit in July 2016. The commission said that the court had ruled that its tax policy constituted a “double recovery” of income tax costs for MLPs and eliminated that benefit.

This doesn’t mean that it makes fiscal sense for all parent companies to dissolve their MLPs, but Underhill added he expects the announcements to force investors to question the validity of the MLP model and re-evaluate the C-corp structure.

Some introspection by the sector may be in order as well.

“The industry itself needs to remain cognizant that minimizing an MLP’s [incentive distribution rights] burden—or lowering its cost of capital in other ways) —and maximizing an MLP’s investor base may be needed to extend an MLP’s lifespan beyond 15 to 20 years,” he said.

Ethan H. Bellamy, senior research analyst with Baird Equity Research, noted the economic advantages that MLPs provide, as opposed to corporations, for qualifying assets outside of cost-of-service-driven interstate gas pipelines.

“Will MLP general partners held in private hands, and MLP-able assets held by private-equity firms, abandon MLP IPOs?” he asked. “If the long arc toward free cash flow across the energy sector, not just in E&Ps, helps instill M&A discipline in midstream multiples, IPOs may still represent their best exits.”

Joseph Markman can be reached at jmarkman@hartenergy.com or 713-260-5208.

Recommended Reading

Technip Energies Wins Marsa LNG Contract

2024-04-22 - Technip Energies contract, which will will cover the EPC of a natural gas liquefaction train for TotalEnergies, is valued between $532 million and $1.1 billion.

Halliburton’s Low-key M&A Strategy Remains Unchanged

2024-04-23 - Halliburton CEO Jeff Miller says expected organic growth generates more shareholder value than following consolidation trends, such as chief rival SLB’s plans to buy ChampionX.

Diamondback May Go Nuclear to Power Permian Basin Ops

2024-04-08 - Oklo Inc., a California fission power plant developer, on April 8 said it signed a letter of intent to collaborate with Diamondback Energy on implementation of nuclear energy for drilling operations in the Permian Basin.

E&P Highlights: April 8, 2024

2024-04-08 - Here’s a roundup of the latest E&P headlines, including new contract awards and a product launch.

E&P Highlights: April 22, 2024

2024-04-22 - Here’s a roundup of the latest E&P headlines, including a standardization MoU and new contract awards.