Blame the vast political and geographical divide, blame an unclear regulatory climate, blame the U.S. shale revolution—which has reduced Canadian exports—blame the growing influence of the Indigenous people, blame environmental activism vs. development of the controversial oil sands, blame the inability to construct the final phases of the Keystone XL Pipeline (KXL) in the U.S., which would take that heavy oil to a ready and willing Gulf Coast market.

It all adds up to the same result: an energy industry with a loss of market share and capital investment.

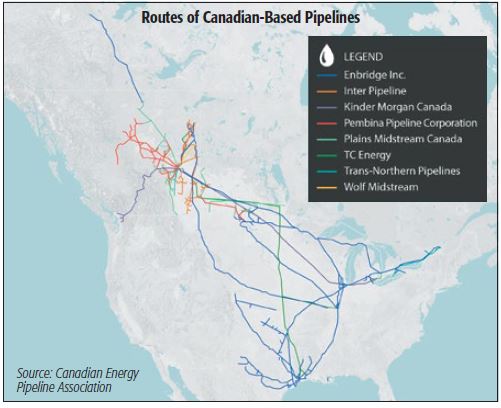

Since 2016, only one major transmission pipeline application has been put forward in Canada, compared to 14 in the U.S. Bottlenecks have constrained producers seeking to move their product. The main beneficiaries of this pipeline draught are railroads, owners of storage facilities and U.S. producers.

One report said rail offtake from the Western Canadian Sedimentary Basin (WCSB) rose 40% in April over March, though not close to the record set last December. Analysts at Peters & Co. estimate that, until a new export pipeline is completed, the WCSB will need at least 400,000 barrels per day (bbl/d) of rail and/or curtailments to balance the market.

Maxed-out storage

Maximum storage capacity is estimated at 37 million barrels (MMbbl). Even with cuts made last fall by Alberta producers, oil inventories in Western Canada set a record of 37.1 MMbbl in April, falling to 34 MMbbl in May, as reported by Genscape.

Hope arose in June after federal officials finally approved the long-awaited Trans Mountain Expansion Project (TMX), which will triple the amount of crude transported from the Edmonton region into British Columbia, ostensibly for export to Asia.

But it would have been far bigger news if the Trudeau administration had killed the C$7.4 billion project since his government bought its ownership from Kinder Morgan (see accompanying article).

In addition to TMX, the two other transmission pipeline projects are Enbridge’s Line 3 Replacement Program and TC Energy’s KXL. All three have been in progress for almost 10 years and are not forecast to be online for at least another two years. Construction on the Canadian portion of Line 3 is complete; however, the project is facing new delays in Minnesota.

KXL is in a holding pattern as well with legal challenges in Nebraska and Montana. KXL did receive a favorable appeals court ruling in Montana in late June, but TC Energy said it is too late for construction to start this year.

High cost of bottlenecks

In a study released in May, Toronto’s Fraser Institute estimated that pipeline bottlenecks last year cost Canadian oil producers C$20.62 billion because of the huge discounts they were forced to offer. According to the Fraser Institute, if Canadian producers last year could have shipped volumes equal to their current levels of production, Western Canadian Select would have traded at an average of US$52.90/bbl instead of the actual average price of US$38.30/bbl.

Last year, Canadian heavy crude traded at an average discount of US$26.50/bbl compared to US$11.90/bbl less than West Texas Intermediate (WTI) five years earlier.

The Canadian think tank pointed out that in September 2018, Western Canadian oil production reached 4.3 million bbl/d, but the takeaway capacity remained constant at 3.9 million bbl/d.

For Canada’s gross domestic product, the overall loss of oil revenue is about 1%.

Canadian producers and the Alberta provincial government agreed last fall to cut 8.7% of oil production, a scheme that has helped decrease the differential with WTI but is not seen as a long-term solution.

A new forecast released in June by the Canadian Association of Petroleum Producers (CAPP) was less than promising. CAPP estimated oil production will grow by an average of 1.4% annually until 2035, citing the lack of new pipelines and inefficient regulation for halving its forecast from five years ago.

Though Canada holds the world’s third-largest crude reserves, CAPP insisted, “We need pipeline capacity and more efficient regulatory policy to help bring investment back to the oil sector and drive growth.” CAPP also forecasts that capital investment in the industry will fall to C$37 billion (US $27.7 billion) in 2019, compared with C$81 billion in 2014.

Meeting challenges: C-69

Then there is C-69, the Impact Assessment Act that has sent an Arctic chill throughout the oil and gas industry. Following Canadian Senate approval in June by a 57-37 vote and already approved by the House of Commons, the bill quickly received royal assent to become law.

C-69 changes the review process by creating a new federal agency to assess industrial projects, such as pipelines, mines and inter-provincial highways, for their effects on public health, the environment and the economy. The Canadian Energy Regulator (CER) established by the Impact Assessment Agency (IAA) replaces both the National Energy Board and the Canadian Environment Assessment Agency.

Although the governing Senate Liberals accepted 99 proposed amendments, they rejected another 89 proposed by the Tory party that were sought by the energy industry. Alberta Premier Jason Kenney quickly labeled C-69 as the “No More Pipelines Law.”

One reason the Trudeau administration gave for rejecting those proposed amendments was that they would have allowed the IAA to not have to consider the effects on Indigenous people or climate change when assessing a project. Other changes would have restricted limits as to who can participate in an assessment hearing, as well as making it more difficult to challenge a project approval in court, Global News reported.

Martin Olszynski, associate professor of environmental law and natural resources at the University of Calgary, told Global News that the newly enhanced consultation process might instead reduce some of the litigation brought against future projects because it would bring potential critics into the decision-making process before they get to the courts.

Industry representatives, however, have reacted with predictable fury to C-69’s passage, insisting that it fails to create clarity and certainty necessary for future pipeline projects.

“We desperately need more investment,” Chris Bloomer, president and CEO of the Canadian Energy Pipeline Association (CEPA), told Midstream Business, saying that working on C-69 has, and will continue to be, among the group’s top priorities.

“Canada is sending mixed messages that will send critical investment elsewhere. Under C-69, our members have stated that it is unlikely that any new major pipeline project will be proposed, due to high financial risks associated with lengthy, costly project reviews. These are important projects, which inject billions of dollars into Canada’s economy—money that would help pay for critical social services and the transition to a lower-carbon energy future,” he said.

Lack of clarity

Bloomer said the industry is “gravely concerned” about the lack of clarity that has long surrounded Canada’s regulatory processes.

“To be more competitive we need to reduce regulatory layering between jurisdictions. Earlier this year, CEPA commissioned a report on regulatory competitiveness. CEPA makes seven recommendations based on the report.

“Our oil and natural gas resources are landlocked and because of that, foreign and domestic investors are either sitting idle or moving their money to more competitive jurisdictions. According to a report by the C.D. Howe Institute, planned investment in Canada’s natural resource sector projects fell $100 billion between 2017 and 2018. This staggering drop is equivalent to 4.5% of Canada’s gross domestic product,” Bloomer said.

“The real impact is the fact that a lot of capital has been reallocated in the industry to other parts of the world, including the U.S. We’ve seen the departure of some major players. It’s been very challenging and fast-moving. We’re still in an area where it’s a big concern,” he said.

Bloomer acknowledged that the future of energy development in Canada and worldwide is a highly divisive subject. He said CEPA’s research indicates that approximately one-third of Canadians are against pipelines; the other two-thirds are either supportive or neutral.

“It’s important to note that Canada is a world leader in the areas of producing and transporting oil and gas. The average emissions intensity of oil extraction has fallen 21% since 2009, with strong potential for further reductions in the next decade. Canada’s industry will reduce methane emissions by 45% from oil and natural gas operations by 2025,” said Bloomer, adding that he and CEPA members “look toward the future with cautious optimism.”

Positive long-term outlook

Analyst Mark Oberstoetter, research director in the Calgary office of Wood Mackenzie, said it maintains a positive long-term outlook for Canadian’s energy industry despite “significant egress challenges in the short term.

“The oil sands are ready to grow again with multiple steam-assisted gravity drainage projects ready for sanctioning and with improved economics breaking even below U.S.$60/bbl WTI,” he told Midstream Business. “But those sanctions will not occur until confidence in pipeline project construction improves. We see a positive path forward for all three major crude pipelines: Line 3

Replacement, KXL and TMX. But further delays remain possible which leave the upstream companies in further limbo.

“Oil production from Canada could reach 4 million bbl/d from the current level of 3 million bbl/d. But timing on when that growth occurs is chiefly dependent on those three large pipeline projects and shifting investor sentiment on long lifecycle projects.”

On the natural gas production side, he said, continued growth is driven largely by the Montney play, which is one of the world's top five largest unconventional resource plays behind only the Permian, Eagle Ford and Marcellus.

“Growth would occur without LNG investment, but the increased demand coming from LNG Canada and Woodfibre help bolster our outlook for liquids-rich gas drilling in Canada’s resource plays. We see the Montney growing to 20 billion cubic feet equivalent per day by 2030, led by many Canadian-based specialists alongside well-known companies like Shell, Petronas, Encana, ConocoPhillips and Murphy,” Oberstoetter added.

The challenges

What are the biggest challenges energy developers face?

“Regulatory delays and legal roadblocks, public protests, changing political regimes, investor sentiment and cost management are all big issues in getting major projects built,” he said.

“For upstream energy, an expansion to an oil sands project or drilling horizontal wells does not face all of these same challenges. Those companies are most challenged by the factors outside of their control: market access. They have to invest amid uncertainty over which pipelines get built, which determines market options and pricing.”

Oberstoetter said TMX is critical for the Canadian industry, although local permits, further legal challenges and public protests could all cause delay.

“The pipeline is important emotively as an example of getting projects built. It would also offer market diversity away from the U.S. Other pipelines are equally important economically especially as they offer routes to the high-demand U.S. Gulf Coast heavy crude market.

“If all three crude pipelines get built, we’d expect TMX to bring an extra benefit to light oil production, given access to markets in the U.S. Northwest and shipping to Brent-linked markets [not discounted WTI or Edmonton Mixed Sweet Blend].

“That said, the regulatory approval timeline and stability, knowing it won’t change midway through, is a major factor for investors all over the world. I’d argue construction of the already approved projects is most important to get investor confidence back into upstream investments, but regulatory uncertainty will always loom if unaddressed,” he added.

KXL is estimated to add ~$4-$5/bbl in relative value for all Western Canadian crude grades. Meanwhile, TMX has the biggest impact for lighter barrels should all three proceed. Despite some recent setbacks (the Minnesota Court of Appeals overturned the approval of the Environmental Impact Statement), Line 3 has the clearest regulatory path forward to completion in 2021, he said.

Ridley Island

The successful construction of Altagas’ Ridley Island Propane Export Terminal at Prince Rupert, British Columbia, this year will be positive for NGL prices. Pembina is also moving forward with an export project at Prince Rupert and a propane dehydrogenation plant in Alberta and shifting Alberta’s production away from reliance on U.S. exports, the analyst said.

“On the gas side, LNG Canada is already moving ahead, and we expect Woodfibre LNG to make a final investment decision (FID) in 2019. Kitimat LNG, Jordan Cove and/or Goldboro LNG would all be additional upside but with longer term startups and not without their challenges.”

LNG Canada has proposed a gas liquefaction operation at Kitimat. Woodfibre LNG is a proposed liquefaction operation north of Vancouver. Jordan Cove would be at Coos Bay, Oregon, drawing primarily on Canadian-produced gas. Goldboro LNG has been proposed in Nova Scotia on Canada’s Atlantic coast.

“We do need continued investment in the processing plants; 2.2 Bcf/d is being built over the next three years in British Columbia and another 1.3 Bcf/d in Alberta, as well as regional pipeline buildouts: TC Energy’s Upstream of James River capacity additions, North Montney Phase I and II, WEI T-South expansion, Coastal GasLink,” Oberstoetter said.

In July, Plains Midstream Canada announced plans to expand its Rangeland crude oil pipeline to provide more capacity north to Edmonton and south to Carway on the Alberta-Montana border. Combined, the expansion will increase Rangeland’s current light crude oil capacity to 200,000 bbl/d. The expansions will be staged into service later this year with full capacity in 2021.

__________________________________________________________________________

[sidebar]

All Eyes Are On The Trans Mountain Expansion

The Government of Canada gave final approval in June for the C$7.4 billion Trans Mountain Expansion (TMX) project, subject to 156 conditions. First proposed in 2012, the project will triple the pipeline capacity from near Edmonton, Alberta, to Burnaby, British Columbia, near Vancouver.

The approval followed a federal court-ordered review of marine protection measures and more consultations with Indigenous people along the pipeline route.

Trans Mountain President and CEO Ian Anderson said construction should restart in September, pending no further delays.

“I think they’re anxious to see us get started and anxious to get back to work,” he said.

Construction will resume where it halted in August 2018. He said the project will eventually employ 5,000- to 6,000 workers.

Back at Burnaby

The work begins at Burnaby.

“It’ll be back in Burnaby at our Westridge Marine Terminal, building out our dock, working in the Burnaby Terminal and recommencing work in the spread west of Edmonton and east of Jasper National Park. That’s where we’ll go back to work first. Then, over time as final permits and land acquisitions are made, we would work into the Edmonton area as well as the North Thompson area north of Kamloops as our next locations,” he said.

Trans Mountain has operated a pipeline from Edmonton to Burnaby since 1953, bringing refined and unrefined products in a batch system into British Columbia and Washington State. Burnaby is home to two terminals—one houses 13 oil storage tanks and the other is the marine terminal, where fear of tanker spills has drawn opposition.

The pipeline has operated at its maximum capacity for many years. Producers primarily from the oil sands want additional space to ship more product and access world markets, specifically the Pacific Rim.

Trans Mountain decided a twinning of the existing pipeline was the best solution. The second line follows 73% of the original route and includes 610 miles of pipe with 12 new pumping stations, boosting capacity from 300,000 bbl/d to 890,000 bbl/d. Commercial agreements are in place with at least 13 shippers for 15 to 20-year contracts.

It is North America’s only oil pipeline with access to the West Coast.

Government owned

Trans Mountain Pipeline is a wholly owned subsidiary of the Canadian Development Investment Corp. (CDEV), which is accountable to Parliament. Trans Mountain was owned by Kinder Morgan Canada, which sold the company to the federal government in 2018 because of increased opposition to the expansion, including a trade war between Alberta and British Columbia.

The plan is for outside investors, possibly including Indigenous communities, to buy into the project. Though not all Indigenous groups support the expansion, the Vancouver Sun reported that one influential organization hopes to acquire an equity stake.

“We always wanted equity, but in our negotiations with Kinder Morgan, equity was not on the table. When the Government of Canada bought the pipe it opened the door to equity,” said Michael LeBourdais, chair of the Western Indigenous Pipeline Group. He said ownership will give Indigenous people along the route the power to lead environmental risk assessments and “realize the largest economic benefits.

“This pipeline goes right through the middle of our reserve … so we are very familiar with where this pipeline goes and how it works. Most of us are firefighters, forestry workers and oil patch workers. We understand how safe it is. We can retain the expertise and the capacity to own and operate a chunk of this pipeline, and that’s what we’re going to do,” LeBourdais said.

Wood Mackenzie analyst Mark Oberstoetter told Midstream Business that Indigenous participation is expected.

“While uncertain, we could see a government and Indigenous group partner during construction, and perhaps an industry group replace the government’s share once built and de-risked. Private equity partners have shown high interest in other de-risked infrastructure projects.”

—Jeffrey Share

Recommended Reading

TGS Starts Up Multiclient Wind, Metaocean North Sea Campaign

2024-05-07 - TGS is utilizing two laser imaging and ranging buoys to receive detailed wind measurements and metaocean data, with the goal of supporting decision-making in wind lease rounds in the German Bright.

Spate of New Contracts Boosts TechnipFMC's Subsea Profits

2024-04-30 - TechnipFMC's operational profits are growing as the company heightened its focus on “quality” subsea orders, which earned $2.4 billion for the first quarter.

Message in a Bottle: Tracing Production from Zone to Wellhead

2024-04-30 - New tracers by RESMAN Energy Technology enable measurement while a well is still producing.

Defeating the ‘Four Horsemen’ of Flow Assurance

2024-04-18 - Service companies combine processes and techniques to mitigate the impact of paraffin, asphaltenes, hydrates and scale on production—and keep the cash flowing.

Tech Trends: AI Increasing Data Center Demand for Energy

2024-04-16 - In this month’s Tech Trends, new technologies equipped with artificial intelligence take the forefront, as they assist with safety and seismic fault detection. Also, independent contractor Stena Drilling begins upgrades for their Evolution drillship.