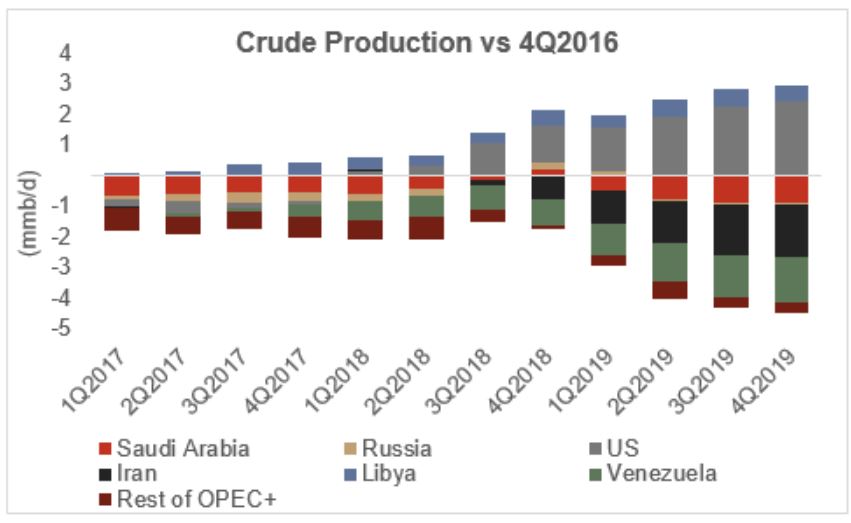

OPEC Ministers are meeting in Vienna to discuss extending or even deepening the current OPEC+ supply agreement, Stratas Advisors reported on Dec. 4. After swiftly convincing markets that an extension until June 2020 was virtually guaranteed, ministers have entered today’s meeting with markets now expecting cuts to be both extended and deepened from 1.2 million barrels per day (MMbbl/d) to as much as 1.6 MMbbl/d. In such a scenario Saudi Arabia would most likely need to bear the brunt of the cut, taking production well below 10 MMbbl/d for much of 2020.

Stratas Advisors continues to believe that a flat extension until at least June of 2020 (if not December) is the most likely outcome, with continued emphasis on increasing compliance. Members are earning more money selling less crude than in the fourth quarter of 2016 when the agreement was struck. However, while OPEC+ members have benefitted from the supply agreement, so have U.S. producers with U.S. crude and condensate production in the third quarter of 2019 approximately 3.1 MMbbl/d above fourth quarter 2016 levels.

Stratas’ Global Hydrocarbon Supply team expects non-OPEC production growth to average 1.4 MMbbl/d in 2020 with increases seen in Brazil, Canada, Norway and potentially Mexico. The bulk of production growth in 2020 though will continue to come from the United States, albeit at a lower rate than in previous years.

Even if a deeper cut is agreed to and complied with, it might not be enough to raise prices substantially. A cut of 1.5 MMbbl/d would barely cover the expected growth in non-OPEC production, leaving markets in a similar situation to this year. However, negative expectations about global demand growth continue to be the dominant variable impacting crude oil prices. As discussed in Stratas’ last global economic outlook several measurements of market uncertainty are showing unprecedented levels, highlighting how pervasive uncertainty about global trade is among governments, traders, and consumers. While still not expecting a global contraction, analysts expect widespread pain and a slowdown in growth in several major countries. Risks remain skewed to the downside and several significant trade disputes remain unresolved heading into 2020.

Recommended Reading

Sapura Acquires Exail Rovins’ Nano Inertial Navigation System

2024-02-01 - Exail Rovins’ Nano Inertial Navigation System is designed to enhance Sapura’s subsea installment capabilities.

Forum Energy Signs MOU to Develop Electric ROV Thrusters

2024-03-13 - The electric thrusters for ROV systems will undergo extensive tests by Forum Energy Technologies and SAFEEN Survey & Subsea Services.

AI Advancing Underwater, Reducing Human Risk

2024-03-25 - Experts at CERAWeek by S&P Global detail the changes AI has made in the subsea robotics space while reducing the amount of human effort and safety hazards offshore.

Tech Trends: Autonomous Drone Aims to Disrupt Subsea Inspection

2024-01-30 - The partners in the project are working to usher in a new era of inspection efficiencies.

Tech Trends: QYSEA’s Artificially Intelligent Underwater Additions

2024-02-13 - Using their AI underwater image filtering algorithm, the QYSEA AI Diver Tracking allows the FIFISH ROV to identify a diver's movements and conducts real-time automatic analysis.