A sign marks where the Texas-New Mexico state line road, which leads to WPX Energy’s Delaware Basin Stateline operations in Loving County, Texas. (Source: Tom Fox/Hart Energy)

WPX Energy Inc. (NYSE: WPX) said Feb. 4 it had executed on roughly $300 million worth of deal making as the company retools it Permian Basin portfolio amid plans to slow down operations in 2019.

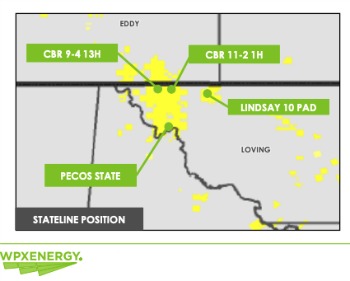

WPX, an independent energy producer with core positions in the Permian and Williston basins, agreed to divest certain holdings in the Delaware Basin in separate transactions for aggregate proceeds in excess of $200 million. In conjunction, the company plans to reinvest $100 million of the sales proceeds to purchase surface acreage within its core Stateline operations in the Delaware.

The transactions will leave WPX Energy with a net cash inflow of about $100 million.

“We remain opportunistic as we manage our portfolio with respect to disciplined development and capital execution,” Rick Muncrief, chairman and CEO of WPX Energy, said in a statement.

Also, on Feb. 4, WPX Energy updated its guidance for 2019 due to the recent pullback in commodity pricing. The updated 2019 plan cuts capital by more than $350 million.

Slowing Down

WPX reduced its full-year 2019 capex guidance to between $1.1 billion and $1.275 billion from prior guidance of $1.45 billion and $1.65 billion, which analysts with Capital One Securities Inc. said represents a 23% cut at guidance midpoint.

“We have already seen and expect to continue seeing similar announcements from other operators as we approach [fourth-quarter] reporting,” Capital One analysts wrote in a research note on Feb. 4.

Production guidance was also lowered by 6% to between 149,000 and 161,000 barrels of oil equivalent per day (boe/d). In addition, WPX reduced its 2019 rig count to eight from 10 with two rigs to be dropped in the first quarter. The company now plans to run five rigs in the Permian Basin and three rigs in the Bakken within the Williston for the rest of the year.

The updated 2019 plan is focused on disciplined growth within cash flow based on a West Texas Intermediate oil price of $50 per barrel. The company expects to maintain momentum into 2020 with 5%-10% production growth from fourth-quarter 2018 to fourth-quarter 2019 based on a revised eight-rig program.

“We’ve worked hard over the past few years to position the company to spend within cash flows in a $50 world and still deliver nice growth,” Muncrief said. “We’re also going to keep our balance sheet strong, continue the technical work that’s driving savings and cost efficiencies, and maintain the optionality we have with our two producing assets and our midstream ownership.”

Deal Making

The Stateline acquisition comprises about 14,000 surface acres in WPX’s core development area within the Delaware Basin. Information on the seller and associated production has not been released.

“The investment in Stateline surface acreage is another example of how we transform potential constraints into opportunities for value creation,” Clay Gaspar, WPX president and COO, said in a statement. “The acreage will provide economic returns through speed of development, facilitating longer laterals, right of way access, and revenue associated with infrastructure like roads, water and electricity.”

WPX holdings in the Stateline area currently include roughly 60,000 net acres, according to Gabriele Sorbara, principal and senior equity analysts with The Williams Capital Group LP.

“We expect WPX to continue to further block up its position, build scale and increase efficiencies in the Delaware Basin,” Sorbara wrote in a Feb. 4 research note. “The WhiteWater sale occurred as planned, and its equity interests in the Oryx pipeline systems are expected in [second-half 2019].”

Sorbara noted The Williams Capital Group values WPX’s equity interests in the Oryx pipeline at $400 million.

WPX’s sales consist of separate transactions for an equity interest in a third-party pipeline and noncore Nine Mile Draw E&P assets in southern Reeves County, Texas. Closings are expected in the first quarter, according to the company release.

One sale consists of WPX’s 20% equity interest in WhiteWater Midstream’s Agua Blanca natural gas pipeline to First Infrastructure Capital Advisors LLC. The other sale involves roughly 5,600 net acres and about 1,500 boe/d of production in an area significantly outside of WPX’s core Stateline development in the Delaware Basin to an undisclosed buyer.

Agua Blanca is a natural gas residue pipeline servicing the Delaware Basin. The system consists of roughly 90 miles of 36-inch diameter pipeline and 70 miles of smaller diameter pipeline crossing portions of Culberson, Loving, Pecos, Reeves, Ward and Winkler counties in West Texas.

The Agua Blanca transaction was also a part of another acquisition for a 60% stake in the line by First Infrastructure Capital from WhiteWater Midstream and its financial sponsors, Denham Capital Management and Ridgemont Equity Partners. The Houston-based investment firm announced the acquisition on Feb. 4.

WPX will continue to be a shipper on the Agua Blanca line, which has an initial capacity is about 1.4 billion cubic feet per day with significant expansion plans underway.

Tudor, Pickering, Holt & Co. and Credit Suisse Securities (USA) LLC advised WPX on the Whitewater transaction.

Tudor, Pickering, Holt & Co. and Credit Suisse Securities (USA) LLC also acted as financial advisers to WhiteWater, Denham, and Ridgemont in connection with the Agua Blanca transaction. Simmons Energy, a division of Piper Jaffray, was the exclusive financial adviser to First Infrastructure Capital. Sidley Austin LLP was lead counsel for WhiteWater and Denham. Troutman Sanders LLP was lead counsel for Ridgemont. Latham & Watkins LLP was lead counsel for WhiteWater management. Milbank, Tweed, Hadley & McCloy LLP was lead counsel for First Infrastructure Capital.

Recommended Reading

Exclusive: Rebellion Energy Orphan Well Method Pinpoints the Particulars in Plugging

2024-03-01 - Rebellion Energy Solutions CEO Staci Taruscio dives into the company's methods when plugging for permanence in this Hart Energy LIVE Exclusive with Editorial Director Jordan Blum.

MethaneSAT: EDF’s Eye in the Sky Targets E&P Emissions

2024-03-07 - The Environmental Defense Fund and Harvard University recently launched MethaneSAT, a satellite tracking methane emissions. The project’s primary target: oil and gas operators.

Exclusive: Scepter CEO: Methane Emissions Detection Saves on Cost

2024-04-08 - Methane emissions detection saves on cost and "can pay for itself," Scepter CEO Phillip Father says in this Hart Energy exclusive interview.

SAF End-users, Producers Talk Challenges, Solutions

2024-02-07 - The lower lifecycle emissions of sustainable aviation fuel are seen as a key lever for airlines to reduce carbon emissions, but cost is a challenge.

A Different Way to Approach Energy Industry Hiring

2024-02-07 - Modern energy companies have embraced competitive efficiency, cutting-edge innovation and ESG transparency. It is time for modern energy hiring to do the same.