At the end of 2017, the United Arab Emirates (UAE) bought U.S. oil in the form of condensate. Remarkably, due to political complications, the UAE finds it more expedient to import from Texas than from its neighbors. The shipment originated from Enterprise Products Partners’ Houston terminal, but even before that, shipments previously moved through any number of MLP-owned pipelines, storage facilities and gathering systems.

While the UAE is a dramatic example, the U.S. has regularly been exporting oil to points as far away as the U.K. and China.

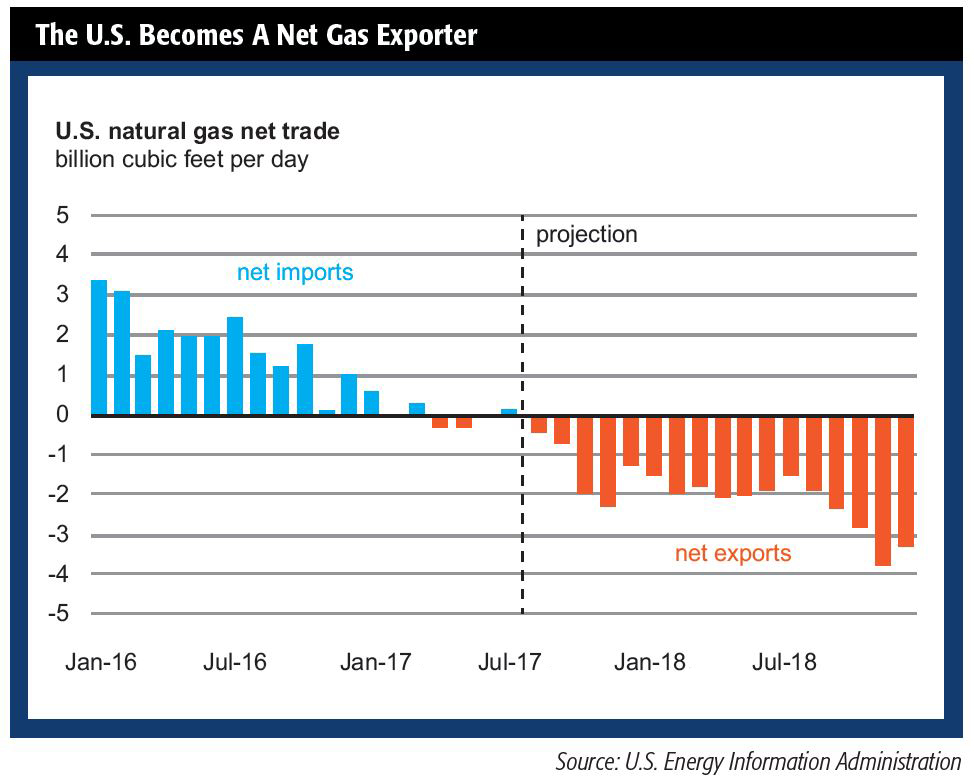

While analysts focus on oil prices and production, natural gas remains underappreciated. Natural gas liquefaction facilities that support exports have been under construction for years in the U.S., and they are now starting to come online. One of the most recent to do so is Dominion Energy’s Cove Point LNG plant, which will be exporting LNG to Asian markets from its location on the Maryland coast.

U.S. LNG has also been delivered to Europe, where it provides an alternative to Russian natural gas. As more and more liquefaction facilities begin operations, they will require midstream assets to provide them with natural gas to liquefy.

These two examples highlight something remarkable: The U.S. has become a significant energy exporter—something unimagined a few years ago, even after the crude export ban was lifted in 2015. Perhaps even more importantly, it’s become the swing producer for the world’s energy needs.

As global GDP continues to grow, it will need to be fueled by something. If one assumes that incremental energy needs will be met in the same proportion as current energy use, most of the new demand will be met by hydrocarbons. With the U.S. now positioned as the swing producer, U.S. oil and gas will be needed globally.

While this provides a boon to producers and exporters of energy, midstream companies will be quietly connecting the two. Oil, natural gas and NGL need to move from inland production areas like the Permian and the Marcellus to ports and liquefaction facilities on the coasts.

Midstream MLPs facilitate this movement.

In short, exports of both oil and natural gas continue to increase as the U.S. begins to meet the world’s needs for incremental energy production. As global GDP continues to grow and energy demand worldwide increases despite the short-term moves in the market, the opportunity set for MLPs remains robust.

Maria Halmo is the director of research at Alerian, an independent provider of MLP and energy infrastructure market intelligence. As of January 2018, over $16 billion is directly tied to the Alerian Index Series. For additional commentary and research, please visit alerian.com/alerian-insights.

Recommended Reading

2023-2025 Subsea Tieback Round-Up

2024-02-06 - Here's a look at subsea tieback projects across the globe. The first in a two-part series, this report highlights some of the subsea tiebacks scheduled to be online by 2025.

Subsea Tieback Round-Up, 2026 and Beyond

2024-02-13 - The second in a two-part series, this report on subsea tiebacks looks at some of the projects around the world scheduled to come online in 2026 or later.

Tech Trends: Autonomous Drone Aims to Disrupt Subsea Inspection

2024-01-30 - The partners in the project are working to usher in a new era of inspection efficiencies.

Haynesville’s Harsh Drilling Conditions Forge Tougher Tech

2024-04-10 - The Haynesville Shale’s high temperatures and tough rock have caused drillers to evolve, advancing technology that benefits the rest of the industry, experts said.

Betting on the Future: Chevron Technology Ventures’ Investment Strategy

2024-04-09 - After a quarter century, Chevron Technology Ventures seeks both incremental and breakthrough technologies with its early-stage investment program.