On May 17, there were three big announcements that certain MLPs would be acquired by their parent companies structured as conventional corporations (C-corps). The Williams Cos. Inc. is acquiring its MLP, Williams Partners LP; Cheniere Energy Inc. is buying the remaining interest in Cheniere Energy Partners LP Holdings; and most notably—in a simplification transaction similar to Kinder Morgan Inc. in 2014—Enbridge Inc. is buying-in all its sponsored investment vehicles, including four MLPs.

Williams, Cheniere and Enbridge rank Nos. 6, 10 and 1, respectively, on the Midstream Business Midstream 50 list of the sector’s largest publicly held firms.

Against a backdrop of a few other conversions, as well as tax updates discussed previously in this space, the avid MLP researcher is tempted to counter the above news with other specific examples like the commitment of both Enterprise Products Partners LP and Magellan Midstream Partners LP to remain MLPs. Or even that NuStar Energy LP’s simplification transaction preserved the MLP.

That context is important to know before addressing two specific concerns:

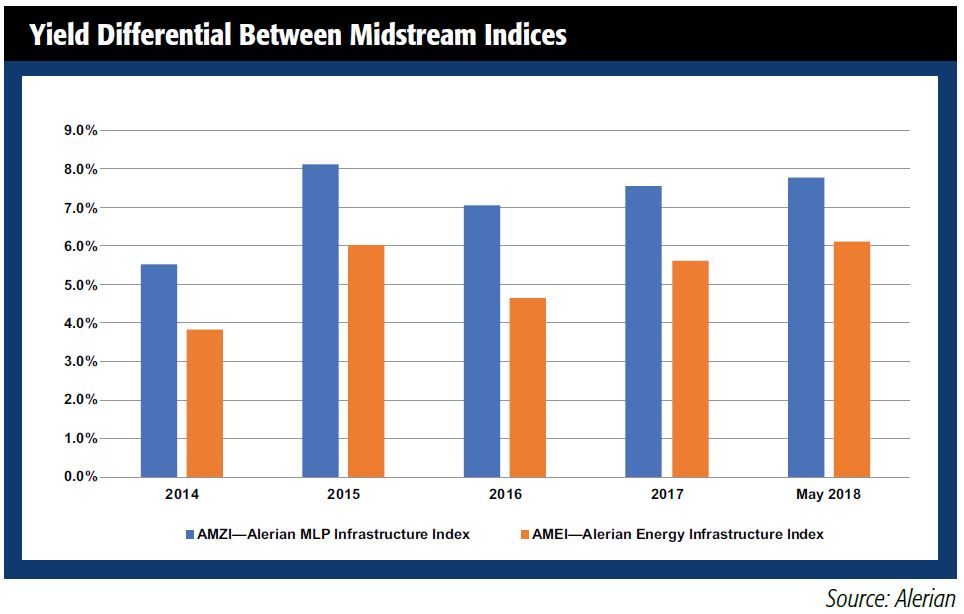

1. If you want yield—Because MLPs are pass-through structures, they pay no federal income tax at the company level. Generally, this additional money is instead paid out to unitholders. As of June, the typical midstream MLP was yielding between 6%-8%, whereas the typical midstream C-corp might yield between 3%-5%. Compared with other asset classes, both numbers are respectable.

2. If you’re a midstream devotee—Midstream MLPs traditionally have had a loyal investor base. Many investors have put in the time to understand the midstream business model and want continued exposure—preferably owning a basket of the biggest MLPs—but are no longer sure how to balance between MLP and midstream C-corp exposure. Or, investors who originally preferred MLP mutual funds, exchange-traded funds, or exchange trading for other purposes now wonder whether their fund provides complete midstream exposure.

Funds mixing midstream MLP and midstream C-corps, known as regulated investment company-compliant (RIC) products, have exposure to MLPs that is capped at 25%. These typically will provide greater diversification at the expense of a lower yield and lower tax-deferred return of capital percentages vs. 100% MLP products.

Products that remain dedicated to 100% MLP exposure will continue to exist, as some investors’ primary objective is income, but are likely to become either more concentrated in the larger names and/or provide additional exposure to mid-cap MLPs. Investor expectations may need adjustment, as both options carry some additional risk.

The Alerian MLP Infrastructure Index (NYSE: AMZI) tracks only midstream MLPs. The Alerian Energy Infrastructure Index (SNP: AMEI) includes both midstream MLPs and midstream C-corps.

Fortunately for the midstream investor, the process of evaluating the underlying business remains the same regardless of the structure.

At the end of the day, midstream MLPs continue to represent a significant portion of the U.S. midstream space. They continue to have higher yields than their C-corp counterparts, and while it would be premature to say midstream MLPs are disappearing, it is always appropriate for investors to revisit their primary investment objectives and understand whether their exposure adequately reflects such objectives.

Maria Halmo is the director of research at Alerian, an independent provider of MLP and energy infrastructure market intelligence. As of the end of May, over $14 billion is directly tied to the Alerian Index Series. For additional commentary and research, please visit alerian.com/alerian-insights.

Recommended Reading

New Fortress Starts Barcarena LNG Terminal Operations in Brazil

2024-03-01 - New Fortress’ facility consists of an offshore terminal and an FSRU that will supply LNG to several customers.

Exclusive: Chevron Balancing Low Carbon Intensity, Global Oil, Gas Needs

2024-03-28 - Colin Parfitt, president of midstream at Chevron, discusses how the company continues to grow its traditional oil and gas business while focusing on growing its new energies production, in this Hart Energy Exclusive interview.

Midstream Builds in a Bearish Market

2024-03-11 - Midstream companies are sticking to long term plans for an expanded customer base, despite low gas prices, high storage levels and an uncertain political LNG future.

Imperial Expects TMX to Tighten Differentials, Raise Heavy Crude Prices

2024-02-06 - Imperial Oil expects the completion of the Trans Mountain Pipeline expansion to tighten WCS and WTI light and heavy oil differentials and boost its access to more lucrative markets in 2024.

Trans Mountain Pipeline Announces Delay for Technical Issues

2024-01-29 - The Canadian company says it is still working for a last listed in-service date by the end of 2Q 2024.