Stratas Advisors highlights several emerging positive factors for oil prices and developments of last week only provided further evidence for the positive factors. (Source: Shutterstock.com)

[Editor’s note: This report is an excerpt from the Stratas Advisors weekly Short-Term Outlook service analysis, which covers a period of eight quarters and provides monthly forecasts for crude oil, natural gas, NGL, refined products, base petrochemicals and biofuels.]

The price of Brent crude ended the week at $ 72.92 after closing the previous week at $72.48. The price of WTI crude ended the week at $69.72 after closing the previous week at $69.10.

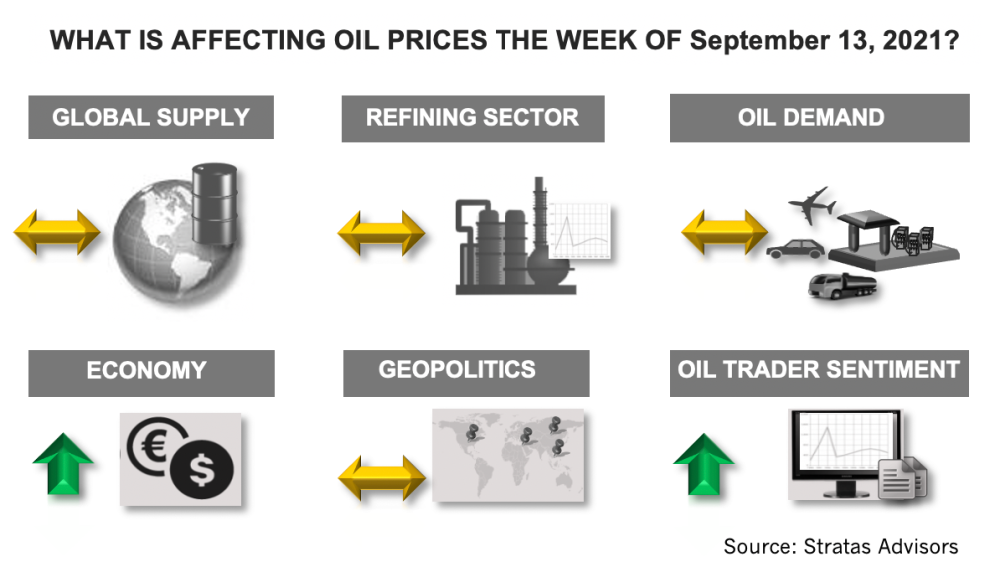

In last week’s note, we highlighted several emerging positive factors for oil prices and developments of last week only provided further evidence for the positive factors. Firstly, is the expectation for the continuation of accommodating monetary policies by the U.S. Federal Reserve and the European Central Bank (ECB). After the recent major speech by the chairman of the U.S. Federal Reserve and the outcome from the Sept. 9 meeting of the ECB, we are still holding to our expectation that these entities will err on the side of being too accommodating, instead of tightening too soon and stifling the economic recovery. Additionally, as has been the situation for the last several weeks, there continue to be signs that the latest wave of COVID-19 is rolling over. From a global standpoint, cases over the last 14 days declined by 18% and deaths declined over the last 14 days by 13%. For the first time since the beginning of the current wave, cases are now declining in all regions: Europe, Middle East, Latin America, Africa, Asia—and finally North America. It is also worth noting that the number of cases and deaths in the current wave never hit the peak of the previous wave that took place in April/May of this year. Cases only reached about 80% of the previous peak, and deaths only reached about 70% of the previous peak.

Additionally, there are factors that will contain oil prices. If prices move too high, the stability of OPEC+ will be more difficult to maintain, since higher oil prices will encourage further supply from OPEC+ members who are eager to pump more oil. Higher prices will also encourage more drilling activity from the shale producers in the US, although this group has been maintaining focus on generating free cashflow and limiting capex. Large consumers of crude oil will also react to higher crude prices, as illustrated by China releasing crude oil from its crude-oil reserve. The action indicates that China is still sensitive about rising oil prices, even though China’s currency has strengthened against the U.S. dollar. Additionally, China will utilize counter-cyclical purchases—buying more when prices are low and reducing purchases when prices are high.

As such, while we are expecting oil prices to drift upward with Brent crude averaging around $76 in the fourth quarter of this year, and the price of WTI averaging around $72, we are also expecting that oil prices will trade in a relatively narrow channel through the rest of the year.

About the Author:

John E. Paise, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

Energy Transfer Announces Cash Distribution on Series I Units

2024-04-22 - Energy Transfer’s distribution will be payable May 15 to Series I unitholders of record by May 1.

Balticconnector Gas Pipeline Back in Operation After Damage

2024-04-22 - The Balticconnector subsea gas link between Estonia and Finland was severely damaged in October, hurting energy security and raising alarm bells in the wider region.

Wayangankar: Golden Era for US Natural Gas Storage – Version 2.0

2024-04-19 - While the current resurgence in gas storage is reminiscent of the 2000s —an era that saw ~400 Bcf of storage capacity additions — the market drivers providing the tailwinds today are drastically different from that cycle.

Ozark Gas Transmission’s Pipeline Supply Access Project in Service

2024-04-18 - Black Bear Transmission’s subsidiary Ozark Gas Transmission placed its supply access project in service on April 8, providing increased gas supply reliability for Ozark shippers.