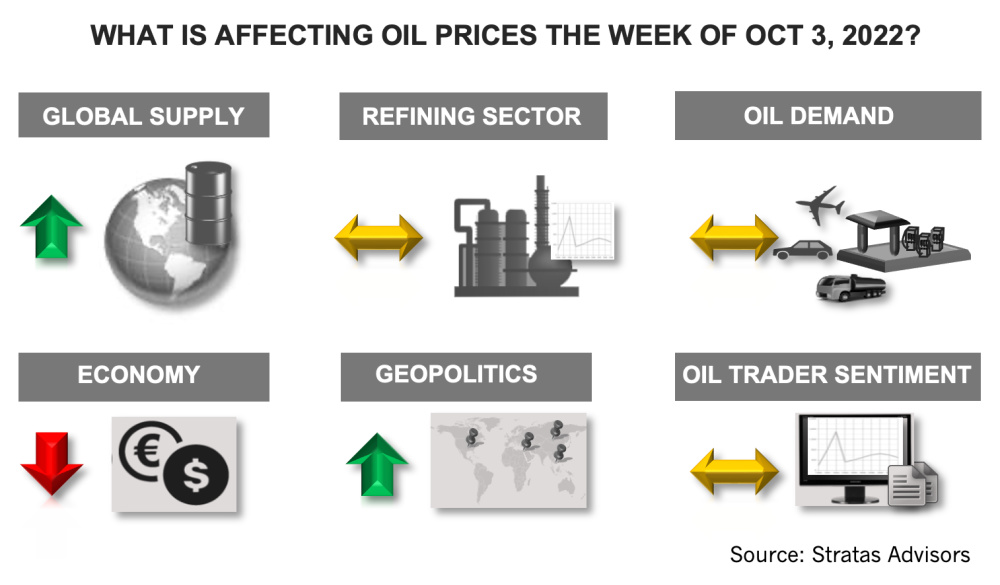

In last week’s note, Stratas Advisors highlighted that the economy would be the governing factor for oil prices from a short-term time horizon. And while there have been a lot of other recent and pending developments, Stratas still thinks that will remain the case, the firm said in its latest oil price forecast. (Source: Shutterstock.com)

Learn more about Hart Energy Conferences

Get our latest conference schedules, updates and insights straight to your inbox.

Editor’s note: This report is an excerpt from the Stratas Advisors weekly Short-Term Outlook service analysis, which covers a period of eight quarters and provides monthly forecasts for crude oil, natural gas, NGL, refined products, base petrochemicals and biofuels.]

The price of Brent crude ended the week at $85.14 after closing the previous week at $85.03. The price of WTI ended the week at $79.49 after closing the previous week $78.74.

In last week’s note, we highlighted that the economy would be the governing factor for oil prices from a short-term time horizon. And while there have been a lot of other recent and pending developments, we still think that will remain the case. With respect to the U.S., the Federal Reserve is expected to raise rates by 75 basis points in November and 50 basis points in December. There are risks, however, associated with the Federal Reserve raising rates aggressively while the U.S. economy is showing signs of fragility.

- New jobless claims declined to the lowest level in five months according to the latest report from the U.S. Labor Department, but the U.S. jobs market has some underlying weakness. Data from the Bureau of Labor Statistics indicates that the number of full-time jobs declined by 242,000 jobs in August and by 465,000 during the months of June, July and August, while the number of average week hours has fallen to 34.5 from the 34.8 at the end of 2021.

- Labor productivity for all non-farm employees fell by 2.4% in the second quarter of this year in comparison with the same period of 2021. Real wages have also been declining with real wages falling by 1.7% in 2Q after falling by 0.4% in the first quarter of this year.

- GDP growth in the U.S. is also mixed with the Commerce Department keeping the GDP growth for the second quarter at a negative 0.6% annualized rate and a negative 1.6% annualized rate for the first quarter. With respect to the third quarter the nowcast from the Atlanta Fed spiked to 2.4% on Friday from 0.3% on September. The upward adjustment stems, in part, from the third-quarter personal consumption expenditures growth and third-quarter gross private domestic investment growth increasing from 0.4 percent and -7.6%, respectively, to 1% and -4.2%.

The tightening monetary policy continues to provide support for the U.S. dollar. The U.S. Dollar Index, declined last week to 112.17 after closing the previous week at 113.10, but remains at the highest level since early in 2002. The strong U.S. dollar is putting further pressure on the economies of other countries because it is making dollar-denominated commodities more expensive.

Inflation in Germany increased to 10% in September from 7.9% in August, and is being driven by energy prices, which are 43.9% higher than in September of 2021. Germany’s economy is expected to be in recession during the rest of the year and through 2023 with a contraction of 0.4% according to Germany’s Joint Economic Forecast. Ironically, the more effective the pending restrictions on Russia’s energy sector, the more downward pressure will be put on the economies of Europe, including Germany.

China’s economy is still being hampered by restrictions pertaining to COVID-19 and highly over-leveraged property sector. According to Goldman Sachs, cities under some form of COVID-19 restrictions still accounts for 25% of China’s gross domestic product. While the latest data for factory output and retail sales were better than expected, the latest data from China’s National Bureau of Statistics shows that service sector fell from 51.9 to 48.9 in September with a reading below 50 indicating contraction. The Chinese Yuan has weakened substantially since April of this year with moving from 6.36 to the US dollar to 7.12 to the U.S. Dollar. Even if the COVID-19 restrictions are removed, it is unlikely that China’s economy will rebound with the economies of two of its major trading partners—Europe and the U.S.—slowing down. We are projecting that China’s growth in the third quarter will be 1.19% and forecasting that growth in the fourth quarter will be 3.25%.

From a supply perspective, members of OPEC+ are to meet on Oct. 5, and it appears that the group will act in response to weakening economic activity and oil demand growth. It is expected that OPEC+ will announce a reduction in supply of at least 1 million bbl/d to provide support for crude prices. Additionally, it is likely that Saudi Arabia will reduce its supply further through a voluntary reduction. In our note of Sept. 19, we expressed the view that member of OPEC+ would adjust supply to align with the waning demand in attempt to defend $90 price. While many members of OPEC+ have been struggling to meet production targets, reduction in supply by Saudi Arabia will represent actual barrels being taken off the market.

While there has been plenty of recent news, we are holding to our forecast that the price of Brent crude oil will average $88.43 in the fourth quarter, while WTI averages $82.48 and Dubai crude oil averages $84.10.

For a complete forecast of energy prices, including crude oil and refined products, please refer to our Short-term Outlook.

About the Author: John E. Paise, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

Exxon Mobil Guyana Awards Two Contracts for its Whiptail Project

2024-04-16 - Exxon Mobil Guyana awarded Strohm and TechnipFMC with contracts for its Whiptail Project located offshore in Guyana’s Stabroek Block.

Deepwater Roundup 2024: Offshore Europe, Middle East

2024-04-16 - Part three of Hart Energy’s 2024 Deepwater Roundup takes a look at Europe and the Middle East. Aphrodite, Cyprus’ first offshore project looks to come online in 2027 and Phase 2 of TPAO-operated Sakarya Field looks to come onstream the following year.

E&P Highlights: April 15, 2024

2024-04-15 - Here’s a roundup of the latest E&P headlines, including an ultra-deepwater discovery and new contract awards.

Trio Petroleum to Increase Monterey County Oil Production

2024-04-15 - Trio Petroleum’s HH-1 well in McCool Ranch and the HV-3A well in the Presidents Field collectively produce about 75 bbl/d.

Trillion Energy Begins SASB Revitalization Project

2024-04-15 - Trillion Energy reported 49 m of new gas pay will be perforated in four wells.