While not directly affecting oil prices in the short-term, Stratas Advisors also noted some interesting developments from COP 27 being held in Egypt that ended on Nov. 20. (Source: Shutterstock.com)

Editor’s note: This report is an excerpt from the Stratas Advisors weekly Short-Term Outlook service analysis, which covers a period of eight quarters and provides monthly forecasts for crude oil, natural gas, NGL, refined products, base petrochemicals and biofuels.]

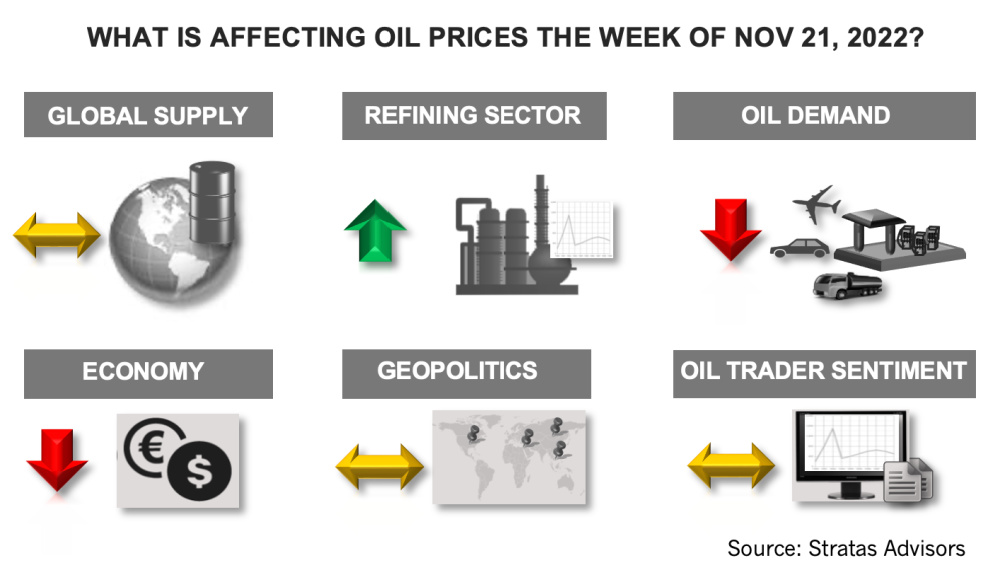

The price of Brent crude ended the week at $87.74 after closing the previous week at $95.99. The price of WTI ended the week at $80.11 after closing the previous week $88.96.

For the last couple of months, we have been putting forth the view that the price of Brent crude would be around $90 during the fourth quarter of this year. Additionally, we expect that the price of Brent crude will remain, for the most part, in the channel between $85 and $95 because of upside resistance coupled with downside support. The upside resistance stems from the weakening and fragile economic conditions, which is translating into muted oil demand growth. The downside support stems from the relatively tight oil supply conditions. While there is sufficient supply to prevent oil prices from breaking out to higher levels, we are forecasting that oil demand will slightly outpace oil supply during the fourth quarter by around 240,000 bbl/d, excluding any changes pertaining to inventories held in strategic reserves. (In first-quarter 2023, we are forecasting that there will be a shift to a slight surplus with supply outpacing demand in first-quarter 2023 and continue to do so throughout 2023). Additionally, there is some uncertainty about the security of supply with the U.S. and its G7 allies continuing to contemplate the implementation the imposition of additional sanctions. While we think the additional sanctions (including a price cap) will be of limited effectiveness (as we have been previously highlighting, including in last week’s note), the uncertainty provides the basis for a risk premium, which otherwise would not be part of oil prices.

While not directly affecting oil prices in the short-term, COP 27 being held in Egypt ended on Nov. 20 with some interesting developments, including the following:

- A fund is to be created to support nations that are vulnerable to climate with the funds to be provided by existing financial institutions

- The funds are not expected to be established for several years, in part, because the agreement does not include details on major items such as which party will be responsible for overseeing the fund

- Limited progress was made in updating national climate targets and there is no language pertaining to achieving the objective of emissions peaking before 2025

- Additionally, it appears that the setting of targets will shift back to a five-year cycle and away from the annual process agreed to at COP 26

- There is also no commitment to phase out fossil fuels with the nations agreeing only to accelerating efforts to phase out unabated coal power and inefficient fuel subsidies

- Some participants have expressed a concern about the potential of using low-emissions energy, such as natural gas, which would still contribute to the emissions of CO₂ and methane

The above developments highlight the difficulty of balancing the need to support economic activity, while addressing the objective of reducing emissions.

For a complete forecast of refined products and prices, please refer to our Short-term Outlook.

About the Author: John E. Paise, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

E&P Highlights: March 11, 2024

2024-03-11 - Here’s a roundup of the latest E&P headlines, including a new bid round offshore Bangladesh and new contract awards.

E&P Highlights: March 25, 2024

2024-03-25 - Here’s a roundup of the latest E&P headlines, including a FEED planned for Venus and new contract awards.

Deepwater Roundup 2024: Americas

2024-04-23 - The final part of Hart Energy E&P’s Deepwater Roundup focuses on projects coming online in the Americas from 2023 until the end of the decade.

Deepwater Roundup 2024: Offshore Australasia, Surrounding Areas

2024-04-09 - Projects in Australia and Asia are progressing in part two of Hart Energy's 2024 Deepwater Roundup. Deepwater projects in Vietnam and Australia look to yield high reserves, while a project offshore Malaysia looks to will be developed by an solar panel powered FPSO.

Exxon Mobil Green-lights $12.7B Whiptail Project Offshore Guyana

2024-04-12 - Exxon Mobil’s sixth development in the Stabroek Block will add 250,000 bbl/d capacity when it starts production in 2027.