Brent rose $1.11/bbl last week to average $71.61/bbl while WTI rose only $0.12/bbl to average $62.09/bbl. The disparity in the price changes show that concerns were broad-based and likely more geopolitical than fundamental.

For the week ahead we expect Brent to be generally range-bound and average closer to $71/bbl on news out of OPEC, concerns about U.S. crude builds, and ongoing trade tensions with China.

Topic of Interest

Reports from this weekend’s Joint Ministerial Monitoring Committee meeting have been mixed. Initial reports indicated that OPEC and its allies are considering raising production levels in the second-half of the year. While an official decision won’t be made until June, Russia has been quite vocal all year in its desire to raise production. At the same time, many members remain wary of a potential price drop if production is increased, similar to the one seen in mid-2018. And in the last 24 hours representatives for Saudi Arabia and the UAE have both come out as opposed to a production increase. Stratas Advisors currently expects OPEC production to gradually rise in the latter-half of the year as a result of lower compliance from deal signatories. Other options could include an official decision to raise production or an agreement to reduce over-compliance.

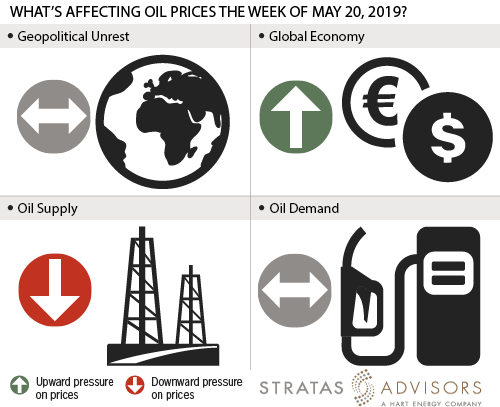

Geopolitics: Neutral

Geopolitics will be a neutral factor in the week ahead. Tensions remain high in the Middle East, but with no new developments, there is no incentive to price in further risk.

Global Economy: Positive

The global economy will be a positive factor in the week ahead. The White House’s decision not to impose auto tariffs as well as the agreement on metals tariffs with Mexico and Canada has somewhat reassured investors about the state of the global economy but negotiations with China are ongoing.

Oil Supply: Negative

Supply will be a negative factor in the week ahead. Despite chatter around OPEC, oversupply concerns remain almost entirely focused on potential U.S. production, as evidenced in the divergence between WTI and Brent price movements last week.

Oil Demand: Neutral

While strong, oil demand is likely to be a neutral factor in the week ahead. Margins globally are generally below their seasonal averages for this time of year. However, utilization is still high. In the U.S., utilization was 90.5% in the second week of May. Even with strong runs, utilization is below last year’s levels, leaving room to increase if price support appears.