Brent prices averaged $64.95/bbl last week, gaining strength at the end of the week. This week prices will likely remain range-bound, averaging $65/bbl with the Brent-WTI differential remaining about $3.50/bbl.

Geopolitical - Neutral

There is minimal news on the geopolitical front that is likely to influence prices this week. While perennial issues such as the decline in Venezuela and unrest in Libya remain, we do not expect them to become more impactful in the short term.

Dollar - Neutral

Fundamental and sentiment-related drivers continue to have more impact on crude oil prices. The dollar moved sideways last week as crude oil rose slightly. Crude oil will likely remain only marginally influenced by DXY in the week ahead.

Trader Sentiment - Positive

ICE Brent and Nymex WTI managed money net positioning both fell slightly last week. Short-selling also indicates that producer level hedging has ticked up in recent weeks as producers take full advantage of recently high prices before a possible correction. Trader sentiment remains generally positive despite recent increases in U.S. production.

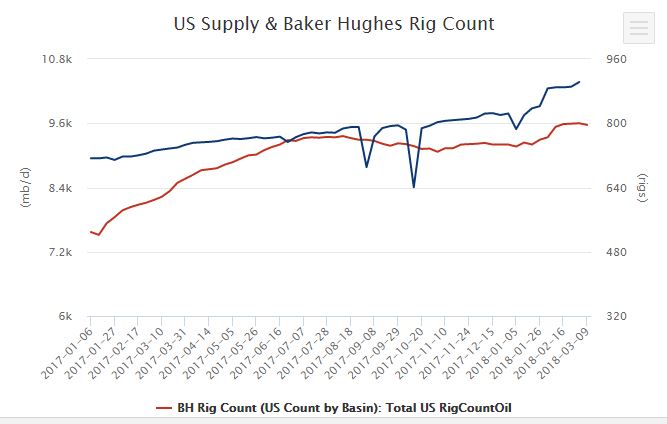

Supply – Negative

According to Baker Hughes, the U.S. rig count fell for the first time in six weeks last week. Such fluctuations in rig numbers are common and we do not believe this is the start of a trend. We continue to expect that the impact on production of these rising rigs will likely start to be seen in May. Libya has been having trouble keeping fields online in recent weeks due to protests, which has reduced production slightly. Evidence of renewed global oversupply continues to pose the greatest threat to prices.

Demand – Positive

U.S. consumption of petroleum products remains generally at or above seasonal averages in all products except fuel oil.

Refining – Neutral

Global refining margins fell across the board last week with the largest decline seen on the U.S. Gulf Coast. Declines in margins appear to be slowing, and we could even see some strengthening in margins in the weeks ahead as Asian refinery maintenance is underway. However, in the meantime, margins are not robust enough to incentivize additional runs of a level likely to support crude.

How We Did

Recommended Reading

AI Poised to Break Out of its Oilfield Niche

2024-04-11 - At the AI in Oil & Gas Conference in Houston, experts talked up the benefits artificial intelligence can provide to the downstream, midstream and upstream sectors, while assuring the audience humans will still run the show.

Going with the Flow: Universities, Operators Team on Flow Assurance Research

2024-03-05 - From Icy Waterfloods to Gas Lift Slugs, operators and researchers at Texas Tech University and the Colorado School of Mines are finding ways to optimize flow assurance, reduce costs and improve wells.

Defeating the ‘Four Horseman’ of Flow Assurance

2024-04-18 - Service companies combine processes and techniques to mitigate the impact of paraffin, asphaltenes, hydrates and scale on production — and keep the cash flowing.

Axis Energy Deploys Fully Electric Well Service Rig

2024-03-13 - Axis Energy Services’ EPIC RIG has the ability to run on grid power for reduced emissions and increased fuel flexibility.

StimStixx, Hunting Titan Partner on Well Perforation, Acidizing

2024-02-07 - The strategic partnership between StimStixx Technologies and Hunting Titan will increase well treatments and reduce costs, the companies said.