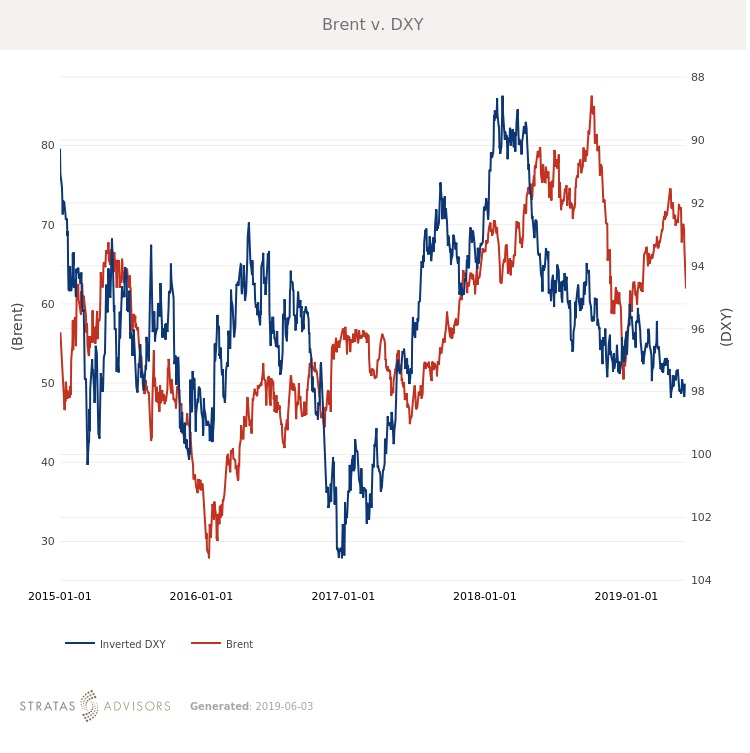

In the week since our last edition of What’s Affecting Oil Prices, the weekly average Brent price fell $2.11/bbl last week to average $68.21/bbl. WTI fell even more sharply, down $3.80/bbl to average $57.01/bbl. Both crudes lost more than $5/bbl from their prices at the start of last week as sentiment swiftly turned against crude. The disparity in price movements of US and international crudes continues to show that concerns are broad-based and not rooted in fundamental changes.

Stratas Advisors has expected these oscillations for some time now, and a common theme in these weekly analyses has been that the longer a bull or bear run lasts without fundamental support, the more severe the “corrections” will be. We expect prices will continue to fall, albeit less dramatically this week, with Brent averaging $61/bbl as markets seek a floor.

On the demand side, economic concerns remain front of mind. The tariff dispute with China continues to drag on, and shipments entering both countries are now subject to increased costs. Adding to the difficulty in securing a deal, after Chinese telecom company Huawei was effectively banned in the U.S., Beijing has threatened to issue similar bans on a list of American companies. And at the end of last week, President Trump made a surprise announcement that imports from Mexico could be subject to an escalating 5% tariff (with a potential cap at 25%) if the Mexican government did not do more to stem the flow of immigrants to the US.

Senior Mexican officials are meeting with their White House counterparts this week to discuss the threat and possible solutions. While the tariffs themselves certainly have implications for trade, they also underline the uncertainty in dealing with the current administration. The tariff announcement was made with no reference to the revised NAFTA agreement that is currently being reviewed by the Canada, Mexico, and U.S. governments.

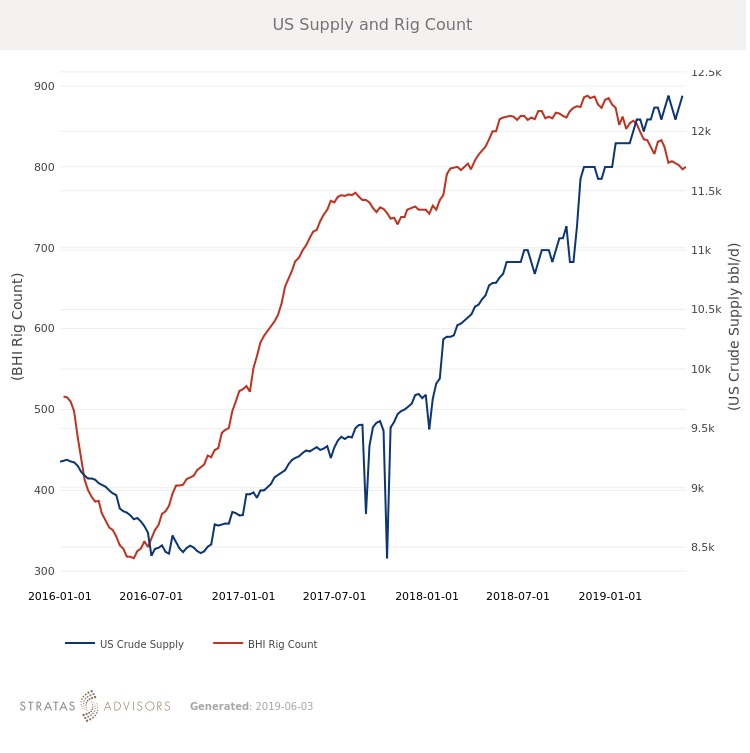

After last week’s severe price correction, Saudi Arabia and other OPEC members quickly provided assurances that any production increase would only be decided once markets were decisively balanced. Elsewhere on the supply side, not much has changed in a week. This week could see flows of Urals start to resume as the refineries affected by the Druzbha pipeline contamination have come to a sharing agreement for what to do with the contaminated crude.

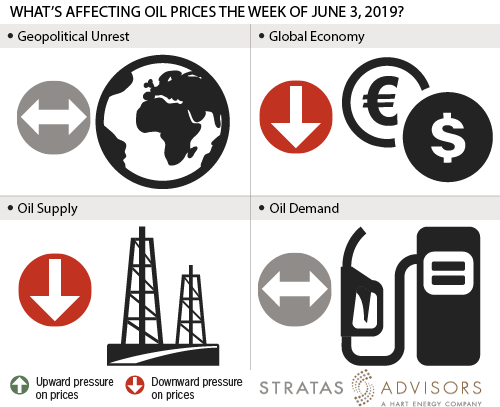

Geopolitics: Neutral

Global Economy: Negative

Oil Supply: Negative

Oil Demand: Neutral

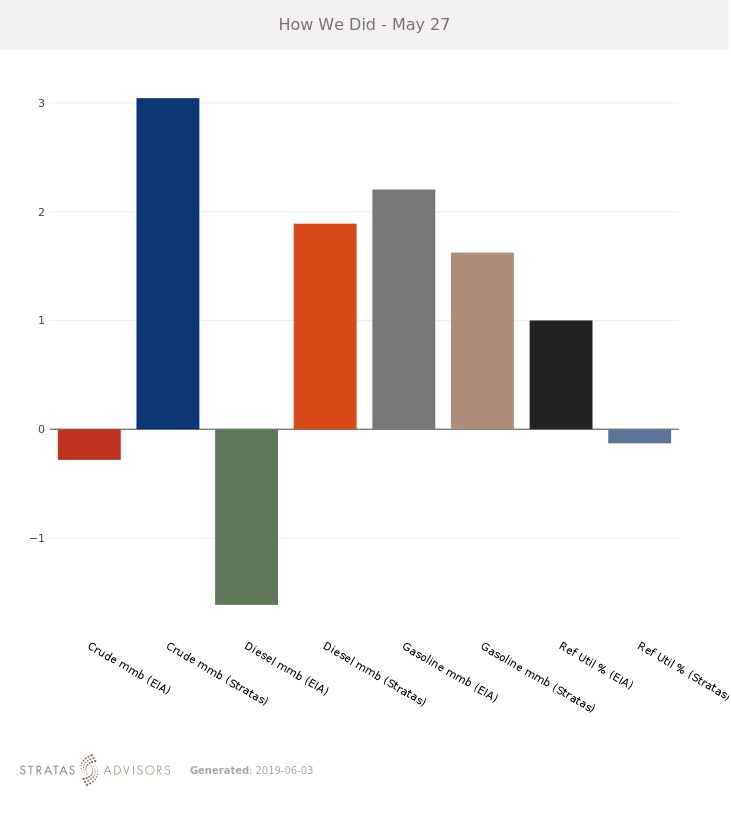

How We Did

Recommended Reading

Biden Administration Hits the Brake on New LNG Export Projects

2024-01-26 - As climate activists declare a win, the Department of Energy secretary says the pause is needed to update current policy.

Rystad Sees Little Support for Henry Hub in Coming Weeks

2024-01-26 - Rystad Energy sees little support for Henry Hub prices in the U.S. as dry gas production rises after the Jan. 17 Arctic freeze that impacted all of the Lower 48 states.

Baker Hughes Detects LNG Slowdown Solutions, Global Opportunities

2024-01-26 - Baker Hughes’ fourth quarter earnings call confronts Biden’s halt on LNG permitting with “solve itself” attitude.

Texas LNG Export Terminal Completes Required Permitting for FID

2024-01-26 - Glenfarne expects the Texas LNG project’s commercialization to be completed in the first half of 2024.

What's Affecting Oil Prices This Week? (Jan. 29, 2024)

2024-01-29 - For the upcoming week, Stratas Advisors forecast that increase in oil prices will be moderated likely due to the U.S. being cautious in response to the recent attack on U.S. troops.