Learn more about Hart Energy Conferences

Get our latest conference schedules, updates and insights straight to your inbox.

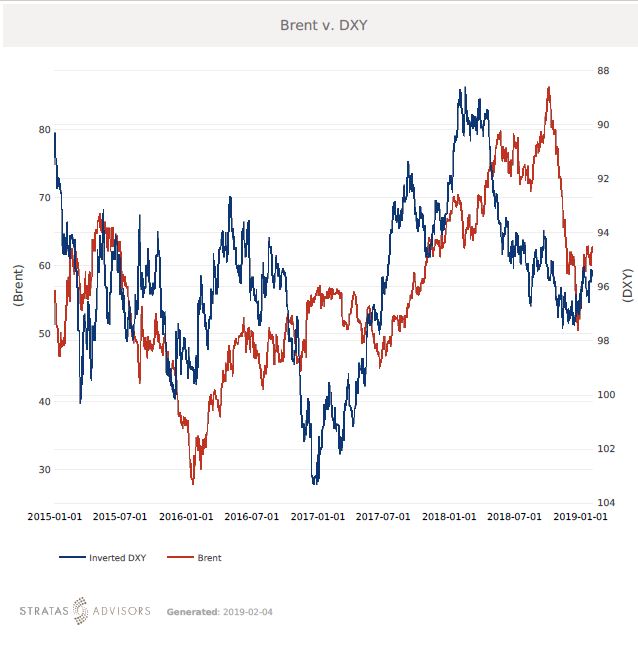

In the weeks since the last edition of What’s Affecting Oil Prices, Brent fell $0.11/bbl last week to average $61.51/bbl.

However, the news wasn’t all bad as much of the drop was actually driven by a sharp downward price move on Jan. 28 and by Feb. 1 Brent closed at $62.75/bbl—on track for our $63/bbl forecast, but a few days too late. WTI was a similar story, although it did in fact follow our forecast and close the week at $55.26/bbl. For the week ahead we see continued strength in prices, and again expect to see Brent averaging $63/bbl and WTI averaging $54/bbl or better.

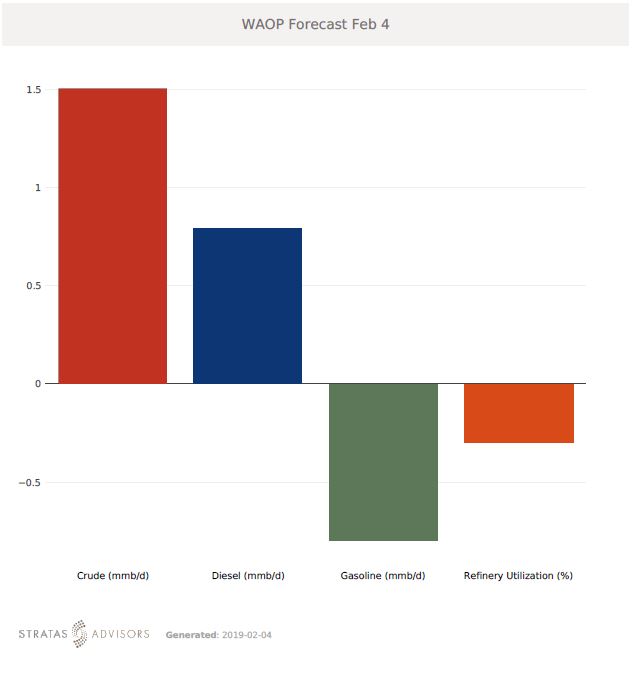

In the U.S., crude runs continue to seasonally decline, but likely builds in crude stocks will be offset by expected declines in product stocks. The situation in Venezuela continues to bear watching due to its implications for North American heavy crude oil flows but for the moment, developments are mainly political in nature, with limited physical impact.

Also worth mentioning, immigration negotiations to avert another government shutdown appear to be making very little progress. While we continue to think it unlikely that a full shutdown will resume in two weeks, we are raising our internal estimates of the likelihood of another partial shutdown. We also continue to watch for progress on trade negotiations between the U.S. and China. While Friday’s (Feb. 1) announcements were more positive than expected, at this point tariffs have been in place long enough that economic data out of China is more relevant.

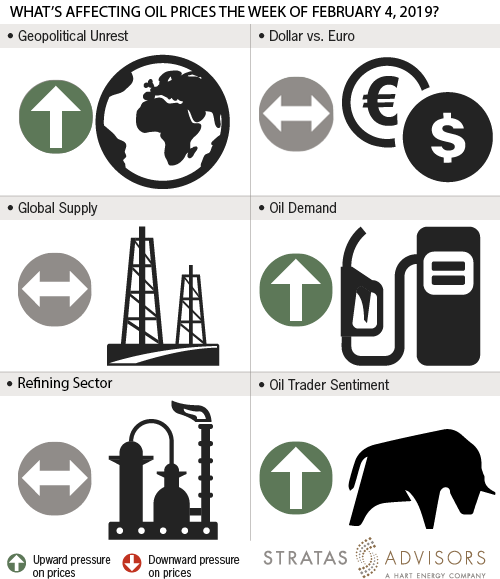

Geopolitical: Positive

Dollar: Neutral

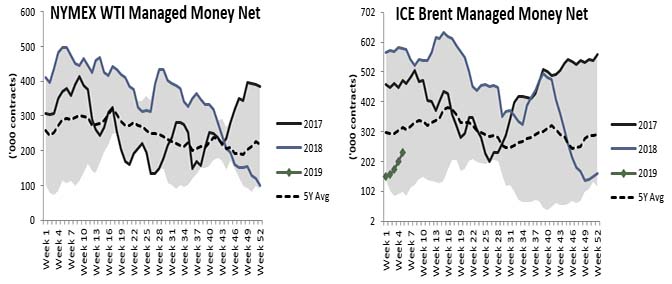

Trader Sentiment: Positive

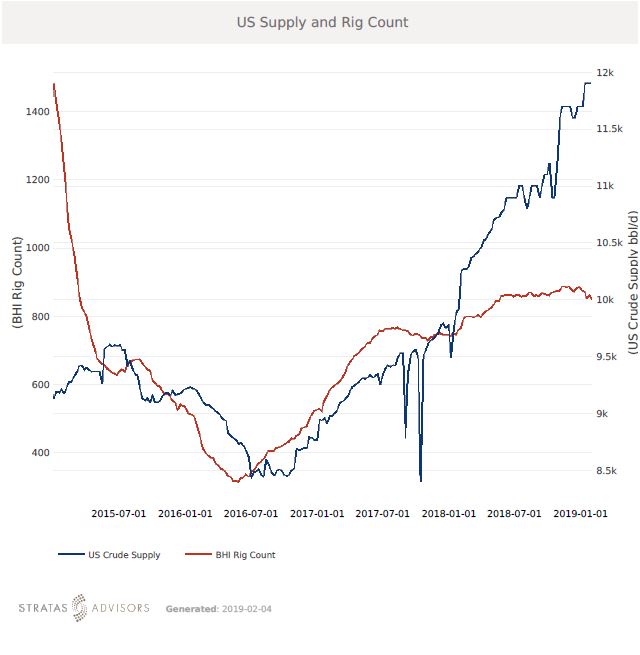

Supply: Neutral

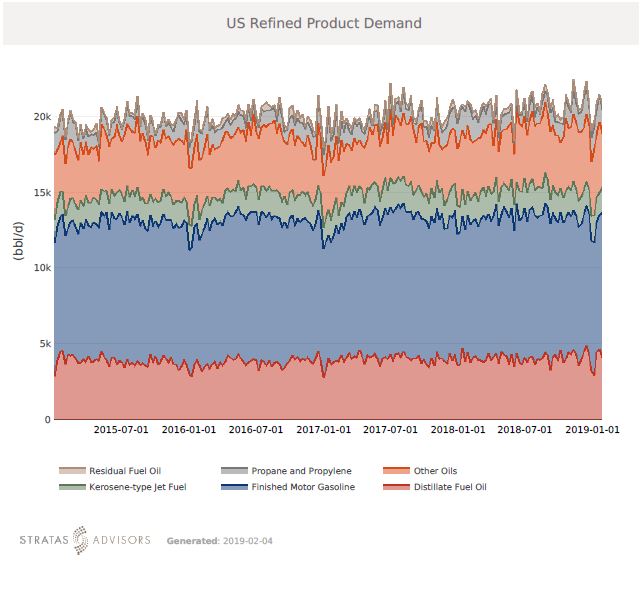

Demand: Positive

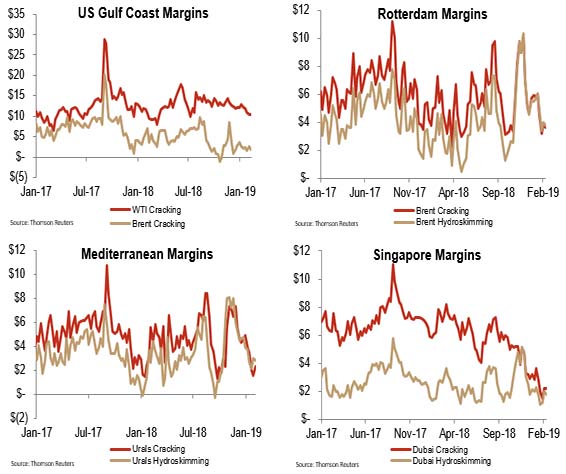

Refining Margins: Neutral

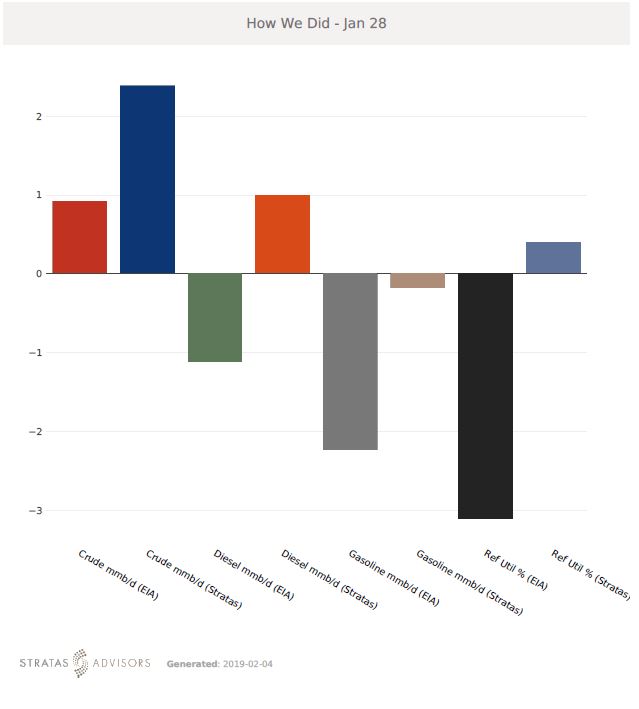

How We Did

Recommended Reading

Buffett: ‘No Interest’ in Occidental Takeover, Praises 'Hallelujah!' Shale

2024-02-27 - Berkshire Hathaway’s Warren Buffett added that the U.S. electric power situation is “ominous.”

CEO: Magnolia Hunting Giddings Bolt-ons that ‘Pack a Punch’ in ‘24

2024-02-16 - Magnolia Oil & Gas plans to boost production volumes in the single digits this year, with the majority of the growth coming from the Giddings Field.

Petrie Partners: A Small Wonder

2024-02-01 - Petrie Partners may not be the biggest or flashiest investment bank on the block, but after over two decades, its executives have been around the block more than most.

Occidental Increases Annual Dividend by 22%

2024-02-11 - Occidental Petroleum Corp.’s newly declared dividend is at an annual rate of $0.88 per share, compared to the previous annual rate of $0.72 per share.

Matador Stock Offering to Pay for New Permian A&D—Analyst

2024-03-26 - Matador Resources is offering more than 5 million shares of stock for proceeds of $347 million to pay for newly disclosed transactions in Texas and New Mexico.