Stratas Advisors expects that oil prices will continue to be volatile based on several factors including constrained oil supply, ongoing negotiations for a nuclear deal with Iran, tepid growth frin the U.S. economy and more. (Source: Shutterstock.com)

Editor’s note: This report is an excerpt from the Stratas Advisors weekly Short-Term Outlook service analysis, which covers a period of eight quarters and provides monthly forecasts for crude oil, natural gas, NGL, refined products, base petrochemicals and biofuels.]

The price of Brent crude ended the week at $96.72 after closing the previous week at $98.15. The price of WTI ended the week at $90.77 after closing the previous week $92.09.

Last week, we highlighted our expectations for heightened volatility because of the uncertainty pertaining to macroeconomic and geopolitical developments coupled with the fragility of the supply/demand fundamentals. The price movement of last week reinforced those expectations with the price of Brent crude starting the week at $98.15 then falling to $92.34 before rebounding to $96.72 at the end of the week.

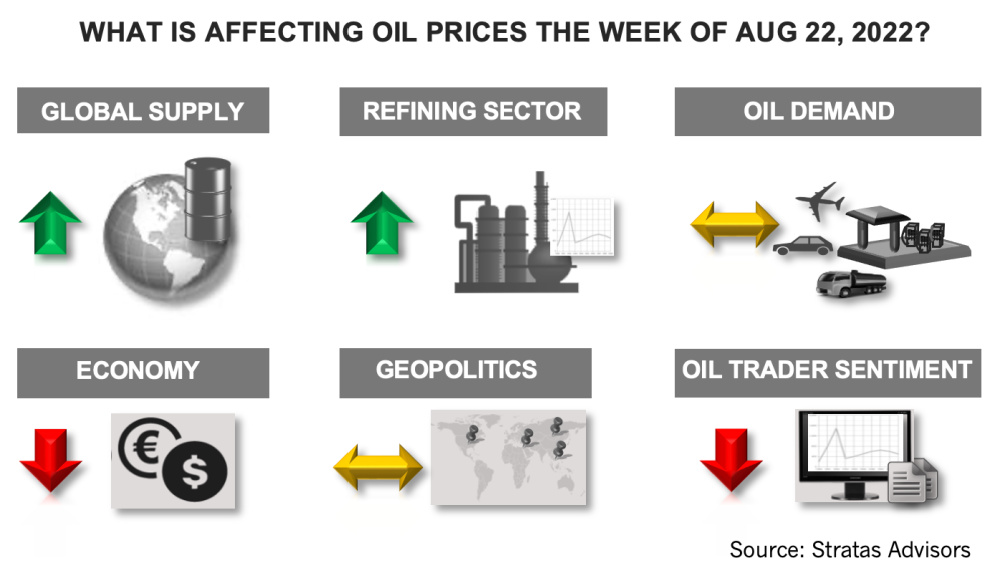

Looking forward to the upcoming week, we are expecting that oil prices will continue to be volatile based on the following factors.

- Oil supply remains constrained with U.S. production moving up slowly, while commercial inventories are running below the pre-COVID levels, even with the ongoing releases from the Strategic Petroleum Reserve (SPR). Since the beginning of the year, inventories in the SPR have decreased by 133 million barrels, while commercial inventories have increased by only 12 million barrels. Additionally, other developments across the globe are not helping the supply situation. Africa production continues to be a mixed bag with more positive news coming out of Libya with Libya’s production reaching 1.21 million bbl/d, while Nigeria’s production falling to 1.08 million bbl/d and below the production of Angola’s production of 1.18 million bbl/d. While there has been some increased production in the Middle East, as illustrated by Iraq, increasing its production by 100,000 bbl/d in July, a majority of increased supply is being used for domestic power generation. Venezuela has recently suspended crude oil shipments to Europe that had restarted in May after the U.S. Treasury Department granted limited licenses to Italy’s Eni SpA and Spain’s Repsol SA to implement oil-for-debt swap arrangements. Since June, Eni has received 3.6 million barrels and Repsol has received about 3 million barrels of diluted crude oil from Venezuela. Now, however, Venezuela wants refined fuel in exchange for the crude oil, but at this time the EU has no plans to shift away from the oil-for-debt to oil-for-refined products.

- Last week, we reiterated our view that a nuclear deal with Iran remains unlikely, even with the ongoing negotiations. We are still holding to that view, in part, because we think it would be very difficult for the Biden Administration to sell such a deal to members of congress and voters. Our view is also supported by the Biden Administration assuring Israel last week that concessions are not being offered to Iran and that a deal is not imminent. The Russia—Ukraine conflict continues, and as we have been highlighting—the longer the conflict continues the greater the risk of escalation and expansion—and the greater the risk of disruptions of energy shipments. Last week, there were Ukrainian attacks in Crimea, which has been under the control of Russia since 2014. The attacks were executed using drones including an attack on the Saki air base. The question now is what Russia’s response will be to these attacks and to more weapons being shipped to Ukraine.

- The U.S. economy continues to exhibit signs of tepid growth. The leading economic index provided by the Conference Board declined in July by 0.4% after declining by 0.7% in June—and now has declined for five consecutive months. Additionally, the U.S. personal savings rate has fallen to 5.1%, which is materially below the average of the decade before COVID-19, when the savings rate averaged around 7.0%. Furthermore, the housing market continues to experience a steep decline with construction starts falling to the slowest pace since 2021 and existing home sales declining for the six-consecutive month to the lowest level since 2020. The GDP Nowcast provided by the Federal Reserve Bank of Atlanta is showing that U.S. GDP growth rate for the third quarter stands at 1.6%. A concern we have been voicing for several months is the possibility of the U.S. Federal Reserve overreacting to the inflation data, in part, because many factors underlying the elevated inflation are not factors that can be addressed by monetary policy—unless the Federal Reserve is willing to push the economy into a recession. And this remains a concern, given that the latest noise out the Federal Reserve indicates heightened focus on wage increases. However, we think that continued higher wage increases, and aggressive hiring is unlikely, given that labor productivity declined in the U.S. declined by 4.6% in the second quarter after declining by 7.4% in the first quarter. As such, from our perspective, it is unlikely that the U.S. will get caught in a wage-price spiral. Meanwhile, the U.S. dollar strengthened significantly, as indicated by the U.S. Dollar Index increasing from 105.63 to 108.12, which puts downward pressure on commodity prices, including crude oil.

- Outside of the U.S., Europe is still dealing with drought-related issues which is affecting shipping on the Rhine and Danube, while facing extremely high natural gas prices, which have doubled since June. The increasing energy prices are also pushing up inflation even though the European economy is slowing down and the German central bank is warning that the inflation rate will exceed 10%. Furthermore, while Germany has reached its initial goal of increasing gas storage to 75% of capacity, the target of 85% by Oct. 1 and 95% by November will be challenging with Russia reducing flows associated with Nord Stream 1 to only 20% of agreed volumes. Consequently, Germany is looking to ration gas supplies to reduce demand by 20%. Since industry represents around 25% of natural gas demand and around 30% of Germany’s economy, the impact on economic growth will be significant. China’s economy is also being affected by drought conditions, which is resulting in power shortages because of reduced hydropower production in the Yangtze River Basin. The Sichuan province, which is a major agricultural region, as well as manufacturing center (heavy industry and light industry) is being especially affected.

- In our latest quarterly update of our global outlook of the oil markets, we are forecasting that global oil demand in the third quarter will increase by 1.8 million bbl/d in comparison to the second quarter of this year. Oil demand is expected to grow during the second half of 2022, and in the fourth quarter is forecasted to reach 101.8 million bbl/d. On average, we are forecasting that global demand will increase by 2.63 million bbl/d in 2022.

- Refining sector continues to enjoy relatively high margins with the U.S. having the highest margins. Product inventories remain tight—particularly diesel/gasoil inventories. Diesel inventories in the U.S. are 23.26 million barrels less than for the same period in 2019 and are running around 20% below the seasonal 5-year average.

- Crude oil traders continue to reduce their net long positions. Last week, traders of WTI crude decreased their net long positions for the fourth consecutive week. Consequently, net long positions remain at the lowest level since April 2020. Traders of Brent crude also decreased their net long positions last week by reducing their long positions, while adding to their short positions.

About the Author: John E. Paise, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

President: Financial Debt for Mexico's Pemex Totaled $106.8B End of 2023

2024-02-21 - President Andres Manuel Lopez Obrador revealed the debt data in a chart from a presentation on Pemex at a government press conference.

Hess Corp. Boosts Bakken Output, Drilling Ahead of Chevron Merger

2024-01-31 - Hess Corp. increased its drilling activity and output from the Bakken play of North Dakota during the fourth quarter, the E&P reported in its latest earnings.

The OGInterview: Petrie Partners a Big Deal Among Investment Banks

2024-02-01 - In this OGInterview, Hart Energy's Chris Mathews sat down with Petrie Partners—perhaps not the biggest or flashiest investment bank around, but after over two decades, the firm has been around the block more than most.

Petrie Partners: A Small Wonder

2024-02-01 - Petrie Partners may not be the biggest or flashiest investment bank on the block, but after over two decades, its executives have been around the block more than most.

From Restructuring to Reinvention, Weatherford Upbeat on Upcycle

2024-02-11 - Weatherford CEO Girish Saligram charts course for growth as the company looks to enter the third year of what appears to be a long upcycle.