In the week since our last edition of What’s Affecting Oil Prices, Brent crude fell 32 cents/bbl week-close to week-close. For the week ahead Stratas Advisors expects prices to average $53/bbl as the adage “no news is good news” holds true. With only one upcoming data release, there will be little news to counter currently bullish sentiment. The supporting rationale for the forecast is provided below.

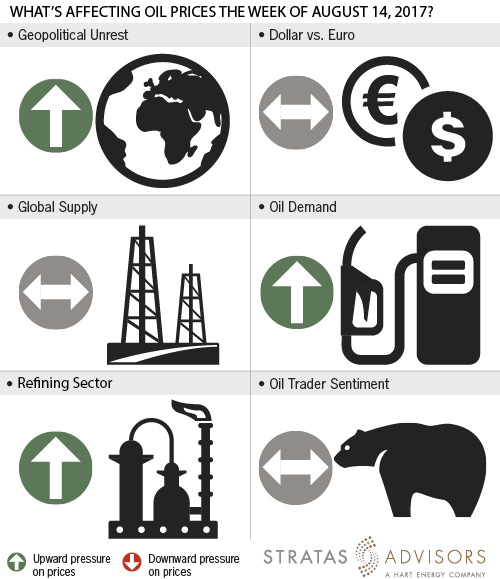

Geopolitical: Positive

Geopolitics, as it relates to oil, will continue to drive volatility but is unlikely to have an immediate fundamental impact. However, the few active hotspots that bear watching are more likely to hamper oil supply, helping prices. In Nigeria, protestors have occupied a crude oil facility and gas plant owned by Shell demanding jobs and infrastructure improvements. Flows from the facility were already reduced due to an outage on the Trans Niger Pipeline, but if the occupation is long-lived it could impact future volumes. Venezuela’s slow collapse remains a perennial issue, but there have been no new developments to indicate a timeline.

Dollar: Neutral

Given the substantial impact on prices from fundamentals and sentiment, the DXY and the USD/EUR exchange rate are still not as impactful as they have previously been. The dollar fell last week on soft inflation data as the Euro rose. Given that crude also fell, this is evidence that the inverse relationship is still extremely weak in light of overwhelming fundamental influences on crude.

Trader Sentiment: Neutral

Trader sentiment will be a neutral factor in the week ahead as Brent has backed off of overbought levels. While traders will remain sensitive to any negative fundamental data, the only relevant data release next week is the weekly EIA report minimizing chances for upset. The IEA and OPEC monthly reports last week reaffirmed current bullish sentiment. NYMEX and ICE WTI Managed Money net longs both fell last week, 2,253 and 380 contracts respectively. ICE Brent Managed Money net longs increased 58,255 contracts as shorts fell 18,644.

Supply: Neutral

Last week the number of operating oil rigs in the U.S. increased by three, according to the weekly report from Baker Hughes. U.S. oil rigs now stand at 768 compared to 396 at the same time last year. In the latest weekly estimates from the U.S., domestic crude production fell on declines out of Alaska. There was little concrete news out of the joint OPEC/non-OPEC meeting last week besides reiterations of how committed the deal participants were. In general, with no new supply news there is little to push markets down.

Demand: Positive

Demand continues to help support crude prices. The IEA’s report reiterated their bullish demand outlook, with reported numbers lending credence. In the U.S., distillate and propane demand increased sharply in last week’s report. ARA total product stocks fell with gasoline and distillate both seeing draws.

Refining: Positive

Margins increased in every enclave last week, potentially leading to another week of increased runs this week. In the U.S., the WTI crack at the Gulf Coast hit another new high for the year, $14.25/bbl. In Singapore, the Dubai cracking margin also hit a new high for the year at $8.08/bbl. While there are reports that Chinese runs have slowed in recent months, they still remain above last year’s healthy levels. Global refinery outages are currently fairly subdued despite scattered small upsets (e.g. Shell’s Convent facility, Paz Group’s Ashdod facility).

For the upcoming week, Stratas Advisors is expecting that crude inventories will see draw, in line with seasonal norms. Crude stocks in the U.S. are expected to fall approximately 2 million to 3 million barrels as runs remain strong. Stratas Advisors also expect the Brent-WTI differential will continue to hover around $3/bbl as Brent’s gains slightly outpace WTIs.

Recommended Reading

US Gulf Coast Heavy Crude Oil Prices Firm as Supplies Tighten

2024-04-10 - Pushing up heavy crude prices are falling oil exports from Mexico, the potential for resumption of sanctions on Venezuelan crude, the imminent startup of a Canadian pipeline and continued output cuts by OPEC+.

What's Affecting Oil Prices This Week? (Feb. 26, 2024)

2024-02-26 - Stratas Advisors forecast that global crude production will be essentially unchanged from 2023, which means that demand growth in 2024 will outpace supply growth.

Oil Settles at Highest in Nearly 8 Weeks on Strong Economic Growth

2024-01-26 - Oil prices settled at their highest in nearly two months on Jan. 26 as positive U.S. economic growth and signs of Chinese stimulus boosted demand expectations.

US Oil Stockpiles Surge as Prices Dip, Production Remains Elevated

2024-02-14 - EIA reported crude oil stocks increased by 12.8 MMbbl as February began, far outstripping expectations.

Oil Broadly Steady After Surprise US Crude Stock Drop

2024-03-21 - Stockpiles unexpectedly declined by 2 MMbbl to 445 MMbbl in the week ended March 15, as exports rose and refiners continued to increase activity.