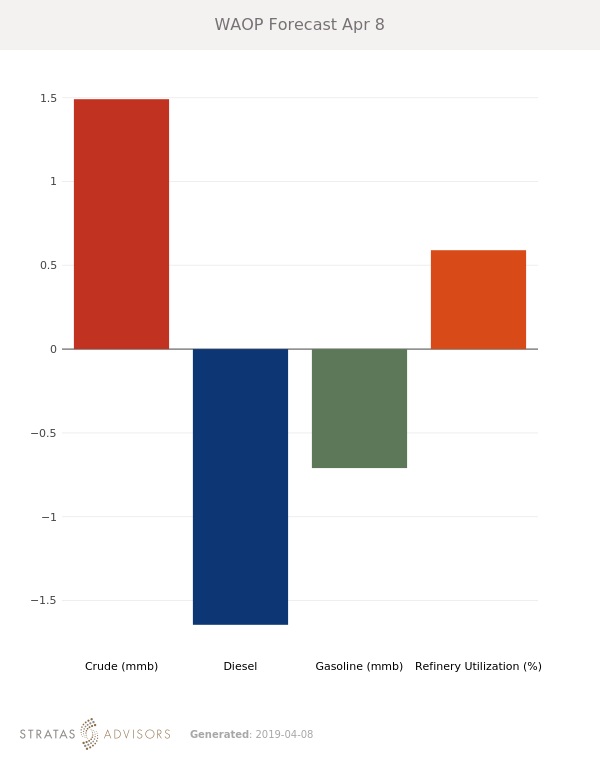

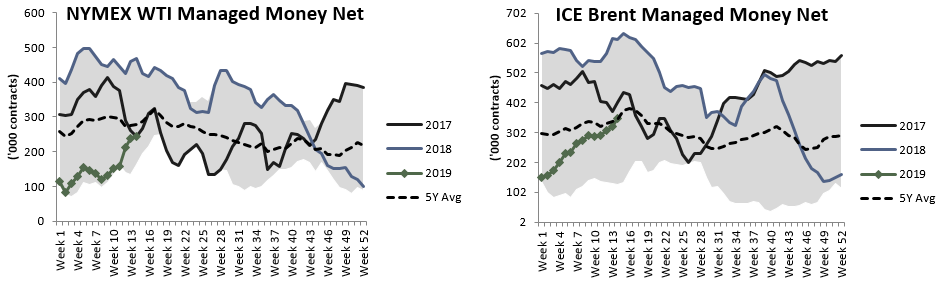

In the week since our last edition of What’s Affecting Oil Prices, Brent rose $1.64/bbl last week to average $69.49/bbl, which was above our expectations. WTI rose $2.84/bbl to average $62.36/bbl. This was Brent’s second straight week of gains and WTI’s fifth week. Moves in managed money were positive but smaller than in previous weeks. For the week ahead, Brent is likely to see additional strength, but the psychological $70/bbl barrier could be too much to sustainably overcome, and we expect Brent to average closer to $71.50/bbl.

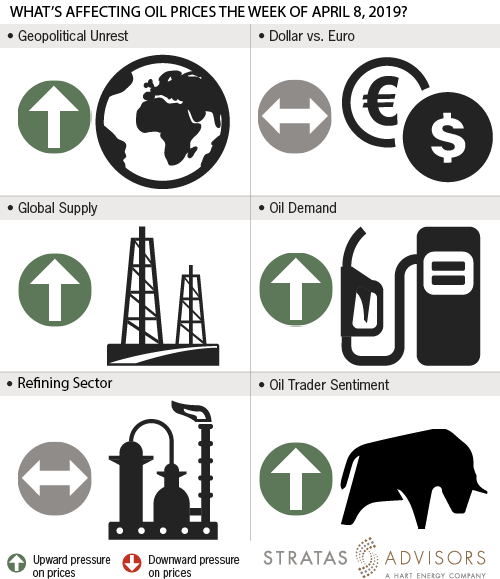

Friday (April 5) saw strong U.S. employment data, further easing fears about demand. Non-farm payrolls increased 196,000 jobs in March. Wages increased 0.1% after February’s 0.4% increase, bringing the annual increase to 3.2%. If wages were to increase too quickly, it could stoke fears about inflation and a rate increase from the Federal Reserve.

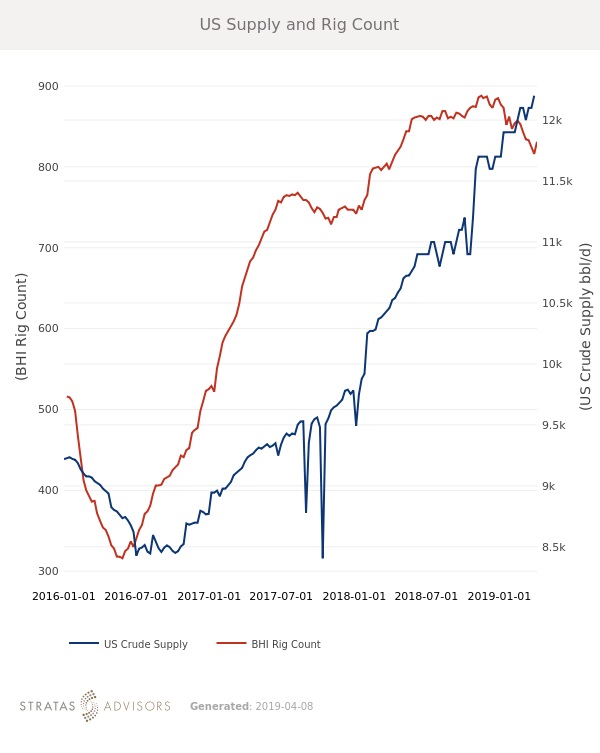

On the supply side, several developments are afoot. Violence in Libya is again escalating, disrupting supplies. General Haftar has escalated his campaign against the internationally recognized government and ordered his forces to march on Tripoli. Haftar hopes to unite Libya under a singular government, led by him. Additionally, the U.S. has targeted Venezuelan oil shipments to Cuba in an effort to further restrict income to the Maduro regime. These interruptions, on top of a stronger demand outlook, appear to have been enough to counteract the first increase in drilling rigs seen in seven weeks.

The “No Oil Producing and Exporting Cartels Act” was recently introduced in Congress. While the legislation has only a small chance of actually passing, Saudi Arabian officials have come out vehemently against such legislation. Debates around the legislation and what it means for the upcoming OPEC+ meeting could inject uncertainty into markets.

Geopolitical: Positive

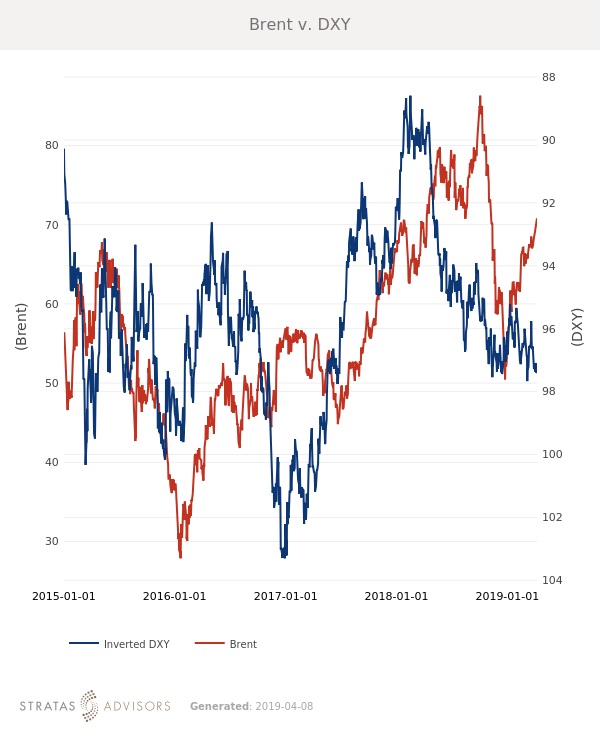

Dollar: Neutral

Trader Sentiment: Positive

Supply: Positive

Demand: Positive

Refining: Neutral

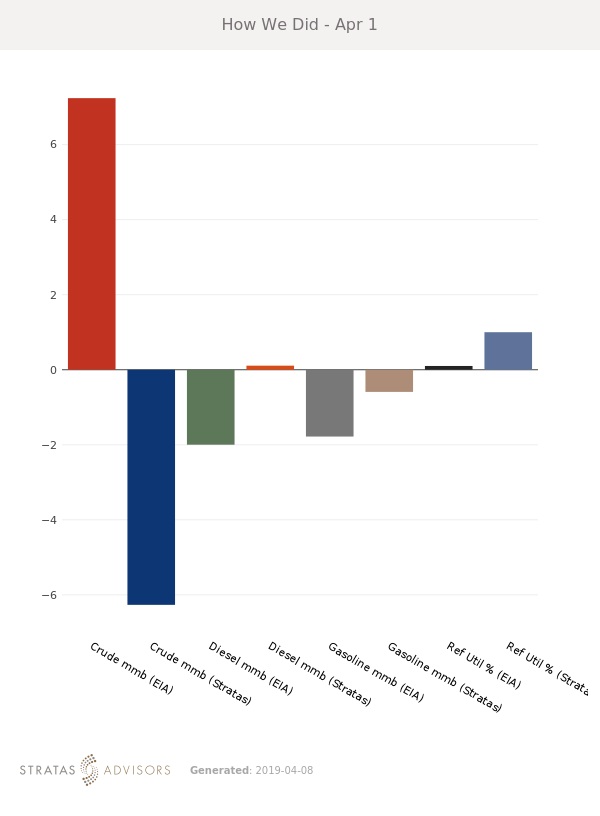

How We Did

Recommended Reading

Chevron, Brightmark JV Opens RNG Facility in Arizona

2024-04-10 - Eloy RNG produces RNG using anaerobic digesters at the Caballero Dairy in Arizona, Brightmark said April 10.

Collaboration, not ‘Mythical’ Renewables will Solve Climate Crisis

2024-03-25 - Tinker Energy Associates CEO Scott Tinker is optimistic that a combination of passion, expertise and funding can solve the world’s existential crisis—if the right questions are asked.

Energy Transition in Motion (Week of April 12, 2024)

2024-04-12 - Here is a look at some of this week’s renewable energy news, including a renewable energy milestone for the U.S.

Summit Carbon Solutions, POET Partner on CCS Project

2024-02-07 - The partnership will incorporate POET’s 12 facilities in Iowa and five facilities in South Dakota into Summit’s carbon capture and storage project.

Kraft Heinz, Carlton Power Partner to Develop Green Hydrogen Plant

2024-02-05 - Located at Kraft Heinz’s Kitt Green manufacturing plant in Wigan, Greater Manchester, the proposed $50.1 million plant will have a 20-megawatt capacity.