The risk of COVID-19 cases extends past India since there are numerous countries in Asia and other regions that have been slow in ramping up their vaccination programs, according to Stratas Advisors. (Source: Shutterstock.com)

[Editor’s note: This report is an excerpt from the Stratas Advisors weekly Short-Term Outlook service analysis, which covers a period of eight quarters and provides monthly forecasts for crude oil, natural gas, NGL, refined products, base petrochemicals and biofuels.]

The price of Brent crude oil ended the week at $66.11 after closing the previous week at $66.77, while the price of WTI ended the week at $62.14 after closing the previous week at $63.13.

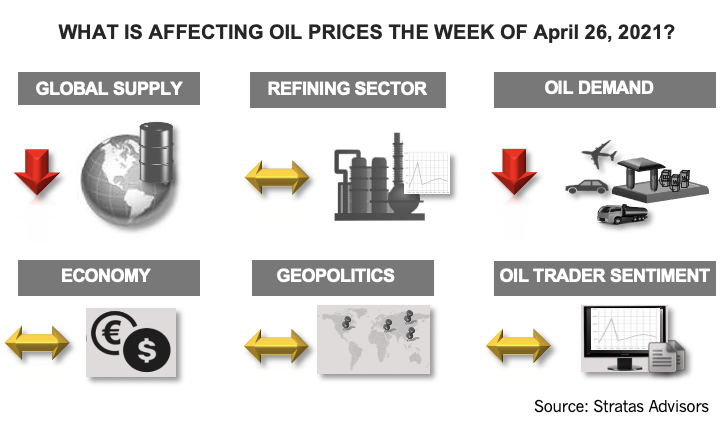

Last week, we pointed out that the fundamentals pertaining to the oil market are strengthening and looked supportive of oil prices during the second quarter. The demand outlook has continued to improve with the impact of COVID-19 being mitigated by behavior, vaccines and time. Furthermore, it appears that the recovery of the global economy is well on the way with the expectation that oil demand will outpace global supply during second-quarter 2021. We also discussed the range of geopolitical issues that could impact the oil markets (among others—Russia and the potential to disrupt the OPEC+ framework, China and its expanding linkages with Iran, and the increasing tensions between China and U.S. and the allies of the U.S. in Asia, as well as in Europe). However, while these geopolitical issues represent noteworthy risks, potential implications do not seem to be on the immediate horizon.

The one risk we highlighted that could have a more immediate impact—and the risk we have been highlighting since November—is the potential for another round of surges in COVID-19 cases that would have a global impact. This risk has been reinforced by the situation in India. Currently, in India the official number of COVID-19 cases per day is exceeding 300,000 and is expected to continue increasing up toward 500,000 cases per day. The situation is stunning because in early February, the cases were at record lows. With the surges in COVID-19 cases comes the potential impact on demand. While India only represents about 5% of total oil demand, during the previous peak of COVID-19 in 2Q20, India’s demand fell by 1.15 million bbl/d in comparison to the same period in 2019. As such, the demand decrease associated with India could have a significant impact on overall demand growth if India continues to struggle with COVID-19 and needs to implement severe lockdown measures. Furthermore, the risk of COVID-19 cases extends past India, since there are numerous countries in Asia and other regions that have been slow in ramping up their vaccination programs.

With additional crude supply coming to the market, the oil market will have heightened concerns about the robustness of demand and forecasted demand growth, and therefore, will react negatively to any signs that indicate weakening demand growth.

We will continue to monitor and assess the situation in India, as well as across the globe to determine if and when we might need to reduce our demand outlook for 2021, which entails a demand growth forecast of 6.34 million bbl/d in 2021 (in comparison with 2020).

About the Author:

John E. Paise, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

How Diversified Already Surpassed its 2030 Emissions Goals

2024-04-12 - Through Diversified Energy’s “aggressive” voluntary leak detection and repair program, the company has already hit its 2030 emission goal and is en route to 2040 targets, the company says.

BKV CEO Chris Kalnin says ‘Forgotten’ Barnett Ripe for Refracs

2024-04-02 - The Barnett Shale is “ripe for fracs” and offers opportunities to boost natural gas production to historic levels, BKV Corp. CEO and Founder Chris Kalnin said at the DUG GAS+ Conference and Expo.