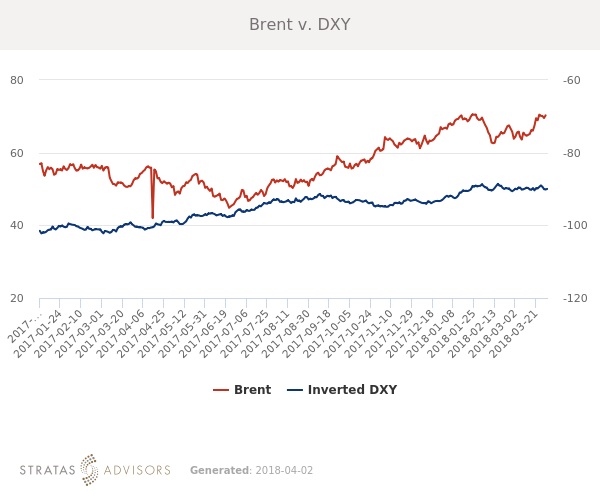

In the week since our last edition of What’s Affecting Oil Prices, Brent prices averaged $70.01/bbl last week, up $1.55/bbl from the week before.

Brent’s increase outstripped WTI, which averaged $65.03/bbl, up only $0.87/bbl after a lackluster report from the EIA on March 28. This week prices will likely lose some momentum, averaging $68.50/bbl.

Geopolitical: Neutral

There is minimal news on the geopolitical front that is likely to influence prices this week. While perennial issues such as the decline in Venezuela and unrest in Libya remain, we do not expect them to become more impactful in the short term.

Dollar: Neutral

Fundamental and sentiment-related drivers continue to have more impact on crude oil prices. The dollar and crude oil both rose last week. The dollar is seeing some fluctuation over concerns about recent tariffs enacted by the White House and retaliatory tariffs enacted by China.

Trader Sentiment: Positive

Nymex WTI and ICE Brent managed money net long positioning increased slightly last week. Overall market sentiment remains supportive but positioning has been moderating on a lack of new bullish indicators. Sentiment is seeing some support from statements by OPEC members that the production deal may be extended into 2019.

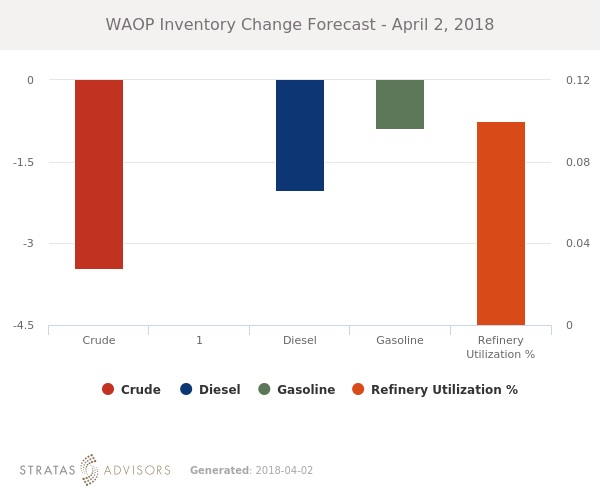

Supply: Negative

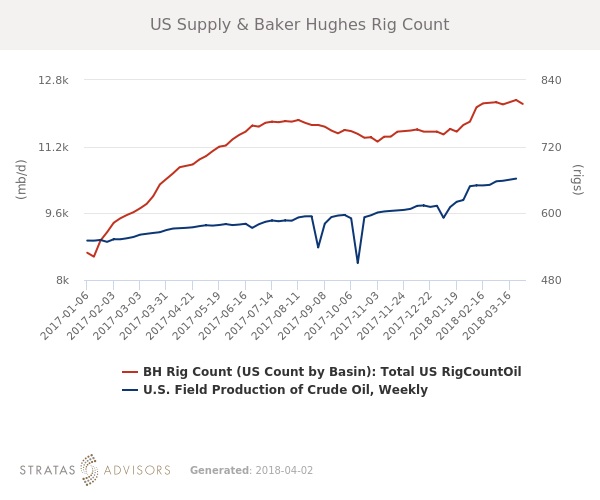

According to Baker Hughes, the number of U.S. oil rigs fell by seven last week. U.S. oil rigs now stand at 797, compared to 662 a year ago. Evidence of renewed global oversupply continues to pose the greatest threat to prices. On a somewhat supportive note, the Dallas Federal Reserve’s quarterly business survey provided more concrete evidence that service costs for U.S. drillers are rising, potentially slowing the rate of U.S. production growth.

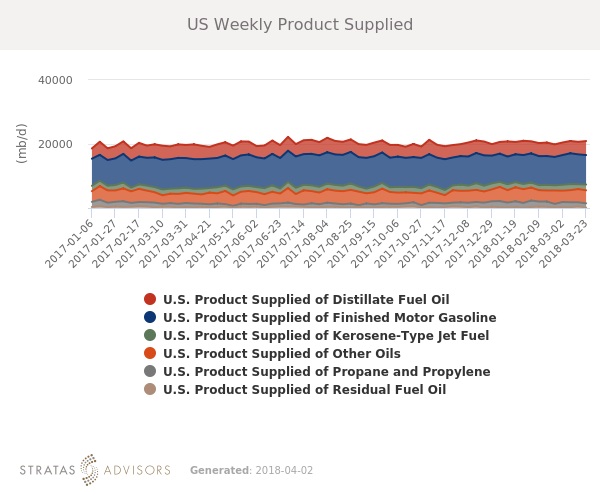

Demand: Positive

U.S. consumption of petroleum products remains generally at or above seasonal averages in all products, including fuel oil. Economic indicators so far presage strong consumer spending through the summer demand season and refined product demand is likely to remain a supportive factor in the short-term.

Refining: Neutral

Margins rose in almost every enclave last week, despite higher crude prices. Brent cracking in Rotterdam increased $2.32/bbl while Urals cracking in the Mediterranean increased $0.97/bbl. This comes despite Brent increasing $1.55/bbl last week.

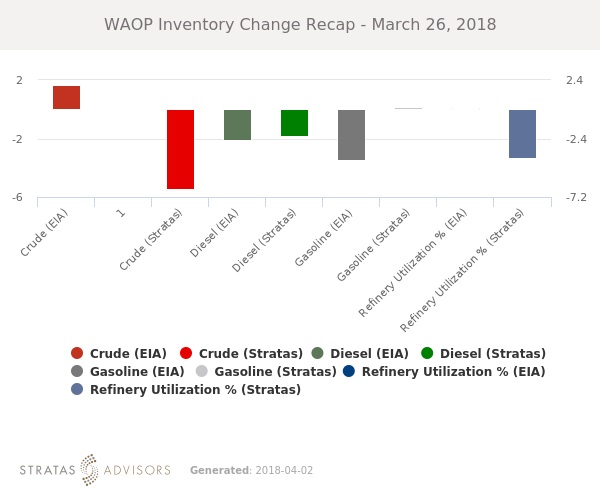

How We Did

Recommended Reading

US Refiners to Face Tighter Heavy Spreads this Summer TPH

2024-04-22 - Tudor, Pickering, Holt and Co. (TPH) expects fairly tight heavy crude discounts in the U.S. this summer and beyond owing to lower imports of Canadian, Mexican and Venezuelan crudes.

Imperial Expects TMX to Tighten Differentials, Raise Heavy Crude Prices

2024-02-06 - Imperial Oil expects the completion of the Trans Mountain Pipeline expansion to tighten WCS and WTI light and heavy oil differentials and boost its access to more lucrative markets in 2024.

US Gulf Coast Heavy Crude Oil Prices Firm as Supplies Tighten

2024-04-10 - Pushing up heavy crude prices are falling oil exports from Mexico, the potential for resumption of sanctions on Venezuelan crude, the imminent startup of a Canadian pipeline and continued output cuts by OPEC+.

Oil Broadly Steady After Surprise US Crude Stock Drop

2024-03-21 - Stockpiles unexpectedly declined by 2 MMbbl to 445 MMbbl in the week ended March 15, as exports rose and refiners continued to increase activity.

Exxon’s Payara Hits 220,000 bbl/d Ceiling in Just Three Months

2024-02-05 - ExxonMobil Corp.’s third development offshore Guyana in the Stabroek Block — the Payara project— reached its nameplate production capacity of 220,000 bbl/d in January 2024, less than three months after commencing production and ahead of schedule.