In the week since our last edition of What’s Affecting Oil Prices, Brent prices averaged $71.27/bbl last week, up $3.43/bbl from the week before.

WTI rose similarly, up $2.94/bbl to average $66.04/bbl. Prices were supported by fears around implications for a U.S. airstrike in Syria and by positive fundamental data from the recently released OPEC and IEA monthly oil market reports. This week prices will likely remain supported, with Brent averaging $70/bbl.

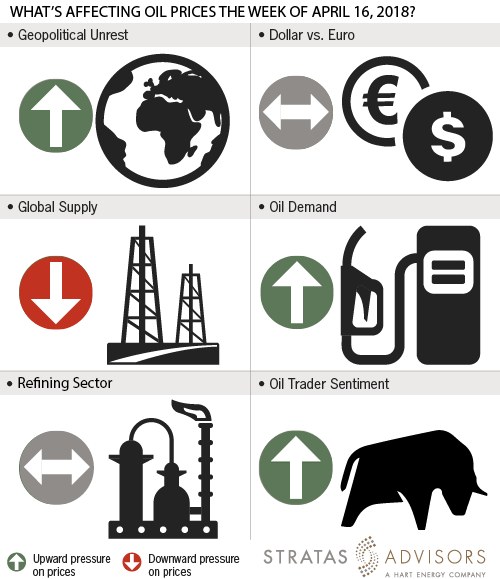

Geopolitical: Positive

Fears were that the joint U.S.-French-British airstrikes could lead to further escalation and retaliatory attacks within the region, leading to an increase in prices, but so far the international reaction to strikes has been muted. Analysts expect geopolitical risks to remain front-of-mind through the week. Regardless of the actual events that transpire, the fact that prices were so sharply impacted by a geopolitical event in which relatively little crude volumes were actually at risk is evidence that global balances are generally considered to be tighter by market participants.

Dollar: Neutral

Fundamental and sentiment-related drivers continue to have more impact on crude oil prices. The dollar fell slightly last week while Brent and WTI both increased.

Trader Sentiment: Positive

Nymex WTI managed money net long positioning fell back last week while ICE Brent managed money net long positioning increased. Overall positioning in both contracts remains supportive. Given the strong geopolitical drivers of the last week, ICE Brent is likely to see more support than Nymex WTI positioning in the week ahead.

Supply: Negative

According to Baker Hughes, the number of U.S. oil rigs rose by seven last week. U.S. oil rigs now stand at 815, compared to 683 a year ago. Evidence of renewed global oversupply continues to pose the greatest threat to prices.

Demand: Positive

U.S. consumption of petroleum products remains generally at or above seasonal averages in all products, including fuel oil. Economic indicators so far presage strong consumer spending through the summer demand season, and refined product demand is likely to remain a supportive factor in the short term.

Refining: Neutral

Margins fell across the board last week, with the largest declines seen in Brent-based values after Brent rose $3.43/bbl. Margins in Singapore generally saw the smallest decline with Dubai cracking falling $0.31/bbl and Dubai hydroskimming falling $0.60/bbl.

How We Did

Recommended Reading

NextEra Energy Dials Up Solar as Power Demand Grows

2024-04-23 - NextEra’s renewable energy arm added about 2,765 megawatts to its backlog in first-quarter 2024, marking its second-best quarter for renewables — and the best for solar and storage origination.

Halliburton’s Low-key M&A Strategy Remains Unchanged

2024-04-23 - Halliburton CEO Jeff Miller says expected organic growth generates more shareholder value than following consolidation trends, such as chief rival SLB’s plans to buy ChampionX.

Enverus: Q1 Upstream Deals Hit $51B, But Consolidation is Slowing

2024-04-23 - Oil and gas dealmaking continued at a high clip in the first quarter, especially in the Permian Basin. But a thinning list of potential takeout targets, and an invigorated Federal Trade Commission, are chilling the red-hot M&A market.

Baker Hughes Awarded Saudi Pipeline Technology Contract

2024-04-23 - Baker Hughes will supply centrifugal compressors for Saudi Arabia’s new pipeline system, which aims to increase gas distribution across the kingdom and reduce carbon emissions

Ithaca Energy to Buy Eni's UK Assets in $938MM North Sea Deal

2024-04-23 - Eni, one of Italy's biggest energy companies, will transfer its U.K. business in exchange for 38.5% of Ithaca's share capital, while the existing Ithaca Energy shareholders will own the remaining 61.5% of the combined group.