Key Points

Dry gas production increased by 0.63 billion cubic feet per day (Bcf/d) to average at 93.3 Bcf/d for the report week. This marks a consecutive week that production has shown gains. A mix of cold and above-average warm temperatures in different parts of the country saw demand from the power generation sector rise from 34.66 Bcf/d to 35.19 Bcf/d in the report week vs. the prior report week. Dry gas exports to Mexico increased by 0.15 Bcf/d to average 5.6 Bcf/d, while dry gas imports from Canada moved up by 0.22 Bcf/d to average 4.87 Bcf/d for the report week.

Our storage analysis leads us to expect a 97 billion cubic foot (Bcf) build for the report week of Oct. 4. If our forecast stands, our expectation will be above the current 93 Bcf consensus forecast and 8 Bcf higher than the five-year average of 89 Bcf.

Our overall view for the week is to see a negative movement in Henry Hub prices. We anticipate Henry Hub prices will likely trade this week within +/- 5 cents of the Oct. 7 $2.30 per million British thermal unit (MMBtu) closing price.

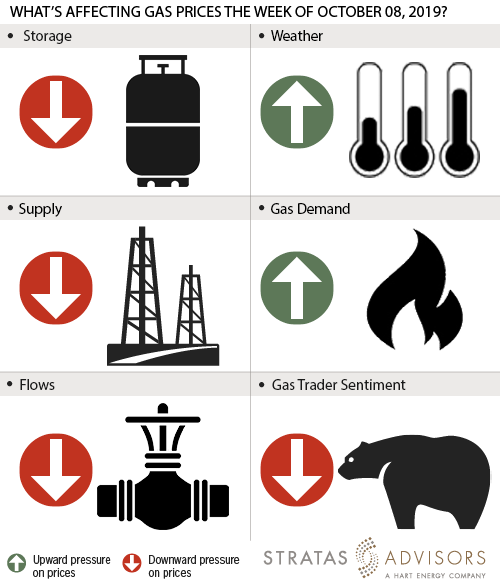

Storage – Negative

We estimate a storage build of 97 Bcf will be reported by the U.S. Energy Information Administration (EIA) for the week ended Oct. 4. Last week, EIA reported an above normal 112 Bcf injection for the prior week. The build increased inventory levels to 3,317 Bcf, 465 Bcf higher than the year-ago value but still 18 Bcf short of the five-year average. With the expectation of a 97 Bcf injection, we expect this week’s build to be higher than five-year average of 89 Bcf. With a higher injection expected this week compared to the five-year average, we see storage changes as a negative driver for gas prices this week.

Weather – Positive

The latest weekly temperature forecast from National Oceanic and Atmospheric Administration (NOAA) shows cold temperatures in early parts of the week in the Northeast and Midwest regions with highs in the 60s. Temperatures in those regions are projected to warm up mid-week then drop in the 30s to 40s range for the rest forecast. Temperatures in the Southeast and parts of the Southwest regions are expected to have high temperatures in the 70s and 80s for most of the forecast period. Despite the light demand, we expect power generation to be highest in the Southeast and Southwest regions of the country, and heating demand to be highest in the Northeast and Midwest regions. Overall, we expect the cold weather and the above-normal warm weather to have a positive effect on gas prices.

Supply – Negative

Supply levels increased for a consecutive week to post an average of 93.3 Bcf/d, compared to 92.67 Bcf/d from the previous report week. Accordingly, supply will likely apply negative pressure to this week’s price activity.

Demand – Positive

Residential and commercial sector demand moved up by 1.97 Bcf/d or 13.8 Bcf to average at 10.47 Bcf/d for the report week. Industrial demand showed week-on-week gains of 0.19 Bcf/d and a weekly average value of 21.27 Bcf/d. We expect structural demand-side drivers for the report week to have a positive effect on prices.

Flows – Negative

For a second week in a row, flows to LNG terminals show a week-on-week loss. We expect flows to LNG terminals this week to average at 6.15 Bcf/d, a 0.03 Bcf/d loss from the previous week. The slight decline in flows can be considered a negative this week.

Trader Sentiment – Negative

The U.S. Commodity Futures Trading Commission's (CFTC) Oct. 4 commitment of traders report for Nymex natural gas futures and options showed that reportable financial positions (managed money and other) on Oct. 1 were 121,303 net short while reportable commercial operator positions came in with an 88,193 net long position. Total open interest was reported for this week at 1,198,913 and was up 23,055 lots from last week's reported 1,175,858 level. Sequentially, commercial operators this reporting week were adding to longs by 5,800 while adding to shorts by 32. Financial speculators cut shorts and cut longs for the week (-8,665 vs. -8,499, respectively). Overall, we see trader sentiment will likely be negative this week.

Recommended Reading

Defeating the ‘Four Horsemen’ of Flow Assurance

2024-04-18 - Service companies combine processes and techniques to mitigate the impact of paraffin, asphaltenes, hydrates and scale on production—and keep the cash flowing.

Tech Trends: AI Increasing Data Center Demand for Energy

2024-04-16 - In this month’s Tech Trends, new technologies equipped with artificial intelligence take the forefront, as they assist with safety and seismic fault detection. Also, independent contractor Stena Drilling begins upgrades for their Evolution drillship.

AVEVA: Immersive Tech, Augmented Reality and What’s New in the Cloud

2024-04-15 - Rob McGreevy, AVEVA’s chief product officer, talks about technology advancements that give employees on the job training without any of the risks.

Lift-off: How AI is Boosting Field and Employee Productivity

2024-04-12 - From data extraction to well optimization, the oil and gas industry embraces AI.

AI Poised to Break Out of its Oilfield Niche

2024-04-11 - At the AI in Oil & Gas Conference in Houston, experts talked up the benefits artificial intelligence can provide to the downstream, midstream and upstream sectors, while assuring the audience humans will still run the show.