Key Points

Dry gas production rose by 0.74 Bcf/d to average at 92.95 for the report week. The rise in production comes after two consecutive weeks of declines.

Cooler temperatures across the country saw demand from the power generation sector fall from 35.12 Bcf/d to 34.52 Bcf/d in the report week vs. the prior report week. This marks the second week that power generation has fallen. Dry gas exports to Mexico increased by 0.21 Bcf/d to average 5.49 Bcf/d, while dry gas imports from Canada showed no change and remained at 4.65 Bcf/d for the report week.

Our storage analysis leads us to expect a 109 Bcf build for the report week of Sept. 27. Our expectation is above the current 106 Bcf consensus forecast and 26 Bcf higher than the five-year average of 83 Bcf.

Our overall view for the week is to see a negative movement in Henry Hub prices. We anticipate Henry Hub prices will likely trade this week within +/- 5 cents of the Monday $2.35/MMBtu closing price.

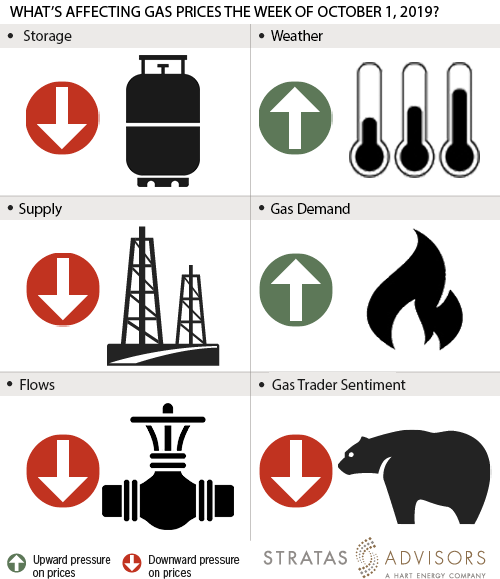

Storage – Negative

We estimate an above-normal and above-consensus storage build of 109 Bcf will be reported by the EIA for the week ended Sep 27. Last week, EIA reported a 102 Bcf injection for the prior week, slightly beyond our ahead-of-consensus 99 Bcf. The build increased inventory levels to 3,205 Bcf, 444 Bcf higher than the year-ago value, yet levels are still 47 Bcf lower than normal. Overall, our higher expectations for storage to be reported later this week will likely drive a negative market reaction for gas prices this week.

Weather – Positive

The latest weekly temperature forecast from NOAA shows fall temperatures beginning to enter the north and northwestern portions of the country with low temperatures in the 20s to 40s. This should prompt early heating demand in these markets. We expect power generation demand to be highest in the south and east regions of the country, where above-normal high temperatures are projected to be in the upper 80s to lower 90s. Overall, we expect the warmer weather in more populated regions to be amplified by the colder weather elsewhere, summing up to an overall positive weather effect in gas prices.

Supply – Negative

Supply levels rose for the first time in three weeks to post an average of 92.95 Bcf/d, compared to 92.21 Bcf/d from the previous report week. Accordingly, supply will likely apply negative pressure to this week’s price activity.

Demand – Positive

Industrial demand slightly moved up by 0.03 Bcf/d to average at 21.05 Bcf/d for the report week. Residential and commercial sector demand followed the same trend with a more noticeable w-o-w increase of 0.24 Bcf/d or 1.68 Bcf change adding up to a weekly average value of 8.58 Bcf/d. We expect structural demand side drivers for the report week to have a positive effect on prices.

Flows – Negative

Flows to LNG terminals show a week-on-week loss of 0.21 Bcf/d to average 6.18 Bcf/d for the report week. The slight decline in flows can be considered as a negative this week.

Trader Sentiment – Negative

The CFTC's 9/27/2019 commitment of traders report for NYMEX natural gas futures and options showed that reportable financial positions (managed money and other) on 9/24/2019 were 121,469 net short while reportable commercial operator positions came in with an 82,425 net long position. Total open interest was reported for this week at 1,175,858 and was down 78,267 lots from last week's reported 1,254,125 level. Sequentially, commercial operators this reporting week were cutting longs by 22,487 while cutting shorts by 20,477. Financial speculators cut shorts and longs for the week (-4,734 vs -7,630, respectively). Overall, we see trader sentiment will likely be negative this week.

Recommended Reading

Marathon Petroleum Sets 2024 Capex at $1.25 Billion

2024-01-30 - Marathon Petroleum Corp. eyes standalone capex at $1.25 billion in 2024, down 10% compared to $1.4 billion in 2023 as it focuses on cost reduction and margin enhancement projects.

Humble Midstream II, Quantum Capital Form Partnership for Infrastructure Projects

2024-01-30 - Humble Midstream II Partners and Quantum Capital Group’s partnership will promote a focus on energy transition infrastructure.

Hess Corp. Boosts Bakken Output, Drilling Ahead of Chevron Merger

2024-01-31 - Hess Corp. increased its drilling activity and output from the Bakken play of North Dakota during the fourth quarter, the E&P reported in its latest earnings.

The OGInterview: Petrie Partners a Big Deal Among Investment Banks

2024-02-01 - In this OGInterview, Hart Energy's Chris Mathews sat down with Petrie Partners—perhaps not the biggest or flashiest investment bank around, but after over two decades, the firm has been around the block more than most.

Some Payne, But Mostly Gain for H&P in Q4 2023

2024-01-31 - Helmerich & Payne’s revenue grew internationally and in North America but declined in the Gulf of Mexico compared to the previous quarter.