Key Points: The daily average production rate remained around the 85 billion cubic feet per day (Bcf/d) with very little variation week-on-week. Demand from power generation rose by 2.65 Bcf/d or 18.5 Bcf over the week and electric industry demand should increase further through in June. Dry gas exports to Canada rose by 0.18 Bcf/d or 1.29 Bcf while exports to Mexico also rose by 0.04 Bcf/d or 0.28 Bcf week-on-week.

Overall, the supply-demand balance remained relatively unchanged. Our analysis leads us to expect 97 Bcf storage build will be reported by EIA for the report week. Our expectation compares to the 100 Bcf consensus whisper expectation and the five-year average, which is nearly 2 Bcf lower at 95 Bcf.

Waha prices, which temporarily recovered above zero in mid-May, crashed below zero for the entire report week. Insufficient takeaway capacity combined with pipeline maintenance are the main causes for the plunge. Henry Hub prices also took a hit on May 27 despite being a federal holiday. Sempra Energy announced the start of Train 1 at their Cameron LNG facility and we anticipate that that would contribute to net flows in the coming weeks.

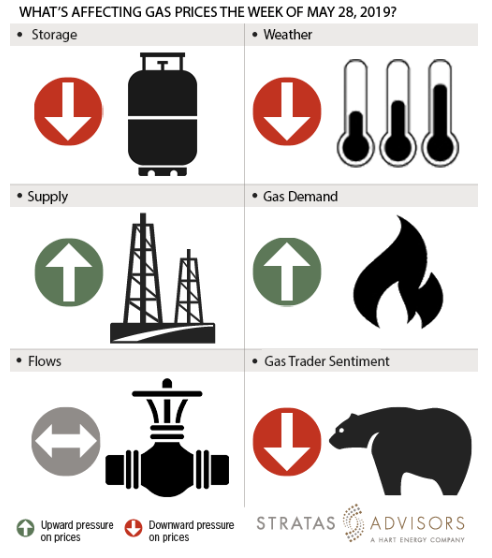

Storage: Negative

We estimate a storage withdrawal of 97 Bcf will be reported this week for the week ended May 24. Our 97 Bcf expectation is on par with the five-year average value of 95 Bcf. Last week we had predicted a storage build of 106 Bcf. This was 6 Bcf higher than the actual reported value of 100 Bcf. The inventory levels are at 1,753 Bcf, 137 Bcf higher than year ago levels and 274 Bcf lower than five-year average values. All in, we see storage changes as a negative driver for this week’s natural gas market.

Weather: Negative

The weather is expected to become more mild in the eight- to 14-day forecast. We expect this to impact the demand. Accordingly, natural gas prices have been dropping from last week’s highs. Spot intraday natural gas prices as of May 28 are at $2.57/MMBtu. The natural gas price at the time of our report last week was at $2.73/MMBtu. We see weather as a negative driver for the gas prices this week.

Supply: Positive

Average field supply decreased marginally by 0.3 Bcf/d or 2.3 Bcf for the report week. The temporary drop is due to scheduled maintenance events on natural gas pipelines and should not linger well beyond the current week. Accordingly, supply should likely exert a mild positive pressure to this week’s price activity.

Demand: Positive

We see a positive effect from structural demand side drivers this week, especially from power generation. From next week onward, demand surges from power generation combined with the start of the Cameron Train 1 LNG can be expected to absorb a lot of production and a smaller supply might be available for storage.

Flows: Neutral

NGPL maintenance is limiting northbound flows subsequently resulting in a crash of Waha Hub prices. However, flows can be considered as neutral for Henry Hub price activity.

Trader Sentiment: Negative

With weather models reporting moderate conditions through the first few weeks of June and high supply resulting in strong storage builds, natural gas futures are trading several cents lower on May 28. The CFTC’s May 24 commitment of traders report for NYMEX natural gas futures and options showed that reportable financial positions (Managed Money and Other) on May 21 were 61,841 net short while reportable commercial operator positions came in with a 32,660 net long position. Total open interest was reported for this week at 1,323,538 and was down 9,301 lots from last week’s reported 1,332,839 level.

Recommended Reading

Range Resources Plans Flat Production Target in 2024

2024-02-23 - Gas producer Range Resources is focusing on system flexibility to respond to market trends.

Permian NatGas Hits 15-month Low as Negative Prices Linger

2024-04-16 - Prices at the Waha Hub in West Texas closed at negative $2.99/MMBtu on April 15, its lowest since December 2022.

Antero Poised to Benefit from Second Wave of LNG

2024-02-20 - Despite the U.S. Department of Energy’s recent pause on LNG export permits, Antero foresees LNG market growth for the rest of the decade—and plans to deliver.

Turning Down the Volumes: EQT Latest E&P to Retreat from Painful NatGas Prices

2024-03-05 - Despite moves by EQT, Chesapeake and other gassy E&Ps, natural gas prices will likely remain in a funk for at least the next quarter, analysts said.

Exclusive: Chevron Balancing Low Carbon Intensity, Global Oil, Gas Needs

2024-03-28 - Colin Parfitt, president of midstream at Chevron, discusses how the company continues to grow its traditional oil and gas business while focusing on growing its new energies production, in this Hart Energy Exclusive interview.