Key Points: With warm weather sweeping across the United States, field production increased marginally due to the absence of freeze-offs. Average field production increased by 4 billion cubic feet (Bcf) week-on-week and ended in an average of 84.4 Bcf/d for the report week ended March 15. Warm weather resulted in a sharp decline in demand by almost 28 Bcf/d week on week. Prompted by high production and low demand, Canadian imports dropped by 5 Bcf and Mexico exports increased by 0.07 Bcf.

Our analysis leads us to expect a 48 Bcf withdrawal will be reported by the U.S. Energy Information Administration (EIA) on March 21, a good bit below the 57 Bcf five-year average withdrawal and in comparison with the current 51 Bcf consensus whisper expectation.

Last week’s withdrawal of 204 Bcf was a surprise high withdrawal for the second week in a row, and was almost double the five-year average withdrawal. Our March winter exit rate is forecasted at 1.0 Tcf, still within five-year values. We do not expect any price movements at Henry Hub given that natural gas fundamentals are likely to remain stable for the remainder of the winter.

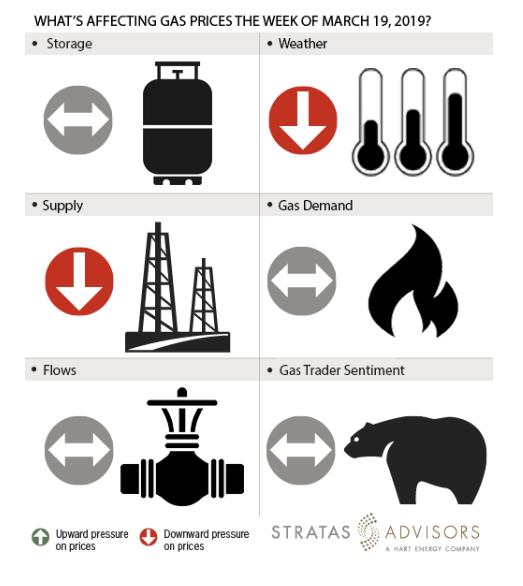

Storage: Neutral

We estimate a storage withdrawal of 48 Bcf will be reported by EIA this week for the week ended March 15. This level is almost one-fourth of the value forecasted for last week. We had predicted a 215 Bcf withdrawal for prior week and overshot the EIA report value by 11 Bcf. The EIA draw will be closer to the five-year average value because of a mix of warm and cool weather. Accordingly, we expect storage to be a neutral driver this week.

Weather: Negative

NOAA weather forecasts for the six-to-10 day period through March 24 shows a warming trend for major parts of the Lower 48. Only portions of South are witnessing lower than normal temperatures for late March. This is seen in the marked drop in the heating demand in Midwest and Northeast portions of the United States. Weather conditions are slightly cooler for this week compared to the prior week, albeit only slightly.

Supply: Negative

In the absence of freeze-offs and any conditions upsetting wellhead production, the average field supply increased marginally to 84.4 Bcf/d for the report week. We believe this supply is only going to increase as we move into spring and summer. Not all of this supply might be going to satisfy domestic demand. Industrial units and power plants will take up a portion of supply, so will LNG exports. All in, we see supply as exerting negative pressure to prices this week.

Demand: Neutral

As the weather warms throughout Lower 48, winter heating demand is expected to fall. Demand from other structural demand-side drivers fell significantly by 6 Bcf/d or 42 Bcf for the report week. We see that the demand from major categories has remained close to the averages for the first three days of the current week compared to the same period as report week. This week we see demand as neutral.

Flows: Neutral

We note that there is lots of stranded gas in the Permian Basin because of an equipment failure on the El Paso natural gas pipeline. El Paso local prices have gone down because of the disturbance, however, the effect of national benchmark of Henry Hub is neutral.

Trader Sentiment: Neutral

We expect the market to hold on the prices around $2.80 range. The CFTC’s March 15 commitment of traders report for NYMEX natural gas futures and options showed that reportable financial positions (Managed Money and Other) on March 12 were 24,229 net short while reportable commercial operator positions came in with a 10,843 net short position as well. We see trader sentiment as neutral.

Recommended Reading

Wayangankar: Golden Era for US Natural Gas Storage – Version 2.0

2024-04-19 - While the current resurgence in gas storage is reminiscent of the 2000s —an era that saw ~400 Bcf of storage capacity additions — the market drivers providing the tailwinds today are drastically different from that cycle.

Biden Administration Criticized for Limits to Arctic Oil, Gas Drilling

2024-04-19 - The Bureau of Land Management is limiting new oil and gas leasing in the Arctic and also shut down a road proposal for industrial mining purposes.

SLB’s ChampionX Acquisition Key to Production Recovery Market

2024-04-19 - During a quarterly earnings call, SLB CEO Olivier Le Peuch highlighted the production recovery market as a key part of the company’s growth strategy.

PHX Minerals’ Borrowing Base Reaffirmed

2024-04-19 - PHX Minerals said the company’s credit facility was extended through Sept. 1, 2028.

Exclusive: The Politics, Realities and Benefits of Natural Gas

2024-04-19 - Replacing just 5% of coal-fired power plants with U.S. LNG — even at average methane and greenhouse-gas emissions intensity — could reduce energy sector emissions by 30% globally, says Chris Treanor, PAGE Coalition executive director.