Key Points:

Field production remained flat at 93 billion cubic feet per day (Bcf/d) for the report week ended Jan 10. Average demand in the residential and commercial sectors climbed by 3.63 Bcf/d or 25 Bcf due to colder weather in consuming regions of the United States. Last week, the U.S Energy Information Administration (EIA) reported a weak draw of 44 Bcf compared to Stratas Advisors expectations of 52 Bcf and the then-consensus of 55 Bcf. As a result, we show 3,148 Bcf in working natural gas inventories, which is 74 Bcf higher than five-year average. Dry gas imports from Canada increased by 0.53 Bcf/d or 3.7 Bcf while exports to Mexico also increased by 0.78 Bcf/d or 5.4 Bcf.

For this week, our analysis leads us to expect a 87 Bcf withdrawal. Again our expectation is lower (5 Bcf this week) than the current consensus of 92 Bcf. Both are less than half of the 223 Bcf five-year average storage withdrawal, which shows the combined effect of high production and low winter demand overall this year.

Key Hub Price Call:

Henry Hub prices have maintained in the $2.00-$2.10 range during the report week. Prices rose by 3.3% on Jan. 13 compared to the Jan. 10 close of $2.08. Any cold weather could help Henry Hub to rise above the current levels at this point.

Gas Price Differentials:

Cold air continues in the West and Northern Plains where we see strong local demand. We see gas differentials in Opal Hub and Wyoming increasing with respect to Henry Hub.

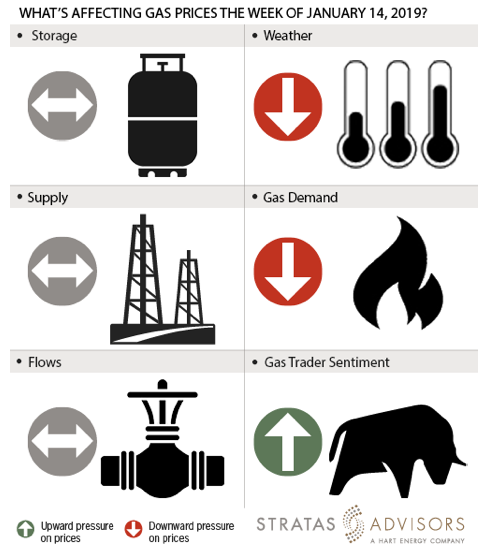

Storage: Neutral

We estimate a storage withdrawal of 87 Bcf will be reported by EIA for the week ended Jan. 10. This withdrawal is higher than the last week’s reported draw of 44 Bcf, yet is much lower than the five year average of 223 Bcf. Because of the weak draw last week, inventory stockpiles went from a -38 deficit to a +74 surplus compared to five-year averages. We had predicted a 52 Bcf withdrawal for prior week and overshot the EIA report value by 8 Bcf. Accordingly, we expect storage to be a neutral driver this week.

Weather: Negative

Temperatures are comfortably warm throughout United States and is expected to remain the same through the next six to 10 days. There may be strong demand locally in Rockies during early this week but that is not bound to swing the national demand by much. Temperatures are forecasted to revert to upper 60s during the latter part of the week for populous regions in Northeast, Texas and Southeast. Weather is a negative factor for gas price activity.

Supply: Neutral

In the absence of freeze-offs and any conditions upsetting wellhead production, the average field supply remained flat for the report week. Natural gas producers aren’t seeing much incentive to increase production apart from LNG exports which are flagging with low global demand growth. Drilling activities have decreased in most U.S. shale plays with a drop in the number of oil and gas rigs. The total number of rigs have dropped by over 294 compared to last year’s 1,075 level. Even accounting for production efficiencies, this drop is bound is help production to decrease or remain flat. We see supply offering a neutral pressure on gas prices.

Demand: Negative

Demand from other structural demand side drivers increased by 5.51 Bcf/d or 37 Bcf for the report week, thereby increasing the storage pull expectations by almost 35 Bcf compared to prior week. Initial expectations for next week show a lighter demand for next week. We see that the demand from major categories is almost 3 Bcf less for the averages for the first three days of the current week compared to the same period as report week. This week we see demand as negative.

Flows: Neutral

Average LNG flows for report week remained stable from prior week’s levels. Flows are a neutral factor for gas prices.

Trader Sentiment: Positive

We see trader sentiment as positive factor for gas price activity. The CFTC’s Jan. 10 commitment of traders report for NYMEX natural gas futures and options showed that reportable financial positions (Managed Money and Other) on Jan. 7 were 207,252 net short while reportable commercial operator positions came in with a 161,883 net long position. Total open interest was reported for this week at 1,370,227 and was up 53,974 lots from last week’s reported 1,316,253 level. Sequentially, commercial operators this reporting week were adding to longs by 10,398 while adding to shorts by 7,109. Financial speculators added shorts and added longs for the week (25,722 vs 21,682, respectively).

Recommended Reading

Santos’ Pikka Phase 1 in Alaska to Deliver First Oil by 2026

2024-04-18 - Australia's Santos expects first oil to flow from the 80,000 bbl/d Pikka Phase 1 project in Alaska by 2026, diversifying Santos' portfolio and reducing geographic concentration risk.

Iraq to Seek Bids for Oil, Gas Contracts April 27

2024-04-18 - Iraq will auction 30 new oil and gas projects in two licensing rounds distributed across the country.

Vår Energi Hits Oil with Ringhorne North

2024-04-17 - Vår Energi’s North Sea discovery de-risks drilling prospects in the area and could be tied back to Balder area infrastructure.

Tethys Oil Releases March Production Results

2024-04-17 - Tethys Oil said the official selling price of its Oman Export Blend oil was $78.75/bbl.

Exxon Mobil Guyana Awards Two Contracts for its Whiptail Project

2024-04-16 - Exxon Mobil Guyana awarded Strohm and TechnipFMC with contracts for its Whiptail Project located offshore in Guyana’s Stabroek Block.