(Source: Shutterstock, HartEnergy.com)

Learn more about Hart Energy Conferences

Get our latest conference schedules, updates and insights straight to your inbox.

Key Points: Average dry gas production increased week-over-week and reached about 91 billion cubic feet per day (Bcf/d) for the report week ending Aug. 2. Demand from power generation rose 2.2 Bcf/d from the previous week. The average demand for power generation for the report week was 41.10 Bcf/d. LNG net exports from U.S. were at 5.93 Bcf/d during the report week. Imports from Canada increased by 0.13 Bcf/d while exports to Mexico declined 0.04 Bcf/d to average 5.31 Bcf/d.

Our analysis leads us to expect a 60 Bcf injection level for the report week. Our expectation is closely aligned to the current consensus of 59 Bcf and 5 Bcf more than the 55 Bcf five-year average storage build.

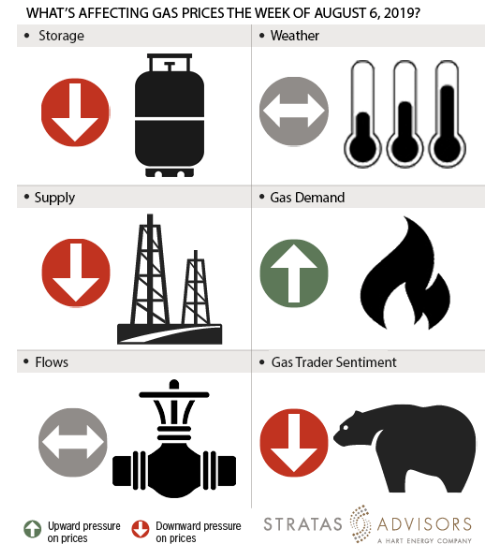

Storage: Negative

We estimate a storage build of 60 Bcf will be reported by EIA for the week ended Aug. 2. Last week, EIA reported a 65 Bcf injection for the prior week. The build increased inventory levels to 2,364 Bcf and increased deficits to 123 Bcf compared to the five-year average. This week we expect the build to be higher than the five-year average. We see storage changes as a negative driver for gas prices this week.

Weather: Neutral

According to forecasts by the National Oceanic and Atmospheric Administration (NOAA), we expect demand to be moderate for the next eight to 10 days. We are expecting cooler temperatures in the Midwest and East portions of the U.S. with temperatures staying in the mid-70s to low-80s. The hottest regions will be the Southwest and Texas with temperatures expected to stay above 90. The peak of the summer is almost over but temperatures are not falling yet. This might have an effect on demand, but since the supply levels are so strong this year we think the effect of weather will be a neutral driver for gas prices this week.

Supply: Negative

Field supply increased to more than 91 Bcf/d during the report week. Average total dry gas production increased by approximately 1% compared to the prior week. Compared to prior week, dry gas production increased 1.50 Bcf/d or 10 Bcf for the report week. All together, we see supply as exerting negative pressure to prices this week.

Demand: Positive

Gas demand for power, which averaged above 41 Bcf/d, accounts for more than half of the total natural gas demand in the United States. Power generation demand has increased by 2.22 Bcf/d or 15.6 Bcf week-on-week. Demand from industrial plants stayed relatively flat at about 20.8 Bcf/d. We think demand will be a positive driving factor for gas prices.

Flows: Neutral

Flows can be considered neutral this week as there are no new upset conditions.

Trader Sentiment: Negative

With cooler temperatures expected for the Midwest and Northeast regions, we project Henry Hub prices to average lower than $2.20 for the current week. Natural gas futures for August dropped during trading on the morning of Aug. 5. It appears as though the markets are not finding any incentive to raise prices. We see trader sentiment as being negative for the gas price activity. The CFTC’s Aug. 2 commitment of traders’ report for NYMEX natural gas futures and options showed that reportable financial positions (managed money and other) on Aug. 30 were 203,650 net short while reportable commercial operator positions came in with a 169,377 net long position. Total open interest was reported at 1,362,478 this week and was up 31,659 lots from last week's reported 1,330,819 level.

Recommended Reading

Moda Midstream II Receives Financial Commitment for Next Round of Development

2024-03-20 - Kingwood, Texas-based Moda Midstream II announced on March 20 that it received an equity commitment from EnCap Flatrock Midstream.

Tellurian Executive Chairman ‘Encouraged’ by Progress

2024-03-18 - Tellurian announced new personnel assignments as the company continues to recover from a turbulent 2023.

Enbridge Advances Expansion of Permian’s Gray Oak Pipeline

2024-02-13 - In its fourth-quarter earnings call, Enbridge also said the Mainline pipeline system tolling agreement is awaiting regulatory approval from a Canadian regulatory agency.

Bobby Tudor on Capital Access and Oil, Gas Participation in the Energy Transition

2024-04-05 - Bobby Tudor, the founder and CEO of Artemis Energy Partners, says while public companies are generating cash, private equity firms in the upstream business are facing more difficulties raising new funds, in this Hart Energy Exclusive interview.

TC Energy Appoints Sean O’Donnell as Executive VP, CFO

2024-04-03 - Prior to joining TC Energy, O’Donnell worked with Quantum Capital Group for 13 years as an operating partner and served on the firm’s investment committee.