Gas prices have rallied, but what will be the implications for the North American shale market this winter? (Source: Leonid Ikan/Shutterstock.com)

Learn more about Hart Energy Conferences

Get our latest conference schedules, updates and insights straight to your inbox.

We are heading into winter months with record high natural gas prices as strong demand recovery and unplanned supply outages have led to tighter markets. According to the International Energy Agency’s (IEA) latest gas market report, such tensions are a reminder that security of supply remains a major concern only a year after a record drop in demand left markets oversupplied.

But what does this mean for the U.S. natural gas market?

Last week, Natural Gas Supply Association (NGSA) Chairman David Attwood said he expects U.S. shale producers to be actively involved in the response to the highest natural gas prices in nearly a decade.

“I firmly believe the market works,” Attwood told media following the release of NGSA’s Annual Winter Outlook. “There is no doubt the market is giving strong signals for production to increase. That supply is there and will come and meet the demand.”

In its winter outlook, NGSA said it expects a “gradual production recovery” and increase in rig counts during the winter months to offset rising demand.

On the supply side, the outlook expects an increase in production this winter, with the daily average up 4% or 3.7 billion cubic feet per day (Bcf/d) above last year winter, putting downward pressure on prices.

RELATED: Analysis: Global Natgas Price Surge Looms for US This Winter

“These are very interesting times in the gas market,” said Amber McCullagh, director of intelligence at Enverus, adding that September was the most volatile month in terms of gas prices in the post-shale era with the exception of cold winters

“Right now, gas storage inventories are more than 200 Bcf below the 5-year average…Certainly the U.S. is in a better situation than Europe, but we don’t have a buffer in terms of average storage inventories like we did over the last 5 years,” McCullagh said, speaking at Enevrus’s natural gas outlook webinar last week.

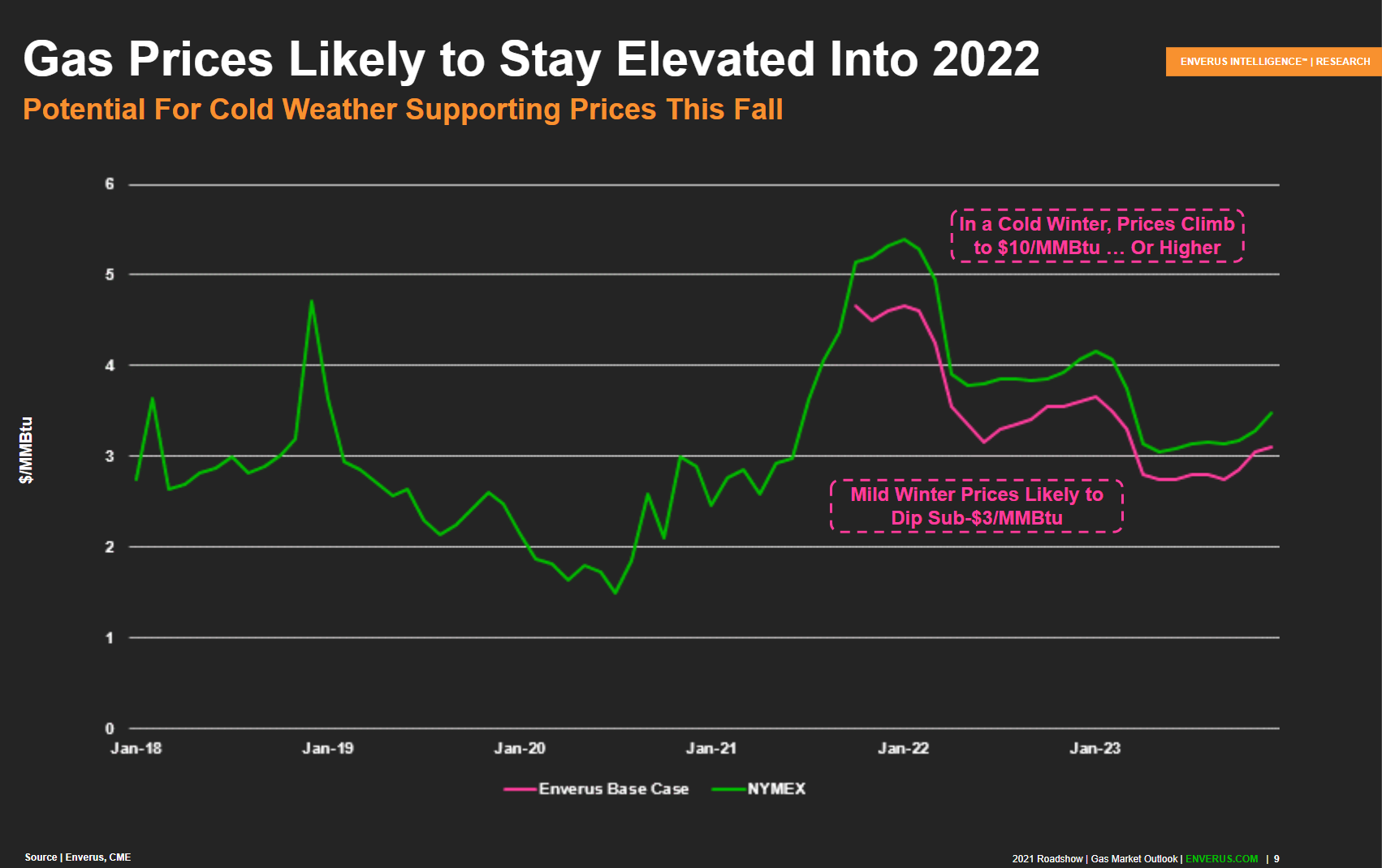

McCullagh also noted that gas prices are likely to stay elevated into 2022. If the winter is mild—which is unlikely—gas prices could dip into the mid $4/MMBtu range. However, in a cold winter scenario, prices could soar up to $10/MMBtu or higher. (Figure 1)

Unlike the past decade, Enverus expects seasonal supply growth from the Northeast in the coming months.

“This winter, we will see relatively seasonal gas production out of the Northeast. Marcellus southwest is where you will see most of the seasonality consistent with the region’s takeaway capacity,” McCullagh noted.

In contrast, she said season-to-season production growth is expected in the Haynesville, where production will continue to grow at a rate of 1.5 to 2 Bcf/d annual pace until gas prices come down.

However, gas activity in the Permian Basin will continue ramping up, in both the Midland and Delaware basins, as public operators and private companies continue drilling.

Another factor affecting gas supply is the continued growth of LNG capacity, McCullagh noted. North America continues to add LNG capacity with two major projects ramping up over the next two years. Venture Global’s Calcasieu Pass in Louisiana is expected to be fully operational by 2023. The 10 million mt/year capacity facility will use modular trains that are smaller than the traditional liquefaction units used at U.S. facilities.

Speaking at the Gastech conference last month, Venture Global CEO Michael Sabel said the export terminal is nearing completion and will begin production within months.

Additionally, Cheniere Energy’s Sabine Pass facility is running ahead of schedule and is set to begin liquefying gas in first-quarter 2022, which will add another 750 Mcf/d of feed gas demand.

McCullagh also noted that the coming winter will not impact LNG exports. That is a dramatic reversal for the LNG export industry, which was idling last year in a pandemic oversupply amid discussion of the role of gas in a low-carbon world.

“This year, even if gas prices spike, it is unlikely to threaten the economics of LNG exports because global gas prices are high and supply is limited,” she said.

Will coal offer relief?

Despite significant additions in wind and solar capacity, McCullagh noted non-fossil power generation is down year on year.

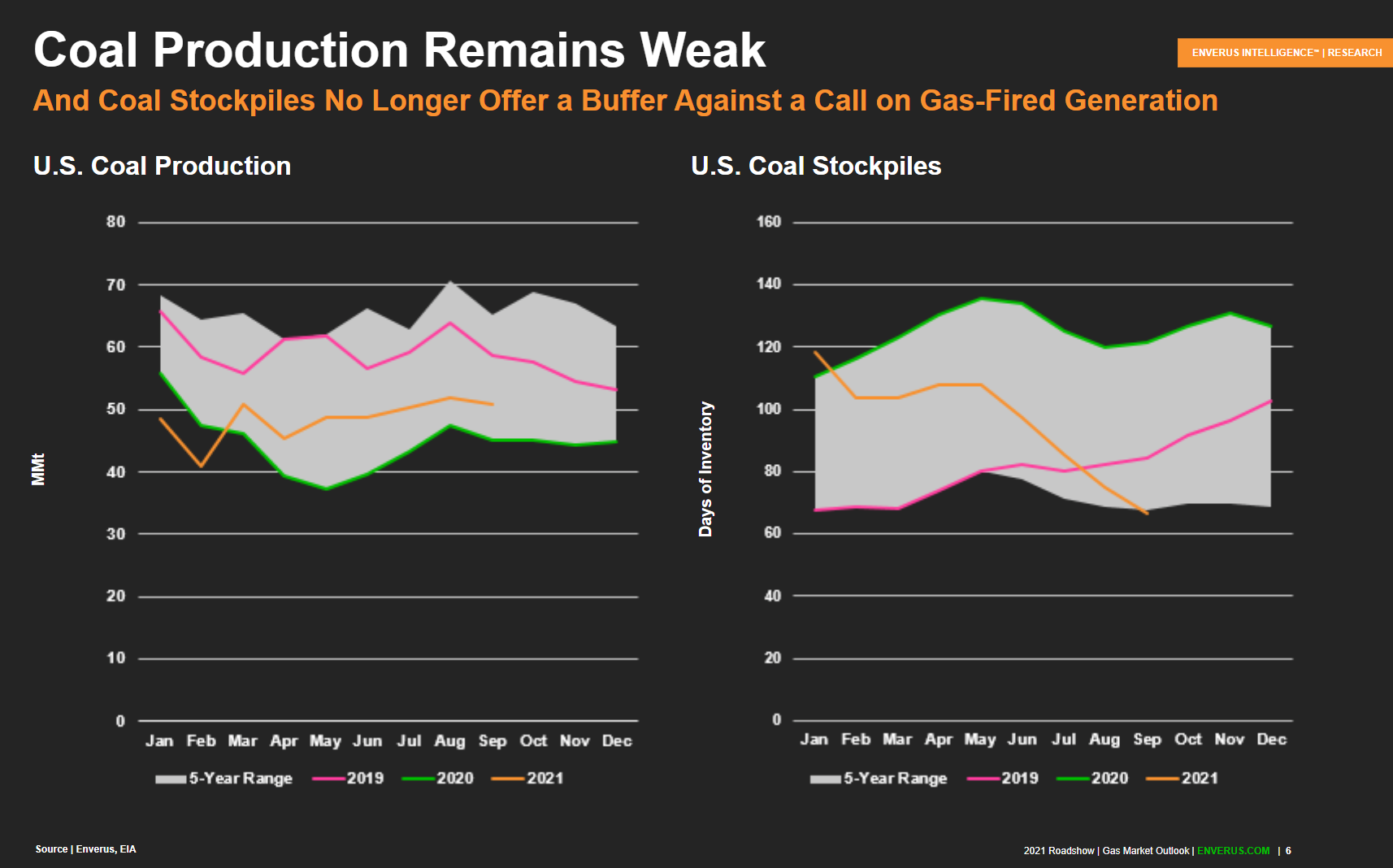

In addition, she said coal generation is limited in how it can ramp up in response to higher gas prices since coal production has been relatively flat year to date, despite the tremendous rally in Henry Hub prices (Figure 2).

“With that higher call on fossil generation this summer and higher gas prices, we have already drawn down coal stockpiles significantly…so inventories are already at the very low end, which means coal will no longer offer a buffer against a call on gas-fired power generation this winter,” she said.

Additionally, coal production recovery has been limited because the plants that would have burned the incremental coal have largely retired or are set to retire soon.

About 9.2 GW of coal-fired generation retired in 2020 and another 3.2 GW is expected to retire in 2021, followed by 4.9 GW in 2022, S&P Global Market Intelligence data shows.

Demand continues to outrun supply because that there is not a lot of elasticity on either the demand or supply side.

“Storage inventories will remain low through the winter,” McCullagh noted. “Any demand upside due to extreme weather will likely imbalance the market because we have exhausted coal generation, there will be no immediate response in LNG exports and no elasticity in demand until gas prices are competitive with oil products.”

Recommended Reading

TC Energy’s Keystone Back Online After Temporary Service Halt

2024-03-10 - As Canada’s pipeline network runs full, producers are anxious for the Trans Mountain Expansion to come online.

Early Startup of Trans Mountain Pipeline Expansion Surprises Analysts

2024-04-04 - Analysts had expected the Trans Mountain Pipeline expansion to commence operations in June but the company said the system will begin shipping crude on May 1.

Pembina Pipeline Enters Ethane-Supply Agreement, Slow Walks LNG Project

2024-02-26 - Canadian midstream company Pembina Pipeline also said it would hold off on new LNG terminal decision in a fourth quarter earnings call.

Enterprise Gains Deepwater Port License for SPOT Offshore Texas

2024-04-09 - Enterprise Products Partners’ Sea Port Oil Terminal is located approximately 30 nautical miles off Brazoria County, Texas, in 115 ft of water and is capable of loading 2 MMbbl/d of crude oil.

Enbridge Announces $500MM Investment in Gulf Coast Facilities

2024-03-06 - Enbridge’s 2024 budget will go primarily towards crude export and storage, advancing plans that see continued growth in power generated by natural gas.