If 2016 was the year of cutting costs, 2017 was finally the year of cutting stocks.

2017 was another volatile year for oil markets, with prices finally appearing on track to a sustainable recovery after several false starts. As the year winds to a close, Stratas Advisors offer a look back at the path prices have charted, and some of the key events impacting oil markets this year. Stay tuned next year as Stratas Advisors start the year with an overview of 2018 Themes and Risks.

If 2016 was the year of cutting costs, 2017 was finally the year of cutting stocks. Global inventories began drawing consistently, and now OECD stocks are very close the five-year average goal that OPEC has championed. While the data outside of the non-OECD is less transparent, available indicators all point to tightening balances.

Several notable events also happened that, while not directly impacting oil prices, certainly had an impact on perceptions of global risk and forecasts of future economic growth. Oil markets have generally shrugged off most geopolitical risk since the price crash of 2014, with oversupply seen as sufficient to cover any potential disruptions. However, as balances have slowly tightened geopolitical risk is again able to move the needle on prices. Into this climate, Donald Trump was sworn in as President of the U.S. while in Europe a string of elections led to a wave of right-wing party victories. In the Middle East, Saudi Arabia has been undergoing significant changes, announcing a new Crown Prince and launching a national corruption crackdown that ensnared several members of the royal family. Additionally, tensions between Saudi Arabia and Qatar came to a head, with the former being “frozen out” by its regional contemporaries and marking another escalation in the proxy conflict between Saudi Arabia and Iran.

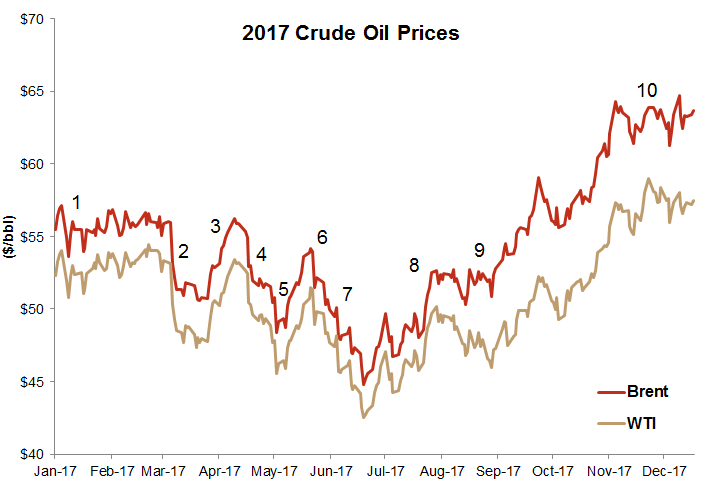

2017 Price Path

1. Prices stable after OPEC agrees to an output cut.

Prices started 2017 trading in a stable range after OPEC and non-OPEC allies reached an agreement in late-2016 to limit crude oil production. During this time, managed money net longs for both Brent and West Texas Intermediate were increasing to new record levels.

2. Prices drop after several reports of large crude stock builds in the U.S.; drop is exacerbated by traders unwinding record long positioning.

Sentiment suddenly shifted after several large crude builds were reported in the EIA’s Weekly Petroleum Status Report despite no actual change in the trajectory of fundamental balances. Traders quickly unwind long positions, further exacerbating the price drop. Sudden shifts in trader sentiment, despite a lack of evidence that the fundamental picture has changed could be a risk in 2018 as well.

3. Prices rise on positive U.S. weekly fundamental data and rebound from March drop.

Prices stabilize and again rise as weekly data continues to show that re-balancing is underway and OPEC and its non-OPEC allies continue adhering to their output agreement.

4. Refinery maintenance contributes to stock builds, dropping prices.

Extended spring refinery maintenance both within and outside of the U.S. lowers crude runs and leads to stock builds. Given the opacity of international crude data and lack of comprehensive international maintenance schedules the cause is not immediately confirmed and prices fall.

5. Maintenance ends, and crude draws resume, supporting prices.

Crude stocks in the U.S. and internationally are again drawing, supporting prices and sentiment.

6. Prices rise on growing expectations that OPEC will extend and deepen current production cuts.

Optimism takes over leading into the mid-year OPEC meeting, despite clear signaling from OPEC members that a significant change to the arrangement was unlikely. Prices rise as markets begin to expect that OPEC will deepen the crude oil production cuts in order to speed up the pace of re-balancing given the fluctuations in balances seen throughout the first half of the year.

7. Prices fall after OPEC does not deepen cuts and traders are concerned about falling shale costs and rising global supply.

Markets are unimpressed with OPEC’s decision to maintain production volumes at their current levels and instead extend the output deal through March 2018. Prices quickly succumb to downward momentum. Markets don’t expect the OPEC deal to go on forever, but they will spend much of 2018 looking for clear verifiable signs that progress on an exit strategy are being made.

8. Prices steadily rise on visibly improving fundamentals.

Despite concerns early in the year, summer refined product demand is strong, refinery runs are high and crude stocks across the board begin to draw. With evidence that the OPEC deal is still working despite increases from exempt countries Libya and Nigeria, sentiment also improves and managed money net longs again increase.

9. Hurricane Harvey makes landfall and churns across the U.S. Gulf Coast, flooding refineries and causing extensive damage throughout the region.

Hurricane Harvey made landfall in Texas on August 25, 2017, and churned across the region for a week generating record levels of rainfall. At its peak, the storm took approximately 3.5 MMbbl/d of refining capacity offline as well as a significant chunk of offshore crude production. Despite the extensive damage, recovery for most affected oil facilities was relatively swift once the flooding eased.

10. OPEC extends the oil output deal agreed to in 2016 through the end of December 2018.

At its annual November meeting OPEC surprised markets by extending the supply deal in place through the end of 2018 and placing additional caps on Libyan and Nigerian production. This decision and evidence of compliance has since supported prices at their highest levels all year.

Recommended Reading

US Gulf Coast Heavy Crude Oil Prices Firm as Supplies Tighten

2024-04-10 - Pushing up heavy crude prices are falling oil exports from Mexico, the potential for resumption of sanctions on Venezuelan crude, the imminent startup of a Canadian pipeline and continued output cuts by OPEC+.

What's Affecting Oil Prices This Week? (Feb. 26, 2024)

2024-02-26 - Stratas Advisors forecast that global crude production will be essentially unchanged from 2023, which means that demand growth in 2024 will outpace supply growth.

US Oil Stockpiles Surge as Prices Dip, Production Remains Elevated

2024-02-14 - EIA reported crude oil stocks increased by 12.8 MMbbl as February began, far outstripping expectations.

Oil Broadly Steady After Surprise US Crude Stock Drop

2024-03-21 - Stockpiles unexpectedly declined by 2 MMbbl to 445 MMbbl in the week ended March 15, as exports rose and refiners continued to increase activity.

Oil Dips as Demand Outlook Remains Uncertain

2024-02-20 - Oil prices fell on Feb. 20 with an uncertain outlook for global demand knocking value off crude futures contracts.