A floating liquefied natural gas or FLNG unit at sea. (Source: Shutterstock)

Westwood Global Energy Group is forecasting engineering, procurement and construction (EPC) contracts related to floating LNG (FLNG) developments reaching $35 billion over the next several years.

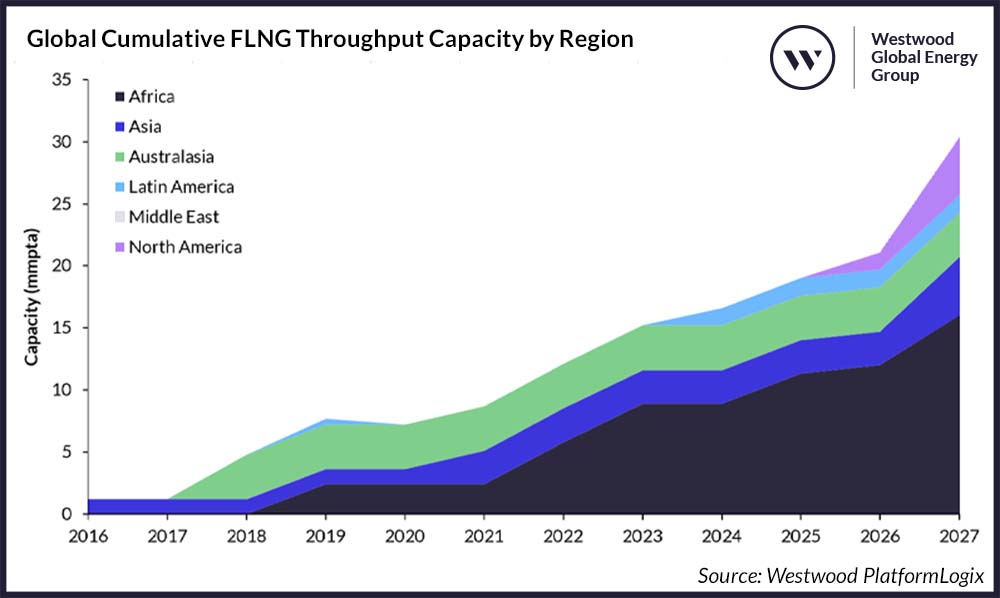

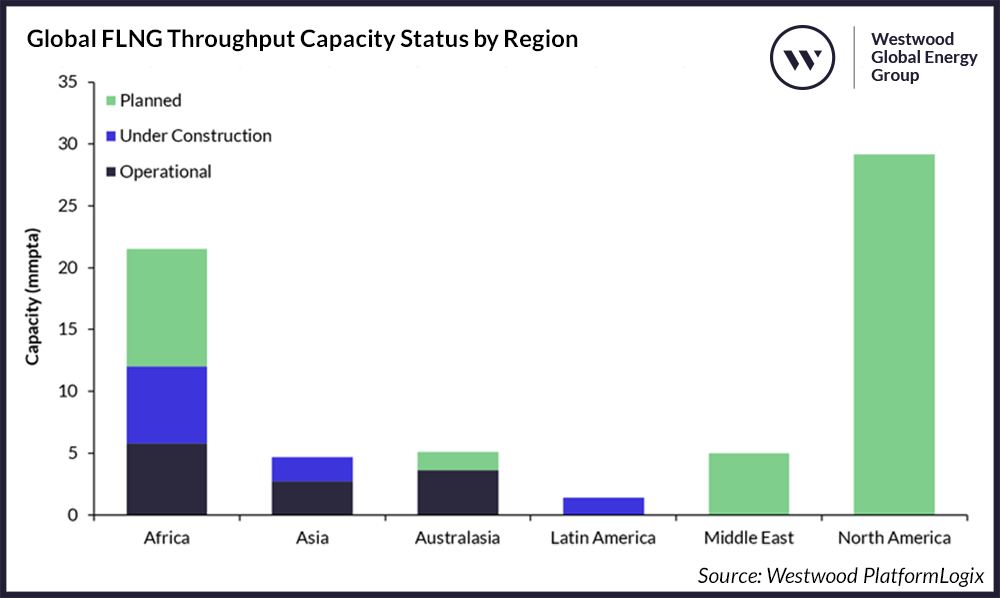

By the end of the 2023-2027 period, Westwood expects an additional 18.3 million tonnes per annum (mtpa) of FLNG capacity onstream, with initial EPC contract awards valued at $13 billion.

Through 2027, a further 36.5 mtpa is anticipated to come onstream post-2027 from sanctioned FLNG units, adding an additional $22 billion of EPC contracts, Westwood announced on April 4 on its website.

“With increasing energy demand and the challenges of energy security, the need for gas to meet the immediate and medium-term energy demand is driving investments in the FLNG market, given the role gas will play in transitioning to a low-carbon energy future,” the London-headquartered consultancy said.

Future LNG supply is expected to continue to rise in coming years, especially from the U.S. and Qatar, according to the Energy Information Administration. The decision by Russia’s President Vladimir Putin to invade Ukraine in February 2022 has boosted demand for LNG imports in the U.K. and Europe to replace reduced Russian energy supply.

“The current risk is that this will lead to an oversupply in the market and push out riskier and higher cost projects,” Westwood said. “This means that FLNG developments must focus on its differentiator to compete — including its speed to market and flexibility.”

While the demand outlook for LNG remains robust, the rise in coal-to-gas switching and further industrialization in Asia (mainly China and India) creates a key growth opportunity for LNG, according to Westwood.

“The significant drive to develop renewables and other new energies (such as hydrogen) in Europe and more mature Asian markets (including the traditional LNG demand markets of Japan, Korea and Taiwan, as well as China), could represent a downside risk for the sanctioning of additional FLNG capacity post-2030,” Woodside added.

Recommended Reading

Shell Brings Deepwater Rydberg Subsea Tieback Onstream

2024-02-23 - The two-well Gulf of Mexico development will send 16,000 boe/d at peak rates to the Appomattox production semisubmersible.

Stena Evolution Upgrade Planned for Sparta Ops

2024-03-27 - The seventh-gen drillship will be upgraded with a 20,000-psi equipment package starting in 2026.

Shell Taps TechnipFMC for 20K System for Sparta

2024-02-19 - The deepwater greenfield project in the Gulf of Mexico targets reserves in the high-pressure Paleogene reservoir.

Rystad: More Deepwater Wells to be Drilled in 2024

2024-02-29 - Upstream majors dive into deeper and frontier waters while exploration budgets for 2024 remain flat.

E&P Highlights: April 1, 2024

2024-04-01 - Here’s a roundup of the latest E&P headlines, including new contract awards.