[Editor's note: This story previously ran on HartEnergy.com. A version of this story also appears in the July 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

The drive for oil in the prolific Permian Basin has generated two main byproducts with nowhere to go: huge volumes of natural gas and more than 500 million gallons of water per day.

Some Permian operators have largely resorted to flaring excess gas due to limited takeaway options. However, water produced from drilling is a different story. Each day, the Permian Basin produces three times as much water as oil, which creates a challenge with fewer easy solutions.

In short, “you can’t flare water,” said Stephen M. Johnson, president and CEO of WaterBridge Resources LLC.

WaterBridge was among the first companies to carve out a niche in the water midstream business after seeing the struggle that Permian operators could face. The company has since emerged as one of the top water companies serving the Delaware Basin.

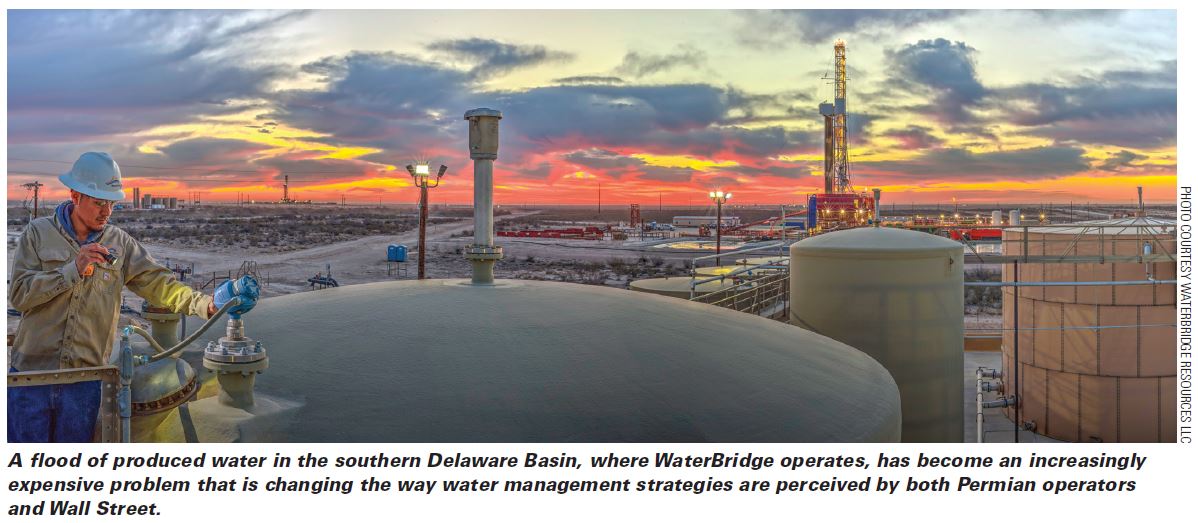

The company owns and operates an integrated system of disposal wells and pipelines primarily in the southern part of the Delaware where a flood of produced water has become an increasingly expensive problem that is changing the way water management strategies are perceived by both operators and Wall Street. “If you’re going to produce your hydrocarbons, you have to be able to do something with your water,” Johnson told Hart Energy at WaterBridge. “Whether it’s recycling and reuse or whether it’s disposal, you have to do something with it. Water handling is one of the primary constraints that a producer must manage.”

Ryan Duman, principal analyst with Wood Mackenzie’s Lower 48 upstream team, estimates that operators in the Permian Basin are generating roughly 12 million barrels per day (MMbbl/d) of produced water and growing. By comparison, the Permian produces a little over 4 MMbbl/d of oil, according to estimates by the U.S. Energy Information Administration in March.

“There is more water being produced than oil in the Permian and that trend is expected to continue,” Duman told Hart Energy.

Depending on the crude forecast, Duman believes the basin could easily reach 19 to 20 MMbbl/d of produced water by 2025.

Steven R. Jones, executive vice president and CFO at WaterBridge, noted that the Permian Basin is actually a water basin with an oil problem.

“It’s always been perceived that water is just a byproduct—which it is, in the sense that producers are not looking for water—however, it also happens to be the main product of the basin,” Jones said.

However, with the growth in produced water come operational and cost risks for U.S. shale producers.

Produced water is not a new development for the Permian Basin. However, Duman said, the volume of produced water has caught the industry off guard, especially as operators have expanded pad development activity west into the Delaware Basin.

Water-to-oil ratios in the Midland Basin range between 1.5:1 and 3.5:1 whereas ratios in the Delaware Basin are typically twice that, Jones said.

Produced water volumes have grown so fast and so high in the southern Delaware that operators have been unable to cheaply reinject all those volumes. Also, water handling can be expensive, ranging between $0.50 and $3 per barrel, including sourcing, transport, disposal and recycling, according to Wood Mackenzie.

Water Opportunity

In the desert landscape of the Permian Basin, water has become a crucial topic in the oil and gas industry. However, it’s not just scarcity and transportation that confront operators, but the millions of barrels of produced water that E&Ps are left with after flowing back their wells.

Wood Mackenzie estimated in June 2018 that saltwater disposal now comprises 40% of total lease operating expenses in the Permian. Trucking availability and the proximity of a well or pad to existing saltwater disposal wells are the biggest factors in cost.

As producers grapple with diminishing well production rates and other drags on profit, some U.S. shale producers have divested water infrastructure and its associated headaches to third-party service providers such as WaterBridge.

The company’s founder, Johnson, said he recognized the opportunity to create a pure-play water midstream company from his time as a senior executive at fluids management business Nabors Industries Inc.

WaterBridge was formed in December 2015 with an initial equity commitment of up to $200 million from private-equity firm Five Point Energy LLC to acquire, develop and manage water infrastructure for upstream producers.

Before launching WaterBridge, Johnson had served as president and COO of Nabors Well Services Inc. until C&J Energy Services Inc. acquired Nabors’ completion and production services business. The $2.9 billion transaction was completed in March 2015.

During his time with Nabors, Johnson oversaw 3,500 professionals in 15 states and Canada, about $1 billion in annual revenue and 29 saltwater disposal wells in Texas, New Mexico, Oklahoma and North Dakota.

WaterBridge initially targeted opportunities in conventional and emerging resource plays throughout North America. But by late 2017, the company’s commitment from Five Point had increased to $500 million.

Johnson said the business strategy was to replace water trucks by building a large footprint of water pipelines and disposal systems in a particular area.

“The genesis of WaterBridge was essentially taking the business that has been dominated by energy service companies and moms and pops and transforming it into a traditional midstream business,” he said. “We gather and process water instead of gathering and processing gas or crude.”

Johnson’s strategy eventually took WaterBridge to the Permian Basin with the acquisition of EnWater Solutions LLC in August 2017. The company also acquired water infrastructure assets in Oklahoma’s Arkoma Basin in September 2017.

EnWater was a produced water and gathering disposal company founded by Jason Long, who now serves as WaterBridge’s executive vice president and chief commercial officer. He and other EnWater executives, Michael Reitz and Cody Allen, joined WaterBridge with the acquisition to support future growth of the newly combined midstream platform.

EnWater’s assets, which at the time included five saltwater disposal wells with 25 miles of interconnected gathering pipeline and nearly 150,000 bbl/d of permitted disposal capacity, would become WaterBridge’s Permian platform.

At the time of the EnWater deal, WaterBridge initially expected to double its position in the southern Delaware Basin by year-end 2018, with 300,000 bbl/d of permitted disposal capacity.

However, WaterBridge’s growth has far exceeded expectations, with the company recently announcing that it began 2019 with approximately 1.2 MMbbl/d of permitted disposal capacity.

‘Wild West’

Wall Street has also taken notice of West Texas’ water management needs. Wood Mackenzie recently called the water management business the industry’s new golden goose.

Jones, WaterBridge’s CFO, discussed the importance of differentiating the midstream model and the service model with respect to water for the investment community, but Jones noted that ths mindset is evolving rapidly.

In December, WaterBridge entered into $800 million of debt facilities led by SunTrust Robinson Humphrey Inc. with a syndicate of 15 financial institutions.

However, the water business remains fragmented, Wood Mackenzie’s Duman said.

With the recent number of management teams in the water business receiving funding, he said “it feels almost like the Wild West out there.”

WaterBridge has continued to grow and currently has 1.2 MMbbl/d of produced water disposal capacity connected via 300 miles of pipeline throughout the southern Delaware Basin. The company’s Permian platform also has roughly 285,000 dedicated acres under long-term contracts from a dozen producers.

Long noted that WaterBridge has grown its position in the Delaware Basin organically and through acquisitions. He estimates the company has built more than half of its water handling facilities and about 75% of the pipe. The rest was primarily acquired from producers.

Within the past year, WaterBridge acquired the water midstream assets of upstream operators Concho Resources Inc. and Halcón Resources Corp. The company also picked up the southern Delaware Basin water infrastructure assets of NGL Energy Partners LP.

“It’s taken a while to earn their trust, and a lot of that’s come with just operating the system as we have and also expanding our footprint,” he said.

Long has been working with WaterBridge’s customers for five years or longer, including his time with the company’s predecessors.

“They’ve given up portions of it at a time,” he continued. “But to hand over 100% of their water handling needs—that really hadn’t happened until the last year.”

Duman noted that Wood Mackenzie expects more consolidation in the water midstream market down the road.

“Just given the size geographically of the Permian, there’s probably opportunities to combine some of these companies so that you get a good amount of scale with pipelines and SWD [saltwater disposal] networks just really offset, offering something that is truly a value add for your E&Ps,” he said.

The management team at WaterBridge believes the water midstream business has the market opportunity to be as large as the crude oil and gas midstream sector. And thanks to “the ideas that Steve Johnson, our sponsor, Five Point, and Jason [Long] were all separately working on,” Jones said WaterBridge has a first-mover advantage.

“That’s the evolution they expected in the market, and it’s exactly what’s happened now,” he said. “They were all just ahead of that transformation.”

Recommended Reading

Google Exec: More Collaboration Needed for Clean Power

2024-04-17 - Tech giant Google has partnered with its peers and several renewable energy companies, including startups, to ramp up the presence of renewables on the grid.

US Geothermal Sector Gears Up for Commercial Liftoff

2024-04-17 - Experts from the U.S. Department of Energy discuss geothermal energy’s potential following the release of the liftoff report.

Hirs: Aspirations Meet Reality—The Undisclosed High Cost of the Energy Transition

2024-04-16 - The nation is trying to keep up with the growth of renewable power resources, but before transmission lines can be built, the power plants must first have interconnects with the grid.

Nova Clean Energy Acquires BNB’s 1-GW HyFuels Portfolio in Texas

2024-04-16 - Covering about 25,000 acres on the Texas Gulf Coast, HyFuels’ power supply will be split evenly between wind and solar energy.