For well more than a year, the U.S. has been in a battle of attrition with OPEC, which has pumped nearly all the oil it could to win “market share.”

The result has been a flat lining of crude oil prices.

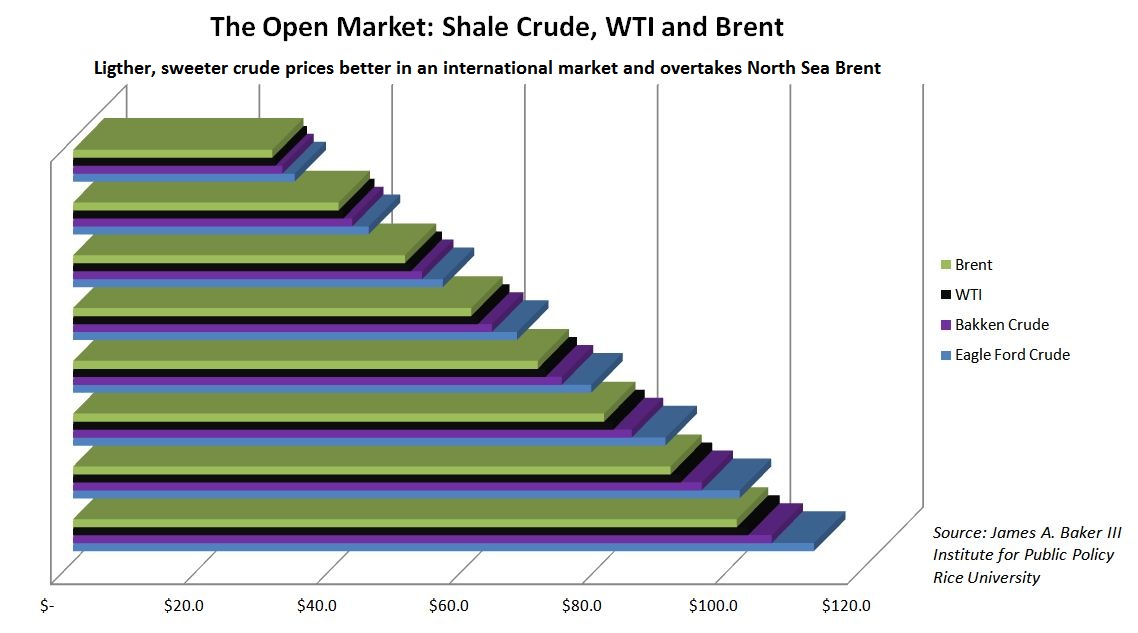

For much of the shale boom, the Eagle Ford and Bakken oil—often of a much higher quality than West Texas Intermediate (WTI) and Brent—has been trapped in domestic markets. Now, with the lifting of the crude oil export ban on Dec. 18, that oil can now find a more fitting and lucrative place for its lighter, sweeter crude.

Some E&Ps are already eager to get their product out. Pioneer Natural Resources (NYSE: PXD) said Dec. 18 it would be capable of exporting crude by mid-2016. The company has been actively working with its midstream partners to secure export facilities on the U.S. Gulf Coast.

The swift passage Dec. 18 strikes down an export ban that limited domestic producers. A few changes are in store in the next 18-24 months.

Sweet Crude

U.S. production is set to decline in 2016 and may fall in 2017 as well. But with an open market, the backlog at Cushing, Okla., could be relieved within 18-24 months, resulting in higher wellhead prices for E&Ps.

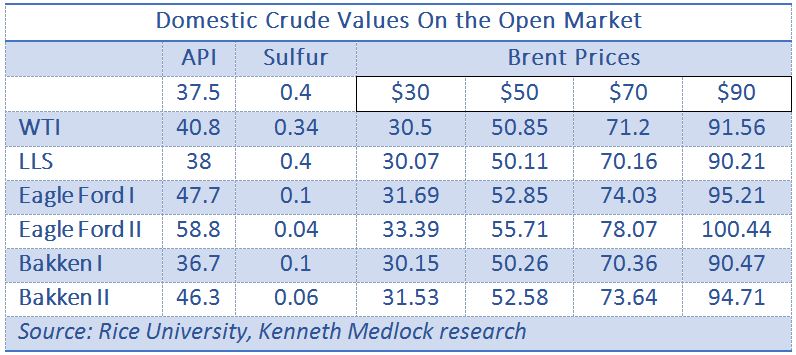

Kenneth Medlock, senior director of the Center for Energy Studies at Rice University’s Baker Institute for Public Policy, said that lifting the ban should level the playing field for the U.S. Oil from the Bakken and Eagle Ford is superior in quality but has faced discounted domestic crude-oil prices relative to internationally traded crudes such as Brent.

In a study published in March, Medlock found that if the majority of light tight oil produced from U.S. shale formations was exported, it would fetch higher prices than WTI and Brent in the international market because it is of higher quality.

With oil locked inside the U.S., oil producers had little choice but to discount light oil to refiners.

But in the international market, higher API numbers—meaning lower density—tend to raise the price of crude relative to Brent while higher sulfur content tends to lower the price relative to Brent.

WTI typically has a higher API and lower sulfur content than Brent, making it more valuable. Some oil produced in the Bakken and Eagle Ford has far lower density than WTI.

Development in the Bakken and Eagle Ford shales has driven the bulk of the increase in domestic crude oil production to date, but it’s been sold for a discount because of the configuration of U.S. refineries.

Based on their open market values, Medlock calculated that at $100 Brent prices, WTI would trade at nearly $102 while Eagle Ford crudes would fetch prices of $111. And in an unconstrained market, those crudes would already be delivered at a premium.

Medlock, however, offered a cautionary statement.

“In reality the U.S. is still going to be a net importer of crude,” he said.

The U.S. will have to find the right match for the gravity of crude being produced.

In the interim, Barclays analyst Michael Cohen said he expected U.S. production declines and increased processing capacity may see the Gulf Coast begin importing light oil volumes that have only recently been displaced.

“Declining output and increased regional demand may cause regional crudes to trade at a premium to comparable international grades, and WTI may trade at a sustained premium to Brent, which could encourage imports,” Cohen said. “What’s more, to gain global market share, U.S. crude traders would need to sell U.S. crudes at levels that would incentivize refiners to test new crudes in their input slate.”

Places To Go

The U.S. already exports more than 700 thousand barrels per day (Mbbl/d) of crude and processed condensate.

Now that oil markets are open, the question is where U.S. shale oil might find new refineries.

Pioneer was among the leaders in exporting Eagle Ford Shale condensate after receiving a green light from the U.S. Department of Commerce’s Bureau of Industry and Security.

The company is already eyeing markets where it can find a foothold for production. Pioneer said Europe, Asia and Latin America are potential markets for U.S. crude as countries from these areas would realize economic and security advantages by diversifying their sources of supply.

“After witnessing the success of condensate exports from the Eagle Ford Shale, the logical next step was to lift the ban on crude exports,” said Timothy L. Dove, Pioneer’s president and COO. “We are pleased that policymakers on both sides of the aisle engaged collectively on this issue.”

Cohen agreed, saying that certain regions will be more welcoming to imports than others. They include Mexico and Latin America.

“We expect U.S. crudes, especially light ones, to have a natural home in Mexico and other Latin American countries whose crude slate is increasingly heavy,” he said. “These countries are closer than other potential markets and would benefit from the higher gasoline and naphtha yields of lighter U.S. grades given their heavier production slate.”

Europe could also be an export target as North Sea crude oil production declines. However, the U.S. would face steep competition from supplies from the Middle East, Africa, Caspian and Russia, Cohen said.

“Though energy security concerns may compel some countries, such as Poland and the Baltic states, to seek U.S. crudes, the U.S. crude footprint in Europe is likely to remain limited to special market circumstances due to high cost and the need for higher distillate cuts,” Cohen said.

In Asia, buyers have been experimenting with lightly processed U.S. condensate in the last year as Asian condensate demand has grown.

However, competing with African grades would mean the U.S. would have to ship via smaller tankers on a journey that would take six days longer because of logistics.

As with any global commodity, U.S. production will be dependent on the overall global price as well as finding appropriate markets, said John Kneiss, director of macroeconomics, geopolitics and policy for Stratas Advisors.

Heavy crude production, for instance, will continue to be used in the U.S. because the nation’s refinery configurations are designed to handle that.

“The lighter crudes coming out of the shale deposits and other formations will be competing against the North Sea and other producers out of Africa and the Middle East,” he said. “Certainly we think there’s going to be some opportunity in the Asian market, probably some opportunity in the South American market.”

Contact the author, Darren Barbee, at dbarbee@hartenergy.com.

Recommended Reading

NOV's AI, Edge Offerings Find Traction—Despite Crowded Field

2024-02-02 - NOV’s CEO Clay Williams is bullish on the company’s digital future, highlighting value-driven adoption of tech by customers.

Marathon Petroleum Sets 2024 Capex at $1.25 Billion

2024-01-30 - Marathon Petroleum Corp. eyes standalone capex at $1.25 billion in 2024, down 10% compared to $1.4 billion in 2023 as it focuses on cost reduction and margin enhancement projects.

Humble Midstream II, Quantum Capital Form Partnership for Infrastructure Projects

2024-01-30 - Humble Midstream II Partners and Quantum Capital Group’s partnership will promote a focus on energy transition infrastructure.

Hess Corp. Boosts Bakken Output, Drilling Ahead of Chevron Merger

2024-01-31 - Hess Corp. increased its drilling activity and output from the Bakken play of North Dakota during the fourth quarter, the E&P reported in its latest earnings.

The OGInterview: Petrie Partners a Big Deal Among Investment Banks

2024-02-01 - In this OGInterview, Hart Energy's Chris Mathews sat down with Petrie Partners—perhaps not the biggest or flashiest investment bank around, but after over two decades, the firm has been around the block more than most.