After a breathtaking performance in the first quarter, the Permian Basin appears to have lost some of its steam heading into the end of the second. (Source: Hart Energy)

The recent dominance of Permian Basin A&D—while firmly intact—seems to have sputtered in its sheer audacity as the second quarter begins to wrap.

While first-quarter megadeals were almost exclusively in the Permian—accounting for about $12.7 billion in value—that has shifted through June 23. The second quarter’s largest deals were instead in the Appalachia and San Juan basins.

EQT Corp.’s (NYSE: EQT) $8.2 billion headliner acquisition of Rice Energy Inc. (NYSE: RICE) not only helped prop up A&D values late in the quarter but also opened up the question of whether broader consolidation might be on the way.

RELATED: Empire Building: EQT Targets Balance After $8.2 Billion Rice Conquest

At Wells Fargo Securities’ West Coast Energy Conference, some of the largest shale producers chewed over the benefits of EQT’s deal, with conversations centering on the benefits of scale and longer laterals.

Such deals make “sense on paper” but E&Ps lack urgency in engaging in the market, David Tameron, senior analyst at Wells Fargo, said in a June 22 report. “The volatility of crude prices has created a difficult bid-ask environment, and many companies are hesitant to sell when being priced off 52-week lows,” Tameron said.

Swaps, trades and deals—including Jones Energy Inc.’s (NYSE: JONE) June 22 Arkoma Basin sale for about $67.5 million—appear to remain on the table, but a flurry of larger corporate combinations still seems to be a ways off.

Consolidation among large publics seems logical with the land grab nearly over and no new, scalable basin to rush toward, Tameron said. Commodity prices also appear range-bound and coring up acreage allows for longer and more profitable lateral wells.

“We continue to believe that given stronger balance sheets, already deep inventories and continued commodity volatility, consolidation is more likely to take place in 2018 and beyond,” he said.

Through June 22, E&Ps announced $17.8 billion worth of deals in the second quarter compared to the full first quarter’s $19 billion tally, according to Hart Energy data.

EQT’s deal and two by Occidental Petroleum Corp. (NYSE: OXY) that totaled $1.2 billion—both announced June 19—made up more than half of the second quarter’s total.

Shale Trade Deficit

In the Permian Basin, executives at Parsley Energy Inc. (NYSE: PE), Occidental and Matador Resources Co. (NYSE: MTDR) see consolidation coming in phases, with coring up on a smaller scale and swap and trades creating contiguous blocks.

The Permian’s upside edge is partly a function of what its producers cannot yet extract from the ground. Production just scratches the surface of the basin’s total recoverable oil at around 8% to 10%. That’s fueled a kind of shale trade deficit in which E&Ps sell assets in other basins to continue coring up in the Midland and Delaware basins.

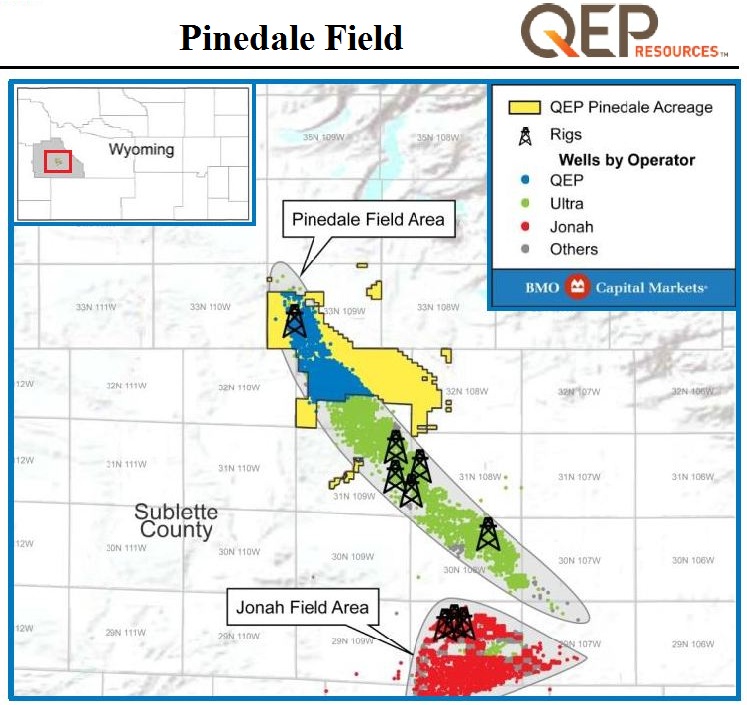

Since April, QEP Resources Inc. (NYSE: QEP) has marketed its Pinedale Anticline Field assets in Sublette County, Wyo., through BMO Capital Markets. QEP has earmarked proceeds to at least partially add inventory elsewhere.

In first-quarter 2017, the Pinedale assets produced an average of 234 million cubic feet equivalent per day (MMcfe/d) and about $14 million of operated cash flow per month.

Brian Velie, an analyst with Capital One Securities, estimates the asset is worth $625 million. However, in June Linn Energy Inc. closed the sale of acreage in the Jonah and Pinedale fields in Wyoming for a solid $581.5 million.

Linn’s sale metrics could up the price of QEP’s assets closer to $1 billion, Velie said in a May report.

During first-quarter 2016, QEP recorded a $1.1 billion impairment on the Pinedale assets due to lower commodity prices. The company is optimistic that it will reach a deal in the coming weeks, Tameron said.

QEP said it is looking at additional acquisitions based on zone values rather than acreage prices and prefers concentrated positions with more locations per surface acre to maximize drilling.

Elsewhere in the Permian:

- Parsley

Parsley plans to work on swaps to block up acreage it acquired in April from Double Eagle Energy Permian LLC for $2.8 billion. With a $600 million war chest, the company noted that a prolonged period with oil prices in the $30s would make management re-think its capital, growth and outspend.

- Carrizo

Carrizo Oil & Gas Inc. (NYSE: CRZO) continues to monitor A&D markets but can afford to be selective with the need to replace only about 4,000 acres annually to keep inventory flat, Tameron said.

Eagle Ford Rally

WildHorse Resource Development Corp.’s (NYSE: WRD) $625 million deal to buy about 111,000 net acres in the Eagle Ford Shale is expected to close at the end of June. WildHorse did not rule out further acquisitions but the company will most likely fill in and block up its current acreage for now, Tameron said.

WildHorse’s deal with Anadarko Petroleum Corp. (NYSE: APC) and affiliates of Kohlberg Kravis Roberts & Co. LP (KKR) was among roughly $3.9 billion in deals announced in the first half of 2017.

Midcontinent

Jones Energy continues to track toward the Merge Play in Oklahoma as the company said June 22 it would exit the Arkoma Basin through deals worth up to $67.5 million.

Jones said the Arkoma deals consist of a $65 million cash payment and up to $2.5 million in a contingency payment based on improving natural gas prices. The sale will reduce the company’s borrowing base by $50 million, Tameron said.

As of May 1, Continental Resources Inc. (NYSE: CLR) still had about 25,000 net acres for sale in the Merge and Jones management said prices in the play could reach $20,000 per acre by year-end, Seaport Global Securities said.

Continental’s Merge acreage averages 50 barrels of oil equivalent per day and is prospective for the Woodford and Mississippian.

Continental is chasing divestitures of at least $500 million in 2017 in an effort to reduce debt to $6 billion. The company had about $6.51 billion in debt as of March 31.

Darren Barbee can be reached at dbarbee@hartenergy.com.

Recommended Reading

Hess Midstream Increases Class A Distribution

2024-04-24 - Hess Midstream has increased its quarterly distribution per Class A share by approximately 45% since the first quarter of 2021.

Equitrans Midstream Announces Quarterly Dividends

2024-04-23 - Equitrans' dividends will be paid on May 15 to all applicable ETRN shareholders of record at the close of business on May 7.

Genesis Energy Declares Quarterly Dividend

2024-04-11 - Genesis Energy declared a quarterly distribution for the quarter ended March 31 for both common and preferred units.

Moda Midstream II Receives Financial Commitment for Next Round of Development

2024-03-20 - Kingwood, Texas-based Moda Midstream II announced on March 20 that it received an equity commitment from EnCap Flatrock Midstream.

Enbridge Advances Expansion of Permian’s Gray Oak Pipeline

2024-02-13 - In its fourth-quarter earnings call, Enbridge also said the Mainline pipeline system tolling agreement is awaiting regulatory approval from a Canadian regulatory agency.