French major Total has deepened its roots in the North Sea and shored up core positions in other parts of the world with its $7.45 billion deal to acquire Maersk Oil and Gas.

The acquisition, which is still subject to regulatory approval and other legal requirements, is expected to lift Total’s output to 3 MMboe/d by 2019, making the company the second-largest operated producer and the third-largest resource holder in the North Sea. The deal is expected to close in first-quarter 2018 with an effective date of July 1, Total said in an Aug. 21 news release announcing the acquisition.

“This is a compelling transaction for Total and one that will add significant value for our shareholders,” Total CEO Patrick Pouyanné said on a conference call.

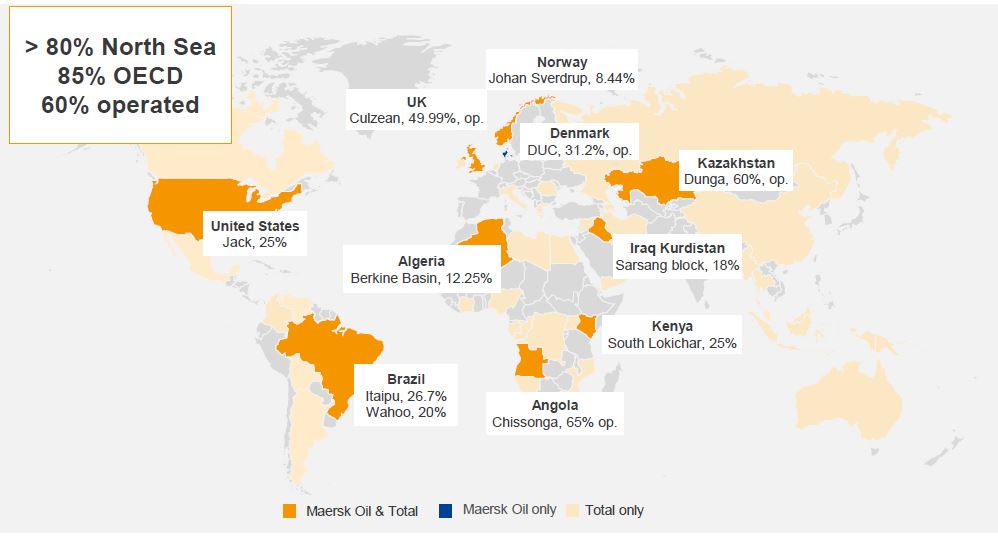

For assuming $2.5 billion of Maersk Oil’s debt and giving $4.95 billion in Total shares—or 97.5 million shares—to Maersk Oil parent company A.P. Møller-Maersk, Total will grow its reserves by about 1 Bbbl, more than 85% in OECD countries.

It also substantially adds to the company’s portfolio, mainly in the North Sea where Total will pick up Maersk Oil’s 49.99% working interest in the Culzean gas HP/HT field in the North Sea, an 8.44% interest in the Statoil-operated Johan Sverdrup development and assets offshore Denmark, including the country’s largest gas field, Tyra.

In addition, the acquisition allows Total to gain a stronger position in the U.S. Gulf of Mexico, where the two currently jointly develop hydrocarbons in the Wilcox Formation, and strengthen its position in Algeria.

Add to this possible upside offshore Angola, where Total pointed out the “potential cross-block development for deep offshore resources,” and “promising onshore discoveries” in Kenya along with the diversification provided by producing onshore conventional assets in Kazakhstan and Iraq Kurdistan and deeper stakes in Brazil’s presalt.

The deal, considered the biggest the North Sea has seen since Statoil’s nearly $30 billion acquisition of Norsk Hydro in 2006, comes as oil and gas companies continue to work toward lowering break-evens, keeping costs low and generating cash flow as they rebound from the prolonged downturn.

With free cash flow of more than $3.1 billion for first-half 2017, Pouyanné said Total has seen the benefits of its efforts.

“We are now in a position to be able to take advantage of the low-price environment” by pursuing new projects and acquiring resources in attractive conditions, Pouyanné said.

Maersk said the agreement to sell is part of its strategy to separate its oil and oil-related activities as it focuses on integrated transport and logistics.

“The valuation of Maersk Oil and Total’s commitment is a testament to the quality and standing of Maersk Oil,” A.P. Moller-Maersk CEO Søren Skou said in a statement. “In addition, the agreement will strengthen the financial flexibility of A.P. Moller-Maersk and free up resources to focus our future growth on container shipping, ports and logistics.”

Pouyanné said Total’s main rationale for the acquisition was its conventional OECD assets, which complements other assets in the company’s portfolio. It also complements the company’s international portfolio and creates synergies, including more than $200 million in cost synergies and about $100 million identified fiscal synergies per year.

To cope with oil prices, Total had planned to cut costs by $4 billion by year-end 2018, adjusting to lower oil prices, Reuters reported. Plans are to revise the target by mid-September. Pouyanne said the North Sea was one of the areas which face further cost savings to remain competitive, and the Maersk Oil deal offers it the opportunity to do so.

“In the U.K. in particular, we have two operations of similar size. There are 700 staff on both sides in Total UK and Maersk UK with more or less same size of assets,” he said in the Reuters article.

Job loss is a possibility given the overlap in operations.

“Obviously we’ll merge these two subsidiaries. At the end of the day, we will have the opportunity to do some rationalization,” Pouyanne said.

Valentina Kretzschmar, corporate service director for Wood Mackenzie, said the cost synergies should add value for Total, given the overlap in the North Sea.

Technology synergies are also present, Kretzschmar added, pointed out Maersk Oil’s expertise as a deepwater specialist skilled in EOR techniques.

“The deal will also reduce Total’s weighting toward areas of high aboveground risk,” Kretzschmar said in a statement. “There are a number of strategic drivers at play here. The acquisition improves Total’s near-term growth outlook—it provides Total with an immediate 6% production increase and strengthen near-term growth.

“It will further shift Total’s weighting toward OECD regions, a core strategic driver for the company as it looks to balance the portfolio away from areas of high above-ground risk,” Kretzschmar added.

In 2018, Total expects to add 160 Mboe/d, mainly liquids production, with estimated free cash flow break-evens were said to be less than $30/bbl. This could increase to more than 200 Mboe/d by the early 2020s.

Total is also maintaining its capex guidance, which remained unchanged at between $16 billion and $17 billion for 2017 and between $15 billion and $17 billion for 2018-2020.

Velda Addison can be reached at vaddison@hartenergy.com.

Recommended Reading

Range Resources Holds Production Steady in 1Q 2024

2024-04-24 - NGLs are providing a boost for Range Resources as the company waits for natural gas demand to rebound.

Hess Midstream Increases Class A Distribution

2024-04-24 - Hess Midstream has increased its quarterly distribution per Class A share by approximately 45% since the first quarter of 2021.

Baker Hughes Awarded Saudi Pipeline Technology Contract

2024-04-23 - Baker Hughes will supply centrifugal compressors for Saudi Arabia’s new pipeline system, which aims to increase gas distribution across the kingdom and reduce carbon emissions

PrairieSky Adds $6.4MM in Mannville Royalty Interests, Reduces Debt

2024-04-23 - PrairieSky Royalty said the acquisition was funded with excess earnings from the CA$83 million (US$60.75 million) generated from operations.

Equitrans Midstream Announces Quarterly Dividends

2024-04-23 - Equitrans' dividends will be paid on May 15 to all applicable ETRN shareholders of record at the close of business on May 7.