The industry’s 50 largest publicly traded E&Ps posted their lowest combined revenue since 2016 at $110.8 billion. (Source: Shutterstock.com)

The oil industry’s economic highs and lows isn’t unfamiliar territory for producers, but the downturn of 2020 brought unprecedented losses in revenues, capex and reserves, a new EY study found.

Last year, the industry’s 50 largest publicly traded E&Ps posted their lowest combined revenue since 2016 at $110.8 billion, according to EY’s U.S. oil and gas reserves, production and ESG benchmarking study.

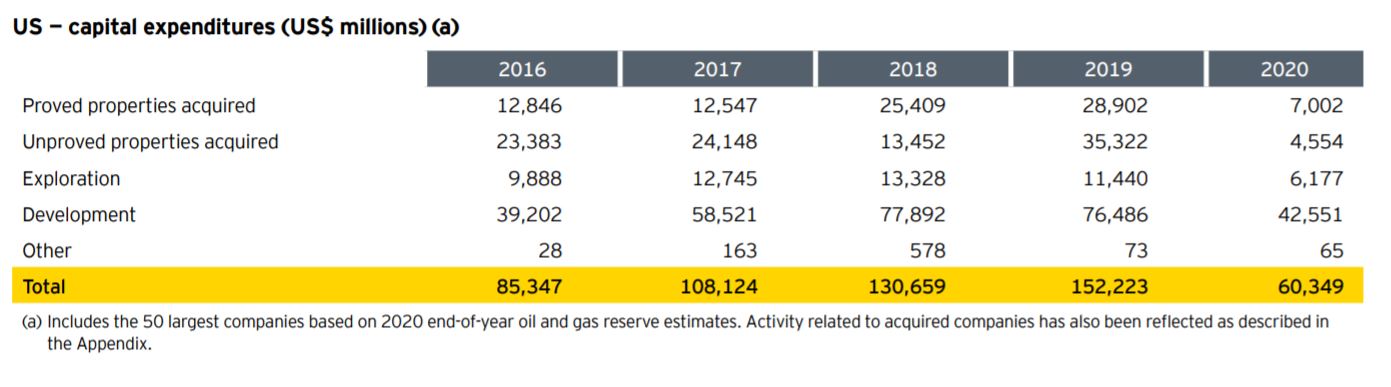

Additionally, the E&Ps reported a total capex of $60.3 billion in 2020, representing a 60% decrease from 2019. It was the lowest for the five-year study period compared to increases of 17%, 21% and 27% in 2019, 2018 and 2017, respectively.

The study attributed these losses to depressed commodity prices which were elevated by the COVID-19 pandemic. In return, the decline in oil prices caused impairment charges to triple, amounting to $66.6 billion—the highest for the five-year study period (2016 to 2020).

After-tax losses were $84.1 billion, the greatest loss during the period and the first loss since 2016, the study found.

“The lower commodity price environment of last year caused a significant drop in capex and significant impairments,” said Herb Listen, EY Americas energy and resources assurance leader. “Though prices have recovered, we haven’t seen a rebound in capex in 2021 and, as a result, likely won’t see a return in U.S. production to the same pre-pandemic levels. This will cause a ripple effect as the market struggles to meet recovering demand and may result in higher prices.”

Chevron Corp. was the leading purchaser of proved and unproved assets with its $6.4 billion acquisition of Noble Energy. The deal brought the company nearly 1 Bcf of international natural gas reserves.

PDC Energy Inc. followed with total property acquisition costs of $1.7 billion spent related to its merger with SRC Energy Inc., the study showed.

However, the E&Ps proven and unproven acquisitions totaled 7,002 and 4,554 last year—a significant decrease from 28,902 and 35,322 in 2019. The companies drilled 41% and 32% fewer development and exploration wells, respectively, compared to 2019, according to the study.

Investments in development expenditures from the integrated oil and gas companies decreased year-over-year by about one-third, while investments in development expenditures from the large independents and independents decreased by about half, the report concluded.

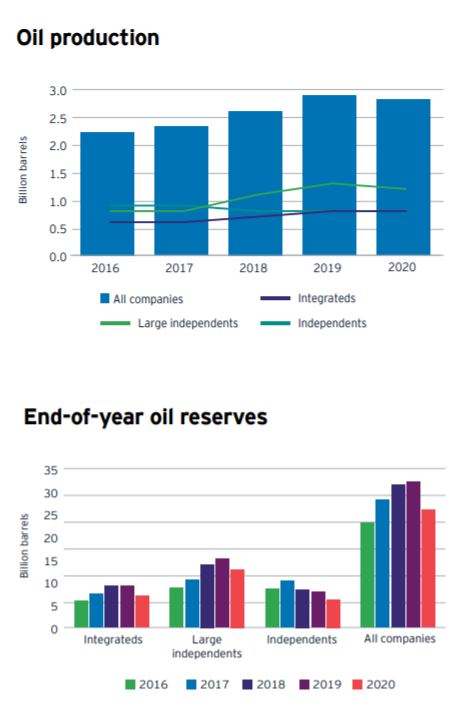

Oil production and gas production remained materially flat at 2.8 Bbbl and 13.2 Tcf, decreasing by only 2% since the record high in 2019.

According to the study, the largest increases were posted by Occidental Petroleum Corp. with 79 MMbbl and Chevron with 26 MMbbl likely due to the acquisitions of Anadarko and Noble Energy. ConocoPhillips and BP Plc posted the largest decreases—27 MMbbl and 21 MMbbl—due to reduced development spending and production curtailments in the low oil price environment.

The studied companies reported combined oil reserves of 26 Bbbl and combined gas reserves of 148 Tcf, decreases of 19% and 13%, respectively, compared with 2019. Downward reserve revisions totaled 5.2 Bbbl of oil and 21.3 Tcf of gas for 2020.

The largest downward revisions were reported by:

- Exxon Mobil Corp., 1.241 Bbbl;

- ConocoPhillips, 449 MMbbl;

- Occidental Petroleum Corp., 373 MMbbl; and

- Chevron, 350 MMbbl.

In 2020, more companies made commitments to reduce their CO2 emissions as ESG-focused goals gained ground. Nearly all of the large independents (93%), all of the integrateds, and 65% of the other independents have published sustainability or ESG reports.

The majority of the companies’ goals aligned with environmental topics (53%), while social topics accounted for 33%, and only 10% of the goals were dedicated to governance.

“ESG and sustainability have become essential to attracting capital and creating long-term value for all stakeholders,” Listen said. “Interestingly, very few companies in our study—only 16%—are providing third-party assurance over ESG metrics. Due to a lack of standardization and companies following various frameworks, the importance of third-party assurance to investors is going to grow.”

Recommended Reading

Some Payne, But Mostly Gain for H&P in Q4 2023

2024-01-31 - Helmerich & Payne’s revenue grew internationally and in North America but declined in the Gulf of Mexico compared to the previous quarter.

Uinta Basin: 50% More Oil for Twice the Proppant

2024-03-06 - The higher-intensity completions are costing an average of 35% fewer dollars spent per barrel of oil equivalent of output, Crescent Energy told investors and analysts on March 5.

In Shooting for the Stars, Kosmos’ Production Soars

2024-02-28 - Kosmos Energy’s fourth quarter continued the operational success seen in its third quarter earnings 2023 report.

M4E Lithium Closes Funding for Brazilian Lithium Exploration

2024-03-15 - M4E’s financing package includes an equity investment, a royalty purchase and an option for a strategic offtake agreement.

California Resources Corp. Nominates Christian Kendall to Board of Directors

2024-03-21 - California Resources Corp. has nominated Christian Kendall, former president and CEO of Denbury, to serve on its board.