As battles rage in Ukraine, economic battles could leave significant impacts, as well. (Source: Hart Energy; IHOR SULYATYTSKYY, Frederic Legrand – COMEO, Seneline/Shutterstock.com)

Three critical factors to keep on an eye on for global oil and gas markets: how Western sanctions against Russian-supplied energy play out; the Biden administration’s policy to weaken the grip of Russian energy over Europe; and how Russia responds to its adversarial energy trading partners.

Economic battles that spin out of control create the potential for oil to shoot up to $185/bbl—a level that experts say would trigger a global recession. That is a worst-case scenario, but one that was acknowledged by analysts from both the International Energy Agency (IEA) and J.P. Morgan at a March 23 conference hosted by Rice University’s Baker Institute for Public Policy.

Sanctions against Russia

Since Russia invaded Ukraine more than a month ago, Western countries have engaged in sanctions both against the country itself and individual Russians, particularly oligarchs and politicians. These are intended to restrict Western exports and cut off Russia from the international financial system.

But there is another type of sanction, a form of patriotic action in oil markets known as self-sanctions, that manifests in refusing to import Russian fossil fuels and related products.

On March 25, European patriotism found its limit when the EU decided not to pursue that strategy. Doing so would have had devastating consequences because, as recently as 2019, Russia supplied 29% of Europe’s crude imports and 51% of its petroleum product imports, according to BP.

Still, Shikha Chaturvedi, head of global gas strategy at J.P. Morgan, said she expects limited self-sanctioning to ultimately take 1 MMbbl/d of Russian oil off the markets permanently as buyers pursue other sources.

That is the chief factor that is driving J.P. Morgan’s price forecast for the second quarter, Chaturvedi said. “We’re already at $120 and we can still go higher from here.”

WTI fell to $103.40/bbl and Brent fell to $109.70/bbl on March 28 as concerns over COVID lockdowns in China’s most populous city of Shanghai spooked the markets.

Self-sanctions are particularly difficult in Europe because of a critical shortage of diesel. Diesel has long been popular in Europe because tax incentives made it cheaper than gasoline. The share of new cars with diesel engines in the EU shrunk from 52% in 2015 to 32% in 2019, according to Statista, but that is still a large share of the auto fleet. As a result, ending Russian imports of 760,000 bbl/d of gasoil and diesel is a non-starter in Europe.

Biden’s plan

On March 25, President Joe Biden and European Commission President Ursula von der Leyen announced a task force to both diversify LNG supplies and, ultimately, to reduce demand for natural gas. The plan begins with the U.S. supplying 15 Bcm of LNG this year and working with EU members to reduce the greenhouse gas intensity of LNG infrastructure and pipelines.

“It’s always been a balancing of addressing climate change while meeting our current energy needs and this announcement reflects that balancing act,” Jeff Nichols, partner and co-chair of the Haynes and Boone LLP energy practice group, told Hart Energy. “They put a thumb on the scale a little bit on the U.S. E&P side in terms of near-term needs. But in the long term, it still seems focused on long-term efforts to reduce climate change and reduce fossil fuel consumption.”

Russia’s gas sales to Europe have not strayed from contracted volumes in recent years and Europeans have done little to build up inventories, said Gil Porter, partner at Haynes and Boone. The result is that Europe’s stockpiles are pretty low right now. Gas Infrastructure Europe estimates that inventories are 22% below the five-year average and 10.7% below the level of a year ago.

Whether the U.S. can actually provide 15 Bcm to the EU market in 2022 is not a sure thing, as the parties alluded to in the announcement with the wording, “strive to ensure.” It would require an uptick in U.S. production that appears unlikely at this point.

“If you look at the LNG plants that are currently under construction, the earliest is not anticipated until 2024,” Porter said. “There’s a number of facilities coming online between 2024 and 2026. So, the real question is, are we looking short-term 2022, 2023? And if so, how are we going to handle the price elements that intersect between Asian demand and Europe demand, which would need a huge amount more than I think could be covered.”

The announcement is a good one for U.S. producers, Nichols said, if it leads to increased permitting for pipelines and LNG facilities.

Russian response

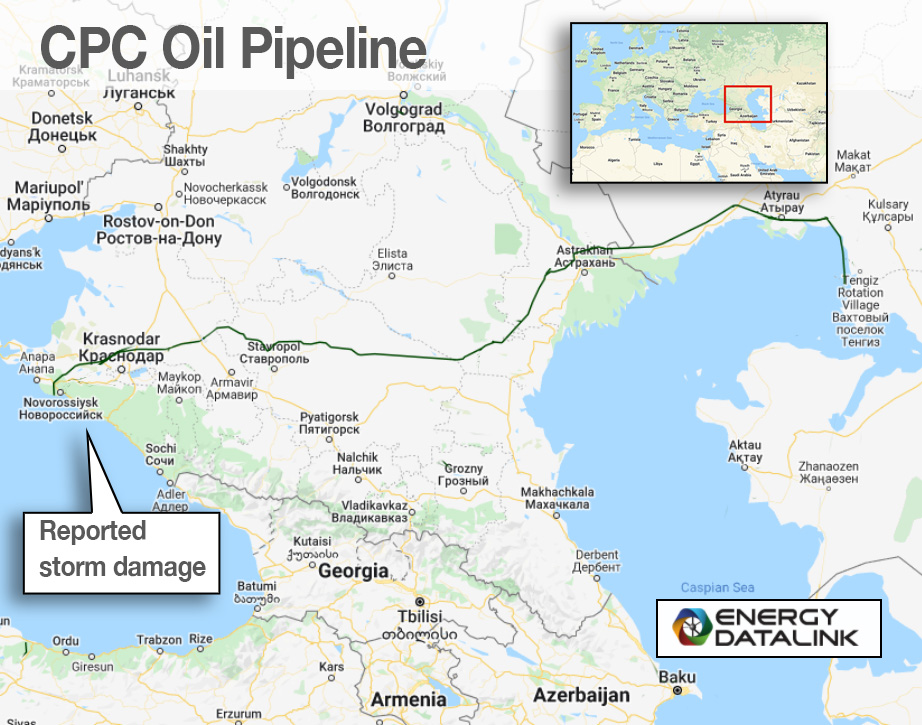

The shutdown of the Caspian Pipeline Consortium (CPC) oil pipeline on March 23 unnerved traders because it took 1 MMbbl/d to 1.5 MMbbl/d off the markets for an expected one to two months. Is it really storm-related damage that disabled two of the pipeline’s three mooring units at Russia’s Novorossiysk-2 Marine Terminal on the Black Sea coast? Experts have described the actual repairs as relatively simple, but the consortium that runs the pipe was quick to signal that delays were possible because western companies would not supply parts.

Russia has also insisted that “unfriendly” countries pay for their natural gas with roubles, a notion that was rejected by Germany and Italy, but not all European countries.

“It’s amazing how often people who are negotiating put a gun to their head and say don’t move or I’ll shoot, and that’s what it sounds like Russia’s story is right now,” Porter said. “But this is diplomacy and politics. Sometimes countries will do things that don’t necessarily make logical sense because they’re staking out turf and they’re willing to suffer for it. It doesn’t make a lot of sense that Russia would cut off Europe when it’s getting badly-needed currency.”

And don’t forget COVID

But while tight supply dominates the picture, there is a looming threat on the demand side.

“We are starting to see some impacts from COVID, the resurgence that’s happening in China,” Chaturvedi said.

J.P. Morgan anticipates a loss of 1.5 MMbbl/d of demand in the second quarter and 500,000-550,000 bbl/d in the third and fourth quarters as the latest Omicron variant sweeps through the U.K. toward another round in the U.S. In recent days, Shanghai has reported 1,500 cases a day.

“We don’t think it should be substantial in longevity because it’s less of a strain, but we certainly are starting to see flight data, obviously, in China has gone down significantly,” she said. “Mobility data across all three regions—the U.S., Europe and Asia—is showing lower at this point in time, so I do think those two competing factors are what is holding pricing more in place and more in check than you’re seeing, obviously, in the European gas market.”

Recommended Reading

Oil Dips as Demand Outlook Remains Uncertain

2024-02-20 - Oil prices fell on Feb. 20 with an uncertain outlook for global demand knocking value off crude futures contracts.

Imperial Expects TMX to Tighten Differentials, Raise Heavy Crude Prices

2024-02-06 - Imperial Oil expects the completion of the Trans Mountain Pipeline expansion to tighten WCS and WTI light and heavy oil differentials and boost its access to more lucrative markets in 2024.

US Oil Stockpiles Surge as Prices Dip, Production Remains Elevated

2024-02-14 - EIA reported crude oil stocks increased by 12.8 MMbbl as February began, far outstripping expectations.

US Gulf Coast Heavy Crude Oil Prices Firm as Supplies Tighten

2024-04-10 - Pushing up heavy crude prices are falling oil exports from Mexico, the potential for resumption of sanctions on Venezuelan crude, the imminent startup of a Canadian pipeline and continued output cuts by OPEC+.

Oil Rises After OPEC+ Extends Output Cuts

2024-03-04 - Rising geopolitical tensions due to the Israel-Hamas conflict and Houthi attacks on Red Sea shipping have supported oil prices in 2024, although concern about economic growth has weighed.