An IMR vessel offshore Bulgaria. (Source: Shutterstock)

The subsea services market – with its flow assurance services, ROV drill support and inspection, maintenance and repair (IMR) – is set to top $7 billion in spending this year. That represents more than a 20% increase compared to last year, driven largely by increased brownfield activity in the Americas and Europe.

A major indicator of the health of the subsea market is subsea tree award and installation activity, as well as tracking the health of trees over their lifetime for key takeaways. A subsea production system (SPS) contains the most failure-sensitive equipment installed underwater and is subject to preventive maintenance through the replacement of control modules. Inspection is critical to monitor the state of the equipment, with most IMR work falling under this category. The major expenditure occurs, however, when repair is needed, even though repair accounts for a relatively small portion of activity.

The subsea umbilical, riser and flowline (SURF) market is the largest subsea market and is naturally subject to IMR needs. Risers and free-hanging umbilicals are subject to extreme dynamic loads and are frequently checked for integrity, both through annulus monitoring from the topsides and visually through the use of ROVs, AUVs or divers. Flowlines and rigid trunklines are placed in static environments. Inspection pigs, ROVs or AUVs inspect the lines because the unprocessed well stream can make pipes more prone to corrosion. As such, pipelines require routine assessment for flow assurance issues, such as waxing. Inspection typically makes up between 70% and 90% of IMR activity for pipelines.

Subsea equipment usually follows a bathtub curve for the likelihood of IMR activities: During the first years, it is crucial to monitor for any initial failure; the middle years are characterized by steady operations; and more regular inspection is required as equipment nears the end of its design life, usually 20 to 30 years. Although it is not a given that age increases IMR intensity, equipment age could be a good indicator of market demand for surveying the integrity of old subsea equipment.

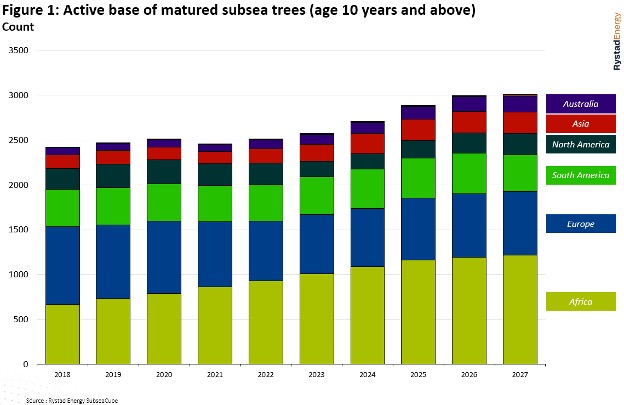

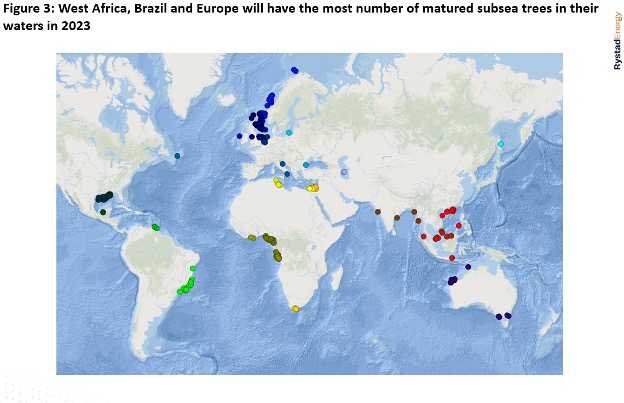

Angola and Nigeria saw a wave of subsea tree installations at the beginning of the previous decade that will pass the 10-year mark in the coming years, potentially increasing the regional demand for IMR services. Africa will have around 1,200 matured (aged 10 years or older) subsea trees in 2027, a 20% increase from what the region will have this year, and the continent will account for around 40% of such matured trees operating globally in 2027. Europe will also be a hot spot for the subsea IMR market as the region holds a quarter of all matured subsea trees operating this year.

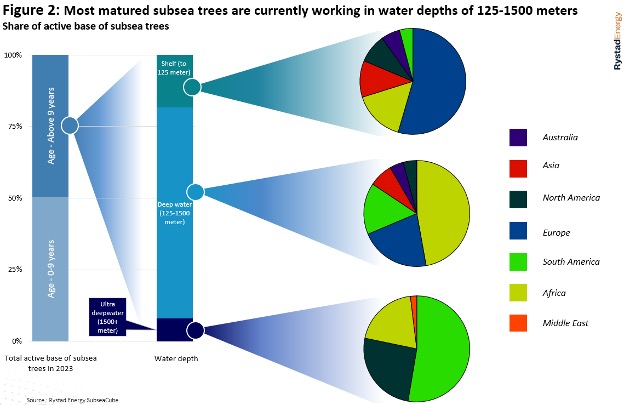

Looking at the water depth at which these matured subsea trees are currently functioning, almost 74% of them are in water depths between 125 m and 1,500 m. 47% of trees in that range of water depth are in Angola and Nigeria, currently operational at projects such as Dalia, Pazflor, Girassol and Bonga. Estimated expenditure on subsea services in Africa is expected to remain at over $800 million per annum in the coming years, having stayed between $500 million to $600 million per annum for the last six to seven years.

In Europe, almost 60% of currently operational matured subsea trees are in water depths of 125 m to 1,500 m, notably at projects such as Troll Oil, Aasgard and Gullfaks South, all of which are in Norway. The remainder of mature subsea trees are currently active in projects located in water depths of 125 m or less.

Brazil is expected to have the most matured trees in water depths exceeding 1,500 m, with its Roncador project that started production in 1999, and Tupi, where the project’s first field came online in 2009.

The global subsea service market has seen around $5 billion spent annually on average over the last five years, which we expect could increase to just over $7 billion a year in the coming five years. Looking at the subsea services expenditures for ROV drill support, IMR services, flow assurance services and others, Europe could see above $7 billion of expenditure in the coming five years, including IMR services and ROV drill support driven by new developments in the pipeline in the region. This will be followed by North America and South America, which together could see over $10 billion of expenditure, also driven by a range of subsea services as new developments are under way. Africa, meanwhile, could see just above $5 billion in that period, but we expect most of it will be for IMR services.

Abhinav Parashar is a senior analyst for energy service research at Rystad Energy.

Recommended Reading

Novo II Reloads, Aims for Delaware Deals After $1.5B Exit Last Year

2024-04-24 - After Novo I sold its Delaware Basin position for $1.5 billion last year, Novo Oil & Gas II is reloading with EnCap backing and aiming for more Delaware deals.

EIA: Permian, Bakken Associated Gas Growth Pressures NatGas Producers

2024-04-18 - Near-record associated gas volumes from U.S. oil basins continue to put pressure on dry gas producers, which are curtailing output and cutting rigs.

Benchmark Closes Anadarko Deal, Hunts for More M&A

2024-04-17 - Benchmark Energy II closed a $145 million acquisition of western Anadarko Basin assets—and the company is hunting for more low-decline, mature assets to acquire.

‘Monster’ Gas: Aethon’s 16,000-foot Dive in Haynesville West

2024-04-09 - Aethon Energy’s COO described challenges in the far western Haynesville stepout, while other operators opened their books on the latest in the legacy Haynesville at Hart Energy’s DUG GAS+ Conference and Expo in Shreveport, Louisiana.