Has Enterprise Products Partners reached the final frontier of EBITDA achievement? Given how its motivated workforce performed in 2022, that trek is far from over.

The company’s Project 9 was meant to increase operations efficiencies to push company EBITDA beyond $9 billion for the year. Among the successes: increasing methyl tertiary butyl ether production and increasing fractionation throughput at Mont Belvieu, Texas.

The Star Trek-themed program –“Boldly go where Enterprise has never gone before” –promised $3,000 bonuses for each employee if the company recorded $9 billion in EBITDA for the year. If the total crossed $9.3 billion, the employees would receive $5,000. It did and they did.

“We had so much fun with this,” said co-CEO of Enterprise Jim Teague during the company’s recent earnings call with analysts. “We decided we are going to have Project 9.3 for 2023.”

But don’t take it for guidance, he quickly told analysts on the line.

Strong earnings and bright outlooks were the theme for three midstream companies recently reporting fourth-quarter and full-year 2022 earnings.

Enterprise Products Partners

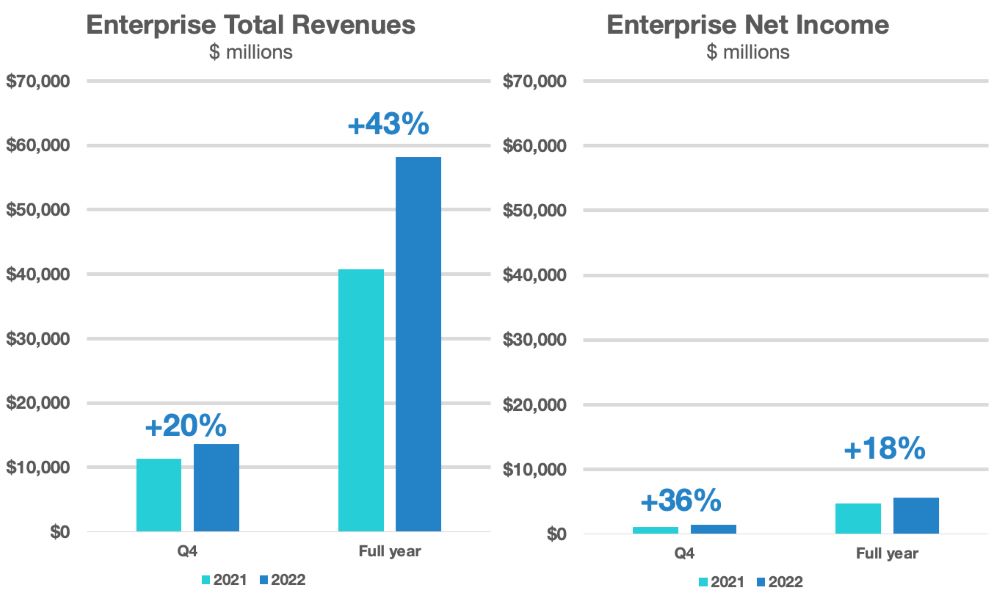

Enterprise reported net income of $1.45 billion on revenues of $13.65 billion for the quarter, and net income of $5.49 billion on revenues of $58.19 billion for the year. Earnings per common unit rose 38.3% to 65 cents for the quarter compared to 47 cents in fourth-quarter 2021. For the full year, earnings per unit were $2.50, a 19% increase over full-year 2021.

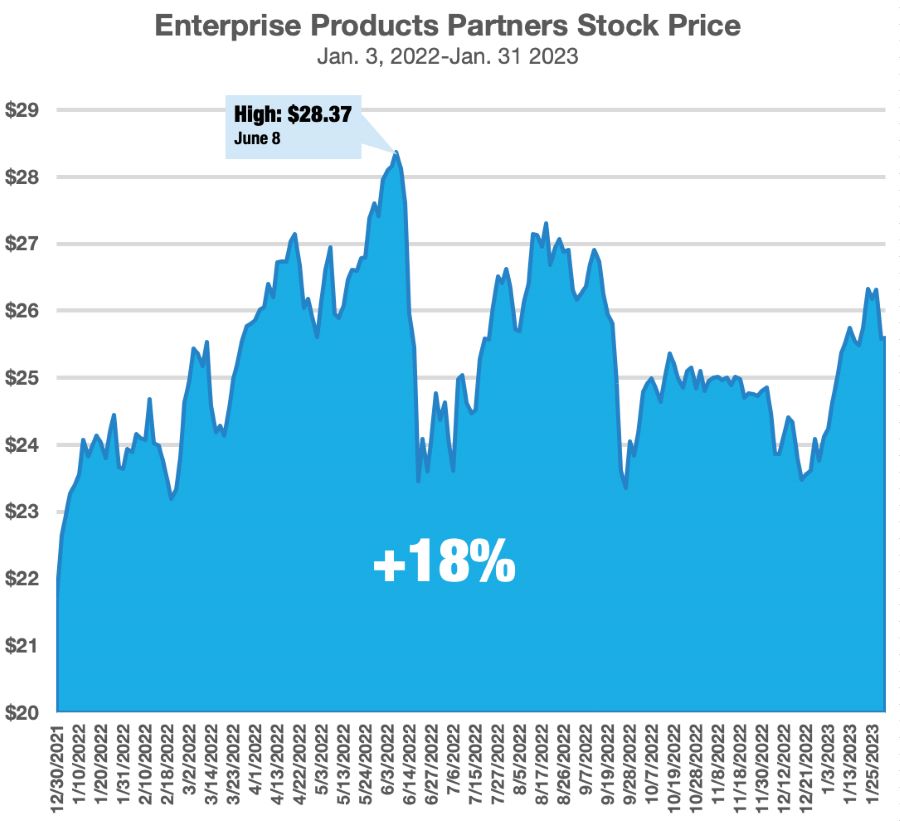

Enterprise’s stock hovered around $26 in the past week, or about 10.3x earnings per unit. That price is well below analysts’ consensus price target of $31. 18 of 21 brokerages that cover the stock give it a ‘Buy’ or ‘Strong Buy’ rating.

Quarterly distributed cash flow increased 22.2% year-over-year to $2.03 billion, and 17.3% to $7.8 billion for the full year.

Teague noted record volumes across several of the company’s assets, as well as contributions from its purchase of Navitas Midstream in February 2022.

“This acquisition was immediately accretive to Enterprise’s cash flow per unit and has exceeded our expectations,” he said.

During the fourth quarter, the company purchased about 580 miles of pipeline and related assets on the Texas Gulf Coast to expand its NGL and petrochemical pipeline systems in the region. More acquisitions are possible as well.

“We are interested in asset acquisition opportunities that make sense, that can come in and bolt on to our system and get good returns on capital,” co-CEO Randy Fowler told analysts. “And that’s where the lower leverage gives us flexibility to … do these cash transactions. I think over the last… 18 months we’ve sort of completed that pivot to go from an externally-funded model to an internally-funded model.”

By segment:

- NGL pipelines and services reported gross operating margin of $1.3 billion in the fourth quarter, up 17% year-over-year;

- Crude oil pipelines and services saw a 4.6% drop year-over-year to $418 million, with West Texas Pipeline System up $31 million and Seaway Pipeline up $18 million;

- Natural gas pipelines and services margin jumped 61% year-over-year to $315 million, setting a record of 17.6 trillion Btu, compared to 14.6 trillion Btu in fourth-quarter 2021; and

- Petrochemical and refined products services margin was flat at $339 million for the quarter, compared to $338 million in the same quarter of 2021.

Enterprise does not expect to return to the capital markets, Fowler said, and expects to mark 25 consecutive years of distribution growth in 2023.

Magellan Midstream Partners

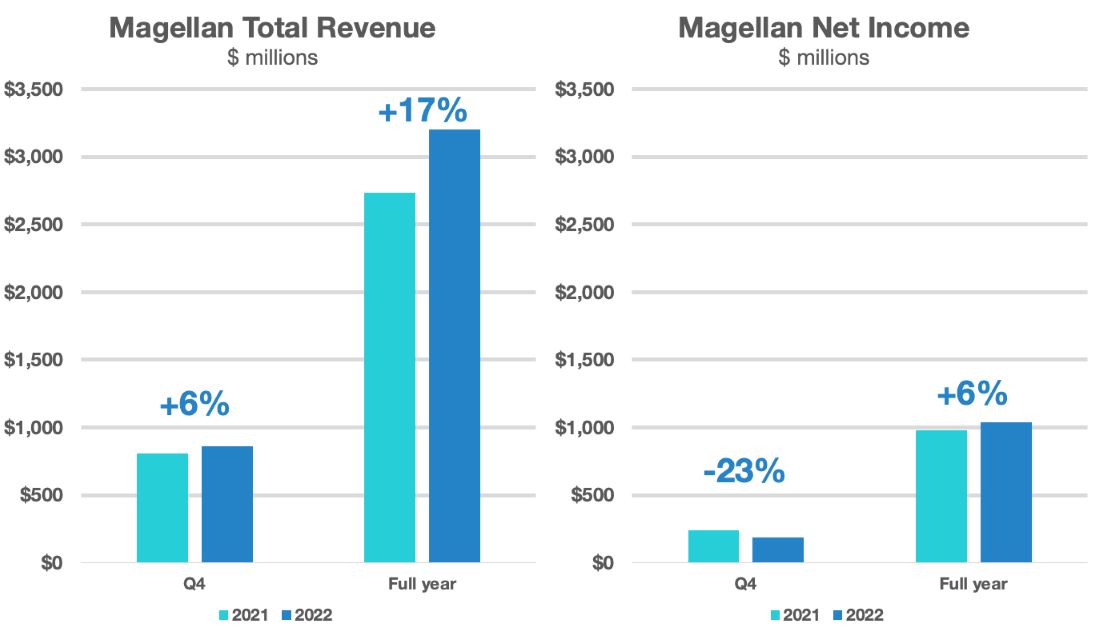

Higher-than-expected revenues from refined products transportation, as well as a higher commodity margin from additional blending volumes, buoyed net income for the company in the fourth quarter. Magellan reported net income of $187 million, affected by a non-cash charge of $58 million related to its investment in the Double Eagle pipeline.

Without that impairment, diluted net income per unit of $1.34 handily beat guidance of $1.22 issued last fall. The Double Eagle impairment involved non-renewal on terms of customer commitments expiring later in 2023 and reduced demand for condensate transport from the Eagle Ford basin. Diluted net income per unit for the full year was $4.47.

Total revenue was $861 million in the quarter, compared to $809 million in fourth-quarter 2021. Full-year revenue of $3.2 billion beat 2021 by 17%. Full-year net income was $1.04 billion, compared to $982 million in 2021.

Magellan’s crude oil shipments in the quarter rose 47.2% year-over-year to 65.2 MMbbl. For the full year, the company shipped 229.8 MMbbl, up 21.2% over the 189.6 MMbbl moved in 2021.

Quarterly crude oil operating margin increased 23.5% to $128.2 million year-over-year. For the full year, the margin was up 8.4% to $466.9 million. Higher average rates on the Longhorn pipeline, higher terminal fees and increased dock activity from customers using a simplified pricing structure in the Houston area pushed up transportation and terminals revenue by $9 million in the quarter.

Crude oil shipments are projected to rise in 2023 on company-owned pipelines. Magellan expects shippers on its joint-venture pipelines to not meet commitment levels and to make deficiency payments.

For 2023, Magellan expects to generate distributed cash flow of $1.18 billion. Free cash flow is projected to be $1.07 billion, or $216 million after distributions. This is based on an average crude price of $80/bbl for the year. The company estimates that each $10 change in the price of crude affects its financial results by about $35 million.

Hess Midstream

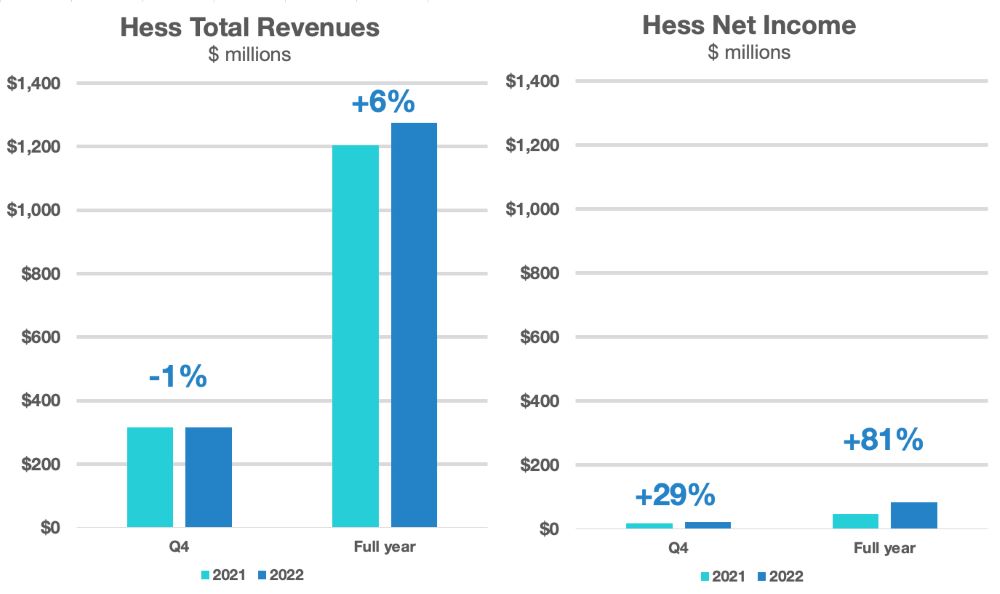

Quarterly net income was $149.8 million, with net income attributable to Hess Midstream of $21.8 million, up 29% from $16.9 million in the same quarter last year. Total revenue in the quarter was $314.6 million, essentially flat year-over-year, with full-year revenues of $1.275 billion exceeding 2021 revenues by 6%.

Gathering operations accounted for $166.1 million, or 52.8%, of revenues in the quarter. Processing and storage revenues totaled $118.8 million, and terminaling and export revenues were $29.7 million.

Throughput volumes for gas gathering dipped 4.9% year-over-year and 11.4% from the third quarter to 328 MMcf/d due to severe weather in the Bakken and Three Forks shale plays. Crude oil gather was off 12.3% in the quarter year-over-year, and 8.8% from the third quarter.

In its 2023 guidance, Hess Midstream projects full-year gas gathering volumes to average 365 MMcf/d to 375 MMcf/d. Gas processing is projected at 350 MMcf/d to 360 MMcf/d. Crude oil gathering is expected to average 95,000 bbl/d to 105,000 bbl/d, and crude oil terminaling is projected to average 105,000 bbl/d to 115,000 bbl/d.

Recommended Reading

Midstream Operators See Strong NGL Performance in Q4

2024-02-20 - Export demand drives a record fourth quarter as companies including Enterprise Products Partners, MPLX and Williams look to expand in the NGL market.

Post $7.1B Crestwood Deal, Energy Transfer ‘Ready to Roll’ on M&A—CEO

2024-02-15 - Energy Transfer co-CEO Tom Long said the company is continuing to evaluate deal opportunities following the acquisitions of Lotus and Crestwood Equity Partners in 2023.

Waha NatGas Prices Go Negative

2024-03-14 - An Enterprise Partners executive said conditions make for a strong LNG export market at an industry lunch on March 14.

Pembina Pipeline Enters Ethane-Supply Agreement, Slow Walks LNG Project

2024-02-26 - Canadian midstream company Pembina Pipeline also said it would hold off on new LNG terminal decision in a fourth quarter earnings call.

Targa Resources Forecasts Rising Profits on 2024 Exports

2024-02-20 - Midstream company Targa Resources reports a record fourth quarter in volumes and NGL fractionation.