(Source: Shutterstock)

[Editor's note: A version of this story appears in the March 2020 edition of Oil and Gas Investor. Subscribe to the magazine here.]

Despite an uptick late in the year, midstream oil and gas stocks endured a rough 2019 on Wall Street. The sector outperformed the E&P and oilfield service segments but was subdued by a general sense of investor disappointment with energy.

“I think that had a lot to do with the midstream sector spending too much money and frustration with that and people wanting them to dial things back,” said Pearce W. Hammond, managing director for midstream and infrastructure equity research at Simmons Energy in Houston.

This year should be better for the sector, Hammond said, because many in the midstream have listened and responded. Four companies in particular, selected by Hammond and Kyle May, equity research analyst for Capital One Securities, are primed for strong uplifts in part because of their approach to generating free cash flow.

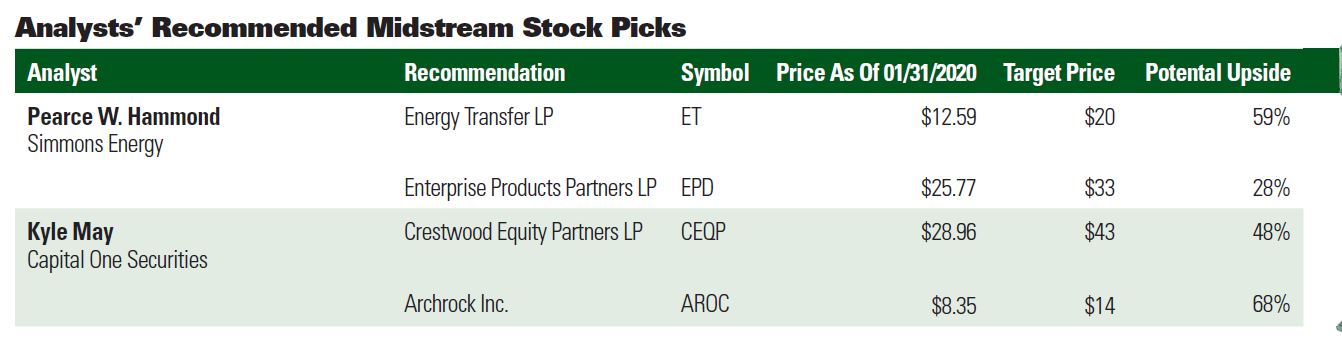

There’s a lot to like about the Dallas-based giant with a market capitalization of $33.8 billion as of Jan. 31. Hammond points out that Energy Transfer pays a dividend yield of about 9%, which will bolster investor return in addition to the expected jump in unit price.“Because the E&Ps are spending less money and production expectations are coming down, people want the midstream companies to spend less, and you see that with Energy Transfer [LP],” Hammond said. “They intend to spend less money in 2020 versus 2019, and then as you move forward it will be even less.”

Hammond sees the company as an attractive valuation relative to peers, noting that its units trade at about a 2x discount at enterprise value-to-EBITDA. He is also impressed that Energy Transfer operates a self-funding capital program. “They generate enough cash flow to cover their distribution and fully fund their capital program,” Hammond said. “There are a lot of midstream companies that actually can’t do that.”

Energy Transfer also boasts an integrated wellhead-to-water business model, which allows it to take an E&P’s molecules and liquids all the way from the lease to the water for export. That’s a one-stop shop for gathering, processing, shipping via pipeline, fractionating and exporting—essentially whatever the producer needs.

Hammond also favors the company’s restrained approach to capital spending in the less-is-more era.

“They’re guiding to growth capital spending this year of $3.6 billion to $3.8 billion, and that compares to $4 billion in 2019,” Hammond said. “After this year, they only have—right now—$1.5 billion worth of projects that are approved. I think that number will go up, but not to the level that would support spending $3.6 billion to $3.8 billion a year. I think the capital spending’s going to fall in the next few years, and that will result in a lot more free cash flow, which is positive for investors.”

‘Management will be prudent’

Capital One’s midstream coverage focuses on specialized mid-caps and small caps, which offer investors plenty of upside potential, among them one of his choices: Crestwood Equity Partners LP. (Editor’s note: Capital One Securities has received compensation for investment banking services from and managed or co-managed a public offering of securities for an affiliate of Crestwood Equity Partners LP within the past 12 months.)

In January, Crestwood, with a market capitalization of $2.08 billion as of Jan. 31, introduced a long-term distribution policy that bases future distributions on free-cash-flow generation.

“To me, that’s definitely a positive sign,” May said. “It signals that the company is aware of what investors are looking for, their desire to see that return of capital, but also that management will be prudent in how they’re going to return capital.”

More than that, May said that Crestwood is signaling to the market that it wants to break the cycle of increasing quarterly distributions by a small amount, common among many midstream companies in the past. “This is more of a ‘we’re going to step things up and, based on our annual outlook going forward, we’ll continue to increase the distribution, but we also want to be mindful of what our free cash flow is and be able to operate within our means,’” he said.

Crestwood operates in the Bakken Shale, the Powder River Basin and the Permian Basin, and it has pumped most of its investment in recent years into those core areas. While challenges abound in U.S. unconventional plays, the Bakken rig count has held steady, May said. The Powder continues to fight for capital. Rig activity in the Permian continues to outpace other areas of the U.S., and operators who have the ability are moving rigs to the Permian from other basins. May expects these areas to continue to drive growth for Crestwood.

In 2020, Crestwood expects to improve its leverage ratio below 4x. The coverage ratio will be around 2x. “The way that our model and our projections shake out, plus with the goal posts that they provided … I think you’ll see their EBITDA increase 15% year-over-year,” May said, adding that he expects continued growth in 2021.

One cause for investor hesitation with Crestwood is related to guidance from a producer, Chesapeake Energy Corp., which announced in late 2019 that it would cut its rigs in the Powder River Basin from four to two.

“I know Crestwood got a lot of pressure from that at the time, but I’ve spoken with the company. Crestwood was already aware of this when they put out their initial guidance for 2020 so the stock maybe got hit a little bit harder than it should have at the time,” May said. Balancing that news are plans by operator Panther Energy Co. LLC to add well connects in 2020. May said he also expects Crestwood to garner commercial agreements with other third parties, but he acknowledged that the Powder River is less of a known quantity with investors.

Top tier assets

The unit price of Enterprise Products Partners LP enjoyed a strong run from December through mid-January, so its potential upside is not as strong as other picks, but the midstream giant (market capitalization of $56.7 billion at the end of January) inspires enthusiasm from Hammond.

“This is definitely a sleep-well-at-night midstream company,” he said.

The No. 1 reason to favor Enterprise is the same reason Hammond likes Energy Transfer—an integrated wellhead-to-water asset base. He also points to a long track record of successful operational execution, a solid management team and strong inside ownership.

“And their assets are top tier,” Hammond said. “They’ve got the largest position at Mont Belvieu, [Texas], and the fractionators there which is kind of an irreplaceable asset. You can’t recreate that asset. They’re the largest exporter of crude oil out of the United States. They’re the largest exporter of LPG.” Enterprise’s debt ratio is around 3.6x for 2020, well below peers, he said. By comparison, the other midstream large caps are at about 4.5x.

He is also intrigued by Enterprise’s partnership with Enbridge Inc., announced in December, to develop the Sea Port Oil Terminal 30 nautical miles off the coast of Brazoria County, Texas. The facility would be able to handle very large crude carriers and load as much as 2 million barrels per day.

Relying on output

May’s optimism about natural gas compression provider Archrock Inc. derives from the U.S. Energy Information Administration (EIA) production outlook. In 2019, the U.S. set a record with average output of 92 billion cubic feet per day (Bcf/d). The EIA expects 2020 output to rise to 94.7 Bcf/d before slipping to 94.1 Bcf/d in 2021.

Archrock’s reduction in growth capex dovetails with the easing of natural gas production growth. Growth capex for the company, with a market capitalization of $1.27 billion, is expected to drop from the range of $285 million to $300 million in 2019 to under $125 million in 2020, or likely more than 55% year-over-year. That’s exactly what the analysts say investors want to hear.

“Based on that, they’ll be able to leverage their existing fleet of large-horsepower equipment and that will lead to free cash flow generation, as you have EBITDA uplift and capex declining,” said May, who expects the company to achieve many of its financial milestones. “They’ll begin generating free cash flow this year. They’re going to improve their leverage ratio below 4x, and their distribution coverage should be above 2x this year as the company increases their dividend.”

Archrock’s success will depend to a large extent on operators’ budgets and plans for 2020, May said. Still, if the EIA forecast points in the right direction, natural gas production will increase, and that should bode well for Archrock. “If you see some headwinds where production falls off more quickly than they’re expecting, then that would definitely be a headwind for the company,” May said.

What could go wrong?

The headwinds these companies will face reflect challenges the midstream sector as a whole will endure in coming months. Hammond’s top concern is the falling rig count, a sign that future volumes will be lower than had been expected. Also worrisome: declining well production rates. An IHS Markit analysis showed that Permian Basin oil output would have tumbled 40% in 2019 had it not been for wells that began production in that year.

The industry’s strategy of relying on exports to compensate for flat oil and gas demand in the U.S. may need revising if production comes up short. It also buttresses the arguments of investors who want to rein in spending, which conflict with proposals by management teams hungry for new opportunities.

“That’s the tension, the tug-of-war between those two,” Hammond said. “The management team is saying, ‘Hey, we got great projects that are being driven by high-quality producers,’ and you have investors saying, ‘yeah, but the energy business is slowing way down. You don’t need to spend so much money to grow.’”

Enterprise, a main driver of exports, is a prime example.

“The expectation a lot of people had, even just a year ago, was that the U.S. was going to grow oil production by about 1 million barrels per day per year … which is what global demand grows at,” he said. “But that’s not the case anymore; it’s probably half that number. So you have to argue that maybe we don’t need as many export facilities as we thought we did.”

May agrees that the pressure on upstream companies to slow their rates of growth will lead to slower volume growth for midstream companies, but he sees an upside to that as well. “There’s going to be less volume growth coming to midstream companies, but in turn, less capex will be required than in recent years when U.S. production was rapidly growing. So, we should see a significant drop in midstream spending this year,” he said.

Aside from volumes, the sector has been grappling with stubbornly low prices for natural gas, with the U.S. benchmark Henry Hub sinking to 12-month lows below $2 per million Btu in late January. Much of that can be attributed to the absence of sustained cold weather across the country this winter and has contributed to financial woes experienced by gas producers.

Other issues from outside the industry can have an impact. Hammond cited the prospect of the Federal Reserve raising interest rates this year. It’s always a possibility, though not a certainty. “The midstream are primarily yield vehicles,” he said. “They pay big distributions or dividends, but they compete with fixed income instruments for investor dollars, so if interest rates were to move higher—they’re pretty low right now—but if they were to move higher, then that could be a headwind.”

And then there’s the wild card: the 2020 U.S. presidential election. “If the Democrats nominate somebody who is pretty far left of center and that person wins, it may not be very favorable for energy at all,” Hammond said. A week prior to the Iowa caucus, Sen. Bernie Sanders, D-Vt., a Democratic Socialist, was leading in the polls in that state, with Sen. Elizabeth Warren, D-Mass., another presidential candidate promising economic upheaval, near the top. Those two were the first choice of 40% of likely voters in a New York Times/Sienna College poll. Moderate Democratic candidates Mayor Pete Buttigieg, former Vice President Joe Biden and Sen. Amy Klobuchar, D-Minn., together accounted for 43%.

What could go right?

The industry has its share of tailwinds, though, including a January report by IHS Markit in which 67% of institutional and private-equity investors with a total of $98 billion in energy assets under management believe there is potential for the industry to enjoy a cyclical rebound in the stock market and lure back equity investors. And 63% of those surveyed view the oil and gas sector as undervalued.

Hammond believes the oil and gas industry as a whole is positioned for a strong transitional year that will result in a much more positive market. He expects much of the shift to take place in the second half of 2020 and carry into 2021 as the positive effect of the combination of lower rig counts, capital discipline from E&Ps, and slower U.S. production growth results in tighter commodity market balances. But improvement with oil supply fundamentals is only part of it. Hammond also points to companies following the lead of those listed here and adopting capital allocation reform strategies, which translate into lower spending. “It’s starting to take hold,” he said. “It needs more time, but it is taking hold.”

The midstream sector is poised for an increase in M&A activity, he said, as well as a continued wave of conversions from MLPs to C corps. And if companies drag their feet in moving forward, count on angry activist investors to express their dismay. “If equity prices had stayed where they were in November, I think you could see some activists come in,” he said.

In this positive outlook for the year, midstream stocks will benefit, though they may be outperformed by other segments.

“If you’re an energy investor, you’re probably going to want to buy the E&Ps and oilfield service sector and, given some of the challenges in oilfield services, you probably would buy E&P first and then oilfield services second,” Hammond said. “I would think in that environment they would probably outperform the midstream sector because the midstream sector is a bit more stable, conservative and, in an upward moving commodity price environment, the higher beta stuff is going to move.”

Recommended Reading

BP: Gimi FLNG Vessel Arrival Marks GTA Project Milestone

2024-02-15 - The BP-operated Greater Tortue Ahmeyim project on the Mauritania and Senegal maritime border is expected to produce 2.3 million tonnes per annum during it’s initial phase.

Sangomar FPSO Arrives Offshore Senegal

2024-02-13 - Woodside’s Sangomar Field on track to start production in mid-2024.

Proven Volumes at Aramco’s Jafurah Field Jump on New Booking Approach

2024-02-27 - Aramco’s addition of 15 Tcf of gas and 2 Bbbl of condensate brings Jafurah’s proven reserves up to 229 Tcf of gas and 75 Bbbl of condensate.

Sinopec Brings West Sichuan Gas Field Onstream

2024-03-14 - The 100 Bcm sour gas onshore field, West Sichuan Gas Field, is expected to produce 2 Bcm per year.

TotalEnergies Restarts Gas Production at Tyra Hub in Danish North Sea

2024-03-22 - TotalEnergies said the Tyra hub will produce 5.7 MMcm of gas and 22,000 bbl/d of condensate.