A LNG vessel and tugboats seen near the port of Gladstone, Australia. (Source: Shutterstock.com)

Europe’s energy crisis in 2022 was arguably softened by U.S. LNG exports, but a reliance on U.S. gas supply comes with its own risks, Shell highlighted in its LNG Outlook 2023.

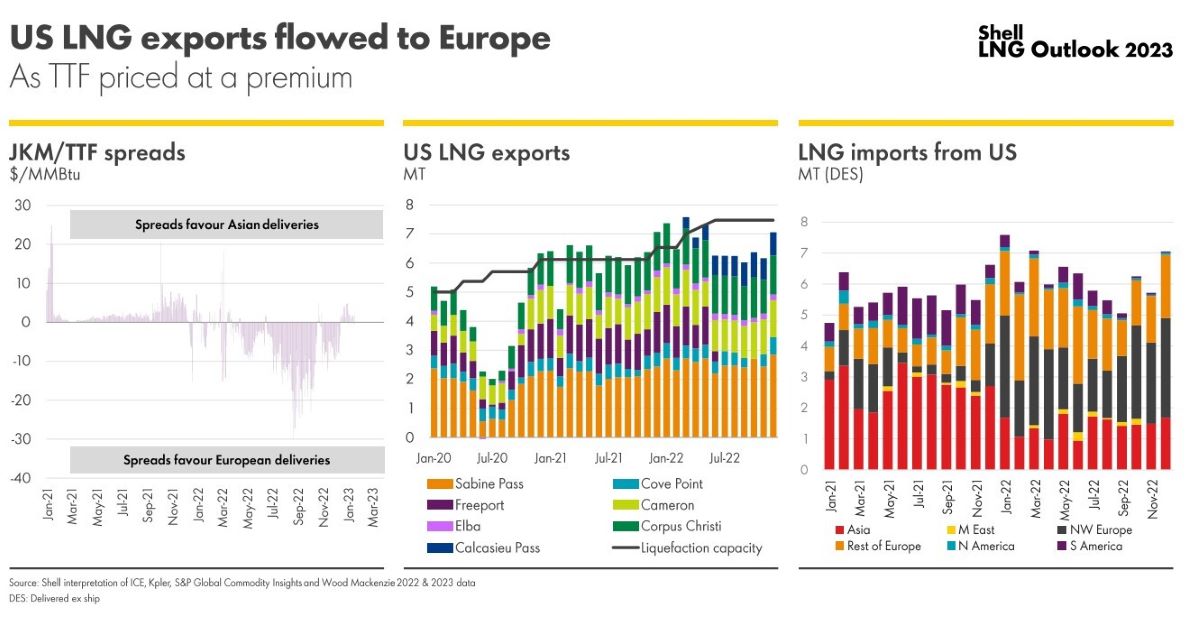

In 2022, European LNG imports rose by 60% to replace Russian gas thanks to higher U.S. LNG imports as well as increased imports of LNG originally destined for Asian markets, Shell said in the yearly report on the LNG sector in February.

Robust gas production from the Permian Basin and other U.S. shale plays has anchored rising U.S. LNG exports. A slew of new liquefaction capacity additions in coming years will only boost U.S. LNG supplies.

But this rising role for U.S. supply in the global LNG market increases the exposure to U.S. gas market risks, Shell said.

Shell said principal risks relate to forecasts for U.S. LNG to account for nearly 20% of total U.S. gas production by 2028 compared to about 10% now; a concentration in Texas and Louisiana of over 95% of U.S.’ LNG capacity by 2030; and higher U.S. gas demand by 2028 driven by the LNG and industrial sectors.

More LNG investment needed

Russia’s invasion of Ukraine in February 2022 led to a reduction of Russian piped gas exports to Europe and forced the region to turn to LNG, pushing up prices for cargoes. Europe was aided by the import of more LNG cargoes from the U.S. and other suppliers. Those cargoes were originally intended for Asia but diverted owing to lower gas demand in China due to its zero-COVID restrictions as well lower demand in South Asia due to high prices.

LNG will remain a key energy source in coming years amid the energy transition, and Europe and China will likely contend for limited LNG cargoes until more liquefaction capacity comes online in the U.S. and Qatar, Shell said Feb. 16 in a separate press release. LNG demand is forecast to span from 650 million tonnes per annum (mtpa) to over 700 mtpa by 2040. Total global LNG trade was 397 mtpa in 2022.

“More investment in liquefaction projects is required to avoid a supply-demand gap that is expected to emerge by the late 2020s,” the European major said.

Shell’s executive vice president for energy marketing Steve Hill said the Ukraine war has caused shifts in the market likely to impact the LNG sector over the long-term.

“It has also underscored the need for a more strategic approach – through longer-term contracts – to secure reliable supply to avoid exposure to price spikes,” Hill said.

While the term LNG contracts will help reduce exposure to price volatility, Europe and major Asian economies China and Japan have different approaches.

By 2030, Europe is forecast to have less than 20% of its LNG demand under term contract compared to around 30% in 2022. In comparison, China and Japan is forecast to have on average around 80% by 2030 compared to around 100% in 2022.

Recommended Reading

SAF End-users, Producers Talk Challenges, Solutions

2024-02-07 - The lower lifecycle emissions of sustainable aviation fuel are seen as a key lever for airlines to reduce carbon emissions, but cost is a challenge.

CAPP Forecasts $40.6B in Canadian Upstream Capex in 2024

2024-02-27 - The number is slightly over the estimated 2023 capex spend; CAPP cites uncertain emissions policy as a factor in investment decisions.

Air Liquide to Add CO2 Recycling at Plant in Germany

2024-02-08 - In a supply agreement, Air Liquide and Dow plan to add a new CO2 recycling solution to two air separation units and one partial oxidation plant.

1 Fatality in Equinor Helicopter Training Accident Offshore Norway

2024-02-29 - Equinor employee died following the helicopter accident, the cause of which has not been reported.

Equinor Resumes Helicopter Flights on NCS Following Fatal Accident

2024-03-01 - Operator also announced it is expanding its helicopter fleet by 15 through contracts with Bell and Leonardo, with the first two helicopters slated for delivery in about a year.