(Illustration by Robert D. Avila)

[Editor's note: A version of this story appears in the September 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

The bright side of first-half 2019 A&D activity is that it’s difficult to see how it could get worse any time soon.

First-quarter transactions “screeched to a halt” in the first quarter, with the lowest quarterly deal value recorded in a decade, according to Raymond James’ analysis. A bounce back in deal values in the second quarter rested heavily on the shoulders of Occidental Petroleum Corp.’s merger with Anadarko Petroleum Corp. in a deal valued between $57 billion and $64 billion.

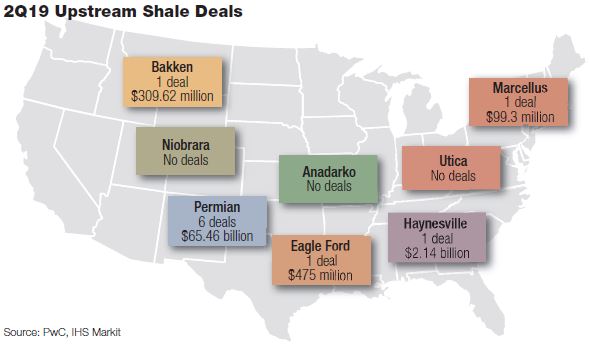

Around the edges of the supernova merger burned a pale corona of asset deals. In the Bakken, Permian, Eagle Ford, Marcellus and Haynesville, PwC counted just nine upstream shale deals in second-quarter 2019.

RELATED:

US E&P A&D Deal List (First-Half 2019)

In a July report, PwC said a new reality is settling over contemporary oil production.

“Investors and lenders are no longer writing checks to companies that can’t show positive cash flow. Eager to black ink, corporate dealmakers are looking to drive scale efficiencies.”

Any lingering doubts about an off-kilter start to 2019 have been confirmed by numbers indicating the sector is sailing in shallow waters. The asset-level A&D environment is soft, though it still has epicenters of relatively strong or at least functional markets, said Art Krasny, managing director at Wells Fargo Securities.

As of late July, A&D asset transactions totaled roughly $13 billion. At its current pace, A&D values in 2019 may eventually tick up to perhaps $25 billion for the year, plus or minus $5 billion—at least a 30% decline compared to 2018, he said.

“That’s a shadow of a market that was already pretty weak back in 2017 and 2018” when deals were about $40 billion, he said. “It’s been a market that’s seen a tremendous compression of activity, of volumes, of downward pressure on valuations.”

In the current market, mineral and royalty deals are gaining strength, private-equity firms are contemplating mergers and some buyers are looking for safe and less costly conventional assets.

Meagher Energy Advisors has seen success with low-decline, conventional asset deals, said Matthew E. Meagher, president and partner of the firm.

Partly, the turn back toward conventional assets comes at a time when public and private financing remains not just closed off but indifferent to upstream companies.

“I just don’t know if buyers really have the capital to develop unconventional, horizontal-type assets,” Meagher said.

Buyers, typically backed by private-equity funds, may be making investment in conventional assets while they wait for better pricing and better times.

“A lot of people are just looking for conventional—its cash flow,” he said.

In the first half of the year, bright spots have been fleeting, though electrifying. Comstock Resources Inc. closed on a cash and stock acquisition of Haynesville operator Covey Park Energy LLC in a $2.2 billion merger.

Apache Corp. sold off its Oklahoma positions in the western Anadarko Basin and Scoop and Stack plays to two private-equity-backed E&Ps for more than $600 million. And on July 29, Osaka Gas Co. Ltd. agreed to buy Houston-based independent Sabine Oil & Gas Holdings Inc., which Osaka said would make it the first Japanese firm to purchase a U.S.-based shale company. Sabine’s East Texas operations sold for about $700 million and followed Osaka taking a 35% position in the company last year for about $145 million.

But A&D value in the second quarter largely rode the coattails of Occidental’s massive deal with Anadarko. Of the $68.2 billion in second-quarter deals tallied by PwC in its July report, just 6% of the total was from other deals.

Dwindling interest by investors appears to have dampened enthusiasm among companies that would typically make transactions.

“On the psychological side, there is a great deal of pessimism out there,” Meagher said. “So, a lot of people, they’re not doing anything. They’re not buying. They’re not selling. They’ve just stopped their activity.”

Meagher said he’s not sure the reticence in the deal market is necessarily associated with oil prices.

“It’s just more of an attitude, and we’ve been here before, where you think the rug is moving out from underneath you, and you just want to stop.”

Forsaken

For the past few years, Wall Street has put public companies on a starvation diet, cutting back on capital and punishing companies that engage in A&D activity.

All but the most financially healthy E&Ps are able to make deals, though companies such as Occidental still face pushback from activist investors such as Carl Icahn.

The continuing drain of capital has started to affect private-equity-backed companies, which are blocked from the exits they would prefer—IPOs or buyouts.

Private-equity firms appear to have only recently recognized that the market is here to stay, Krasny said. In a new twist, those firms are considering their own mergers among their portfolio of companies.

As little as nine months ago, private equity was willing to wait until a window in the market opened up.

“A lot of the companies on the private-equity side were making plans to go through the market at that time,” he said.

While market conditions improved in 2018, the fourth-quarter collapse of crude oil prices created “a complete meltdown, and a lot of packages that were in the market were withdrawn,” he said.

The reaction was a swift change in private-equity firms’ behavior. Firms are no longer waiting for the market to change but instead are lining up potential mergers in their portfolios.

“That’s a fairly new phenomenon,” Krasny said. “We’re beginning to see the first signs of companies exploring those types of moves. We’ve started seeing overtures to try to do consolidation between portfolio companies of different private-equity firms.”

The steady drain of capital has also dulled the appetites of would-be buyers.

Meagher said less capital has pared back the number of offers made for assets and undeveloped acreage. However, quality assets still attract buyers with capital.

“Many of these buyers are family businesses, not private equity,” he said. “But [there are] definitely fewer players.”

Public companies continue to be victims not just of commodity prices beyond their control but of their own success. The industry has been ingenious in solving the equations needed to produce more oil for less money. But it’s been hammered by subtraction as fewer energy stocks are in investors’ portfolios, Krasny said.

The strength of U.S. producers has re-fashioned the oil and gas space as a lackluster and unexciting place to put money. E&P stocks are “no longer a must-have,” Krasny said.

E&Ps have also consistently lost capital, Krasny said.

The confluence of those and other factors is also reflected in a cracked mirror view of the industry as ultra-resilient, in part because U.S. companies weathered the downturn. The result is that even major world events that would have caused spikes in oil prices in the past now barely cause oil prices to flicker. Rising tensions between the U.S. and Iran and continued hostility in the Strait of Hormuz have done little to affect oil prices.

“We changed the dynamic of the global market where the market has stopped responding to the geopolitical signals the way it was responding previously,” Krasny said. “If you are an investor looking to invest in the commodity upside, their thesis has been muted by this dynamic.”

‘Shale 3.0’

One emerging thesis is that E&Ps are further transitioning, just as they metamorphized to their current state—Shale 2.0—by abandoning growth at all costs for restraint.

The current focus on drilling within cash flow and returning capital to investors may give way to what Krasny calls Shale 3.0.

In this stage, the industry will begin to self-regulate, managing production in response to commodity prices while also attempting to govern the supply of the commodity itself.

A&D and M&A are also working along different paths. While A&D rides on the current of the market, M&A is seen as an engine to build scale and efficiencies. In this realm, commodity type follows at a distance second.

“Scale matters,” Krasny said. “When you look at different attributes and try to understand what drives [company] performance and underpins it,” the difference is in the depth and breadth of operations and assets.

Companies with larger and more diverse portfolios and more mature portfolios are able to deliver on the Shale 2.0 promise of staying within cash flow and returning cash to investors—while also growing a cost-effective business.

The move toward Shale 3.0 is reflected in oil majors and large independents that are focused on securing running room in the Lower 48.

“We’ve seen that playing out already with companies like Exxon for instance making sure it has significant runway in the Permian Basin,” Krasny said. “With some of the consolidation on the corporate side we’ve seen in the Permian to date, that’s going to continue to crack the landscape.”

Large E&Ps want to acquire needle-moving targets. “In that class, deals like Occidental Petroleum and Anadarko Petroleum come to mind. And there are a few other companies that can make those moves,” he said.

Middle and smaller companies, at the same time, are already under pressure to consolidate.

Carrizo Oil & Gas Inc., for example, came under pressure in May from investor Lion Point Master LP, which acquired a 5.1% stake in the company. Lion Point saw Carrizo as an undervalued investment opportunity and advocated a merger or sales to increase its value.

On July 15, Callon Petroleum Co. said it would acquire Carrizo in an all-stock deal worth $3.2 billion. The deal builds scale for Callon, which will add Eagle Ford Shale acreage to its current Permian-focused company. Pro-forma production will average about 100,000 barrels of oil equivalent per day.

Carrizo’s asset base will add about 76,500 net acres in the Eagle Ford and 46,000 net acres in the Delaware Basin.

Chesapeake Energy Corp.’s $4 billion purchase in February of oil-weighted WildHorse Resource Development Corp. highlights the market’s interest in scale and diversity that will drive consolidation, Krasny said.

“Small and mid-sized companies desperately need to consolidate, because [they’re] struggling for relevance and struggling for investor attention. To break through, the only way to do it is to consolidate.”

The M&A market is not the A&D market, which ebbs and flows with the broader market. M&A is more fact-pattern specific.

“But that pressure will continue to persist, and we’ll continue to see those types of transactions,” he said.

Private-equity firms find themselves in similar limbo with IPO exits largely off the table in the current market and public companies unable to cash in on a weak seller’s market.

The private-equity world is coming to the same realizations as public companies.

Unable to find suitably rewarding deals or market exits, private-equity ventures are extending their holding times but can only hold out so long as pressure builds to pay investors.

“That drives stronger cost structure and more effective capital deployment and, in many cases, basic survival,” he said. “The pressure to consolidate is on.”

Holding Pattern

In a clouded market, transaction advisers say they are staying remarkably busy.

“We are slightly down from years prior, but not that far,” Meagher said. “We’re pretty selective on the engagements we take.”

The firm’s due diligence—and frank conversations with sellers about their value expectations—have allowed Meagher to close about 90% of the packages it’s offered.

“Basically, everything we’ve had on the market has sold,” he said.

In part, ground lost in upstream deals has been made up through a rise in mineral and royalty transactions. Meagher said such transactions have mushroomed to roughly a third of the company’s business—a far larger percentage than in past years.

“We’ve always done minerals and royalties. That’s just part of the game,” Meagher said. “But I would say this is probably double what we’ve done in the past. But that space is one of the only spaces with capital.”

Assets without capital structures, such as nonops, are more difficult to work with.

“Pricing is stalling there,” he said.

Meagher said activity has been strongest in Texas, Oklahoma and, to a certain extent, Wyoming.

Colorado’s political climate has dampened action around the state.

“The activity here in Colorado has really dropped” due to a massive legislative restructuring of industry regulations signed by the governor in April, he said.

Vital for Colorado, a coalition of state business leaders focused on energy policy, said in August that oil and gas well permitting is down dramatically compared to 2018. The state’s oil and gas regulator, the Colorado Oil and Gas Conservation Commission, is in the process of transforming from an agency “fostering” industry to “regulating” it.

That leaves would-be sellers ready to make deals but hoping to outlast the current market.

To stabilize, the market needs commodity price levels that don’t simply recover in episodic fashion, as they did in 2018, but show sustained strength, Krasny said.

Krasny said Wells Fargo has also stayed “extremely busy” despite negative sentiment. Such markets sometimes invite opportunities to make deals.

Potential sellers face either continuing along an unsustainable path for their business or selling at a less than optimal value, Meagher said.

“Sometimes the right answer is to sell. And we’re seeing companies making those decisions,” he said. “We’re seeing sponsors making those decisions quicker than they have in the past. Because it’s clear the market so far has not been improving.”

Some oil and gas transactions are also insulated from broader market woes. Minerals are particularly strong, as evidenced by Brigham Minerals Inc.’s surprisingly strong $260 million IPO in April.

Minerals continue to have more appeal, particularly because of the contrast they offer of cash flow and less risk, than the industry they overlay.

However, the location of mineral assets remains a key factor. Permian mineral interests, for instance, still command a premium.

“That asset class is exposed to the logic of the upside, which is driven by the industry’s ability to drive and continue growth of production,” Krasny said. “Because of that, it’s going to be highly dependent on the zip code.”

And the market also offers bargain basement opportunity for financially healthy companies.

As the industry makes a tectonic shift, the right kind of capital provider can make investments that do extremely well, he said, “because the valuations are at rock-bottom for some of these assets.”

But natural gas assets remain gripped by faltering prices and diminishing private-equity patience.

A Private Matter

On the 42nd floor offices of Hunton Andrews Kurth LLP in downtown Houston, the firm that represented Sabine offered little good news for momentum in the natural gas arena.

Sabine’s sale came after the company’s exit from a bankruptcy in which control resides in creditors, many of whom purchased Sabine’s debt for pennies on the dollar, said Mike O’Leary, co-head of the firm’s corporate team.

“I think unless a company in this market has to sell a gas property, because gas prices are pretty depressed right now, they’re not going to,” O’Leary said.

The potential for deals resides in companies that have no other choice, either because they’re willing to part with assets at a sharp discount to pay down debt or are forced to seek bankruptcy protection.

“Otherwise, I think people just sit on the sidelines,” he said. “This is not a really active time in the M&A market outside of those areas, or maybe you have an Osaka that wants to hedge their position.”

Phil Haines, who was part of the firm’s Sabine teams, said natural gas deals seem stuck in neutral over concerns that future associated gas production in the Permian Basin and elsewhere in the U.S. will keep prices down for the foreseeable future.

“I think a lot of the interest has been overseas because you can play the differential from continent to continent or you’ve got some other needs where you have to supply LNG,” he said.

But O’Leary said that previous Asian investment, which withered into billions of dollars in asset impairments, leaves additional future investment in doubt.

“Whether their hands are so burned from that that they won’t come back in, I don’t know. But we do some work with some of those Chinese national companies, and we haven’t heard any big movement yet,” O’Leary said.

Courtney Butler, co-lead of the firm’s capital markets practice group, said companies are attempting to run sell-side processes but there aren’t buyers because of the wide gulf between buyer’s and seller’s price points.

“We haven’t heard any of those deals getting past initial discussions,” she said.

Even companies such as British major BP Plc, which said in December it would sell up to $7 billion in Lower 48 assets to pay for its 2018 acquisition of BHP, are taking time to sell their gassier assets, he said.

“I think they’re still playing it, given what’s happened to prices since they announced” a sales process, he said. “The market is just not real strong.”

Private-equity firms are seeing a similar struggle and are considering potential combinations. The attorneys said that rumblings among private-equity firms are that there’s an unwillingness to extend some funds beyond their current expirations.

“If we’re looking at a downcycle that is going to be the next 18 to 24 months, some of these funds don’t have that long to wait,” Butler said. “So there could be forced sales.”

Deals may turn within the next 12 to 18 months because firms want to raise new funds.

“They’ve got to liquidate,” she said.

With depressed prices, wary lenders and apathetic investors, traditional exits are difficult, O’Leary said. As Krasny noted, firms are considering combinations, though those are also difficult to navigate.

“With so much concern about lower-levering portfolio companies, unless the PE firms are willing to put new equity into a buyer to [raise funds for a cash payout], you’re probably not looking at a full cash payout so PE firms can get a full exit,” O’Leary said. “It’s just a very difficult time right now.”

Below is an excerpt from the first-half 2019 U.S. E&P A&D deal list. To view the complete list, click here.

U.S. E&P Acquisitions & Divestitures |

|||||

|

Deals closed from Jan. 1-June 30, 2019. Deals closed in second-half 2018 were listed in the March 2019 issue of Oil and Gas Investor. All deals, updated in real time, are now available at HartEnergy.com/ad-transactions. |

|||||

|

Deal No. |

Estimated |

Buyer/ |

Seller/ |

Month |

Comments |

|

1 |

$7,700 |

Encana Corp. |

Newfield Exploration Co. |

2 |

Acquired The Woodlands, TX-based Newfield in an all-stock transaction and the assumption of $2.2 B net debt; includes positions in the Anadarko Basin (Stack/Scoop), Arkoma Basin, Uinta Basin and Williston Basin. |

|

2 |

$3,977 |

Chesapeake Energy Corp. |

WildHorse Resource Development Corp. |

2 |

Acquired Houston-based WildHorse in a cash-and-stock merger; includes roughly 420,000 net acre position in the Eagle Ford Shale and Austin Chalk formations in S TX with 47,000 boe/d of production (88% liquids/73% oil). |

|

3 |

$1,625 |

Murphy Oil Corp. |

LLOG Exploration Co. LLC; LLOG Bluewater LLC |

6 |

Acquired deepwater US GoM assets comprising 26 GoM blocks in the Mississippi Canyon and Green Canyon areas with 38,000 boe/d of current net production; includes up to $250 MM of contingency payments. |

|

4 |

$1,600 |

Cimarex Energy Co. |

Resolute Energy Corp. |

3 |

Acquired Denver-based Resolute which controls 21,100 net acres (89% HBP) within the Delaware Basin in Reeves County, TX, with an average 79% WI (97% operated) and average production of about 34,752 boe/d during 3Q 2018. |

|

5 |

$735 |

Aethon Energy III; Ontario Teachers' Pension Plan; RedBird Capital Partners LLC |

QEP Resources Inc. |

1 |

Bought QEP’s Haynesville/Cotton Valley business comprised of about 49,700 net acres including 137 gross operated producing wells in NW LA with production averaging 49,500 boe/d (100% dry gas) during 3Q 2018; includes midstream operations. |

|

6 |

$475 |

Ensign Natural Resources LLC; Warburg Pincus LLC; Kayne Anderson Capital Advisors LP |

Pioneer Natural Resources Co. |

5 |

Bought Pioneer’s Eagle Ford Shale assets comprising roughly 59,000 net acres in S TX with 14,000 boe/d of average net production during 4Q 2018; comprised of $25 MM at closing and $450 MM contingent payments. |

|

7 |

$400 |

Diversified Gas & Oil Plc |

HG Energy LLC; HG Energy II Appalachia LLC |

4 |

Acquired certain Appalachia assets including 107 unconventional, producing gas wells with combined net production of over 20,000 boe/d across PA and WV. |

|

8 |

$345 |

Montage Resources Corp.; Eclipse Resources Corp. |

Blue Ridge Mountain Resources Inc. |

2 |

Acquired Irving, TX-based Blue Ridge Mountain through merger; creates Montage Resources with about 227,000 net effective undeveloped core acres across the Appalachia Marcellus and Utica shales plus 500-560 MMcfe/d of pro forma production. |

|

9 |

$320 |

Sequitur Energy Resources LLC; Sequitur Permian LLC |

Callon Petroleum Co. |

6 |

Purchased Ranger operating position within the Midland Basin of the Permian comprising 85% WI in 9,850 net Wolfcamp acres averaging about 4,000 boe/d (52% oil) of production; purchase price includes contigency payments tied to oil prices of up to $60 MM. |

|

10 |

$300 |

Ring Energy Inc. |

Wishbone Energy Partners LLC; Quantum Energy Partners |

4 |

Purchased Wishbone’s North Central Basin Platform assets in the Permian comprising 49,754 gross (37,206 net) acres of mostly contiguous leasehold located primarily in SW Yoakum County, TX, and E Lea County, NM, with an average net production of 6,000 boe/d. |

|

Deals shown are those closed during first-half 2019, involving U.S.-based assets or companies only, and having values of about $20 million or more. Deals are ranked in descending estimated dollar value, when available, and then alphabetically when no value was made public or when the deal was significant but valued at less than $20 million. Deals shown as pending may have since closed. The next E&P A&D list, covering July 1-Dec. 31, 2019, will appear in the March 2020 issue of Oil and Gas Investor. Details on all deal-making, updated in real time, are available at HartEnergy.com/ad-transactions. |

|||||

List compiled by Emily Patsy.

Recommended Reading

Chevron Hunts Upside for Oil Recovery, D&C Savings with Permian Pilots

2024-02-06 - New techniques and technologies being piloted by Chevron in the Permian Basin are improving drilling and completed cycle times. Executives at the California-based major hope to eventually improve overall resource recovery from its shale portfolio.

For Sale, Again: Oily Northern Midland’s HighPeak Energy

2024-03-08 - The E&P is looking to hitch a ride on heated, renewed Permian Basin M&A.

CEO: Continental Adds Midland Basin Acreage, Explores Woodford, Barnett

2024-04-11 - Continental Resources is adding leases in Midland and Ector counties, Texas, as the private E&P hunts for drilling locations to explore. Continental is also testing deeper Barnett and Woodford intervals across its Permian footprint, CEO Doug Lawler said in an exclusive interview.

Sinopec Brings West Sichuan Gas Field Onstream

2024-03-14 - The 100 Bcm sour gas onshore field, West Sichuan Gas Field, is expected to produce 2 Bcm per year.

Orange Basin Serves Up More Light Oil

2024-03-15 - Galp’s Mopane-2X exploration well offshore Namibia found a significant column of hydrocarbons, and the operator is assessing commerciality of the discovery.