Learn more about Hart Energy Conferences

Get our latest conference schedules, updates and insights straight to your inbox.

It’s been quite a while since we’ve heard much discussion about infrastructure development coming out of the Rockies. Operators have preferred to send their cash, equipment and workforce to the prolific Permian Basin, which continues to pump out record amounts of crude.

As a result, the Southwest region has also been the focus of the bulk of pipeline activity as the midstream sector struggles to keep up with producers seeking to move supplies to Gulf Coast and East Texas refineries.

This is not to say that the Rocky Mountain region is devoid of action. As you’ll discover, activity is slowly starting to pick up. Let’s just say that it has had to wait its turn.

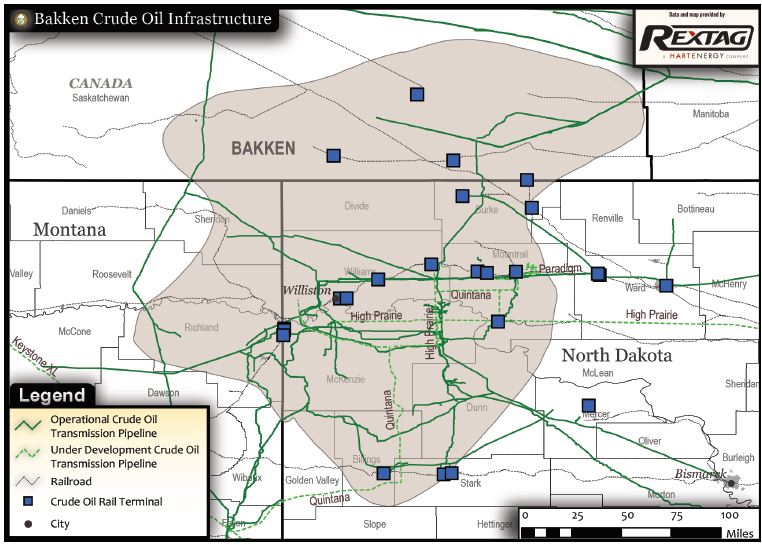

Bakken happenings

The Bakken—usually lumped into the loose “Rockies” region, although scant mountains poke above the western North Dakota prairie—remains the hub of most midstream action.

Attention is focused on two heavily publicized projects: Energy Transfer Partners’ expansion of the Dakota Access Pipeline (DAPL) and TC Energy’s Keystone XL project. The firms rank Nos. 2 and 5, respectively, on this publication’s Midstream 50 of the sector’s largest publicly held companies.

The DAPL expansion nearly doubles pipeline capacity from over 570,000 barrels per day (Mbbl/d) to 1.1 million barrels per day. The expansion will not require new pipelines but includes enhancing the existing line with two 6,000-horsepower mainline pumps and a 300,000 barrel-capacity tank, as well as adding three new midpoint pumping stations in North Dakota, South Dakota and Illinois.

The expansion is slated for completion in late 2020.

Keystone XL passed one hurdle with a court victory in Nebraska. However, a U.S. District Court judge in Montana is expected to decide late this year whether he will again block the 1,184-mile pipeline as he did in 2018, upholding arguments from environmentalists, or allow President Trump’s permit for the line to cross the border with Canada. Native American tribes are also fighting the approval.

Bruce Bullock, executive director of the Maguire Energy Institute at Southern Methodist University’s Cox Business School, is doubtful of Keystone XL’s short-term prospects.

“If I were to say right now, probably not,” he told Midstream Business. “Just based upon the balance in the crude markets, it looks like we’re headed back to a surplus again in 2020. I don’t know whether we’re going to need that crude in the East or in the U.S. Prices are forecast to go down, not up. That makes the type of crude coming out of the Canadian oil sands less economic.

“I believe Canadian companies have a longer horizon in terms of their view on these types of projects than some U.S. companies might. Therefore, they may see something in five to 10 years that they like and decide to proceed.”

Meanwhile, Enbridge, the sector’s largest firm, may add services for producers and shippers in the Bakken through further linkage between its North Dakota System and the Bakken Pipeline System in which it has an equity interest. Current system capacity out of the North Dakota Bakken is 360 Mbbl/d.

Still in limbo is ONEOK Inc.’s proposed 900-mile, 20-inch Elk Creek Pipeline, which would transport up to 240 Mbbl/d of unfractionated NGL from eastern Montana to its existing Midcontinent facilities in Bushton, Kan. The $1.4 billion project was intended to be completed by the end of this year but is delayed because of regulatory issues.

In a unique development in North Dakota, an industry-led consortium, the iPipe (Intelligent Pipeline Integrity Program) has been created to detect and prevent leaks in the state’s 27,000 miles of gathering lines by helping to commercialize new technologies.

Genscape lists other Bakken projects:

Liberty (Phillips 66/Bridger)—A 350 Mbbl/d line from the Bakken and other Rockies production areas to the Cushing, Okla., crude terminal and trading hub. Initial service is expected to commence in first-quarter 2021. Houston-based Phillips 66 will lead project construction and operate the $1.6 billion, 1,350-mile pipeline.

“The Liberty Pipeline is an important undertaking on the part of our company to ensure that oil from Wyoming, the Rockies and the Bakken can get to markets in the U.S. and around the world,’’ said Hank True, president of Bridger Pipeline. From Cushing, shippers can access multiple Gulf Coast facilities, including Corpus Christi, Ingleside and Houston in Texas.

Phillips 66 ranks No. 15 on the Midstream 50.

Portal Line (Enbridge)—Some 145 Mbbl/d will be idled to optimize mainline operations out of Canada. Reduced Bakken deliveries started in the third quarter, and the line will fully be idled in first-quarter 2020.

From Canada into the Rockies:

Express Pipeline (Enbridge)—From Canada into the Rockies, a 50 Mbbl/d expansion with use of drag-reducing agents and pump station expansions. The in-service date is expected to be first-quarter 2020.

In gas infrastructure:

LS 22-Billings Expansion—A 22.5 million cubic feet per day (MMcf/d) project in Montana, owned by WBI Energy (MDU Resources). Work had been planned for October, but it got a later-than-expected start.

It will replace 10-inch pipe with a larger diameter and increase operating pressure to allow more gas to move.

Bakken Missouri River Crossing—A 180 MMcf/d line in North Dakota, owned/announced by Kinder Morgan. Work is to start in January, but it has been unclear if the project has made it past announcements.

Colorado chronicle

Recent news has involved mergers and acquisitions, some planned expansions, and in the key state of Colorado, the focus is on Bill 181, which was signed into law last April and gives local governments increased regulatory authority over oil and gas development.

Industry officials warn that 181 threatens future investment and could ultimately kill drilling activity. The Colorado Fiscal Institute disputes this, pointing out that 181 does not ban any drilling techniques, including fracking. In addition, the study suggests that the likelihood is low of a local government, like Weld County, where 80% of current oil and gas extraction occurs in the Denver-Julesburg (D-J) Basin, banning development.

Midstream Business interviewed several consultants about Rockies’ development, and the general agreement suggests patience.

Political peril

Nathan Scott, principal, Continuum Advisory Group in Denver, acknowledges that the biggest challenge in Colorado is political, following earlier setbacks or governmental actions that resulted in a lighter version of the initiatives sought by fossil-fuel opponents. The bill was intended to be focused more on the environment, less on industry, he said.

“The writers would say they balanced it; the industry would say they shifted to anti-oil and gas. The effect is yet to be determined. How that’s going to play out, how regulation changes moving forward, is still an open question. My takeaway at this point is the uncertainty around it, particularly with significant investment, because building infrastructure to move oil and gas out of the state requires a long-term play with long-term projections,’’ Scott told Midstream Business.

“The Colorado situation, I would say, is iffy for the upstream people,” agreed SMU’s Bullock. “The ability to build additional infrastructure, to get product out there and to market, is probably going to be challenged in the coming months and years. From a gas and oil standpoint, it won’t be until later this year or early next year we’ll get relief in a lot of product coming out of the Permian. I think you will ultimately get some things built out of the Rockies, but it’s going to be more resistance up there than in other areas.”

Blame political and environmental resistance, he said, echoing Scott’s commentary.

“The voters, in fact, rejected something that was on the ballot that would have virtually shut down the industry in Colorado; so, to a great extent, they’re going about it legislatively and through regulations to make it much more difficult. And generally, these environmental groups, whatever they’re not able to stop on the upstream end, they tend to turn on the midstream end to keep pipelines from being built. That’s probably where they’ll turn their attention to next,” Bullock said.

Scott said the need for oil vs. natural gas pipelines is “fairly balanced at this point.”

Market driven

“The market drives it; there’s more money in oil as gas prices have continued to stay low. In most states in the West, flaring of gas is not okay, particularly over the long term, and is gaining ire from regulators along with attention from environmentally concerned groups. Fracking and the nature of how we’re extracting oil in most fields in the Rocky Mountains produces a lot of gas that you have to be able to take off, so the need there is for both.

“I’m not sure of percent-of-capacity for long-haul natural gas vs. oil. There are still projects on the drawing board continuing to move oil. At a local level, if you’ve got wells, at least, from a gathering line perspective and getting into compression facilities, there’s still a need for [pipelines] because you can’t burn it off or store it onsite,” Scott said.

The price conundrum

The economics of production and moving gas out also present one of the biggest challenges that the Rocky Mountain region faces.

“The value of the hydrocarbons is discounted in the Rockies region; the problem is there’s an even greater discount elsewhere,” Greg Haas, director, integrated oil and gas, at Hart Energy’s Stratas Advisors, told Midstream Business. “Recently there were deep discounts, and even negative prices, in the Waha gas basin of West Texas. That was the result of much more associated gas than anyone anticipated. Coming with this very strong growth in crude output, the gas came online before anybody anticipated the need for new pipelines.

“That created an overhang of natural gas in the Waha region which then drove prices negative. We recently saw one significant pipeline startup from the Waha area, and that has brought it [prices] back into positive territory. But it’s around a dollar and change. Henry Hub is $2.40 [per MMBtu] or so today. The price of Colorado or Wyoming gas is about $1.90 or so. How can you get past this wall of West Texas gas economically coming all the way from the Rockies if you’re heading toward the Gulf Coast?

“That’s the real question,” he continued. “If you’re going west to California, you don’t have a lot of options, so that can pay if demand is there. If you’re going east, you have to overcome the wall of gas coming out of Appalachia in the Marcellus/Utica. If you’re trying to go south, you’ve got that wall of gas in the Permian. All of that is really pressuring the cost of moving and producing gas in the Rocky Mountain region.”

Niobrara-D-J

The Niobrara-Denver-Julesburg Basin is a crude oil and liquids-rich gas play located in northeastern Colorado and southeastern Wyoming. The Niobrara is also located in several other areas of the Rocky Mountains, including the Powder River Basin in Wyoming and in parts of northwest Colorado.

The Niobrara production area in the Rockies is a complicated place to determine crude oil supply and demand balances, analyst John Zanner wrote for RBN Energy. It’s at the crossroads of a number of supply areas, with volumes coming in from Canada and the Bakken, as well as locally from the Powder River and D-J basins.

“In terms of destinations, there are well-established local markets, or you can send the molecules to Salt Lake City, or southeast to the Cushing hub and beyond. The Niobrara is one of the few growth areas we look at where there is substantial pipeline capacity for inflows and outflows, with the option to service multiple markets. Now, there are a couple of new pipeline projects ramping up in the Rockies, and given the region’s interconnectivity, it’s a good bet that the status quo in the Niobrara is in for some big changes,” he said.

Edward C. Kelly, vice president, Americas Gas & Power Consulting, IHS Markit, told Midstream Business, “We see one oil pipeline moving forward out of the Niobrara, but new natural gas pipelines leaving the Rockies await the resumption of net production growth in the region.”

Uinta Basin

The Uinta Basin in northeastern Utah contains huge reserves of unusual, waxy crude oil with many characteristics that refiners desire: medium-to-high API gravity and very low sulfur, acid and metal content. The combination of long horizontal wells and hydraulic fracturing offers producers access to the basin’s product at a remarkably low cost per barrel. However, as consultant Housley Carr wrote for RBN Energy, the crude is difficult to transport, posing a major economic and logistical challenge: cost-effective transport to distant markets.

“Refineries in nearby Salt Lake City have been making good use of the waxy oil for decades, but there are limits to how much they can process, so Uinta Basin producers, midstreamers and investors have been working on ways to move large volumes to faraway places like the Gulf and West coasts. They may finally be making real progress,” Carr wrote about the prospects for taking the often-overlooked Utah play to the next level.

Though the fast-growing Denver, Boulder and Salt Lake City metro areas provide a substantial market for Rockies gas, new problems arise as pipelines begin to encroach into more densely populated regions, creating local opposition.

However, the plan has long been to ship that gas to the West Coast. Currently the major route for Rockies gas is via Kinder Morgan’s 680-mile, 1.5 billion cubic feet per day (Bcf/d) Ruby Pipeline, extending from Wyoming to Oregon. For crude, producers want more routes to the Cushing hub and to West Texas, from where it can easily be shipped to the Gulf Coast.

Noble Midstream

Noble Midstream Partners LP, a leading developer in the Rockies, is partnering with Greenfield Midstream LLC in a joint venture, Black Diamond Gathering LLC, which provides crude oil gathering and storage services to producers in the Denver-Julesburg Basin. Black Diamond has a strategic relationship with Saddlehorn Pipeline Co., owned by

Magellan Midstream Partners LP, Plains All American Pipeline LP and Western Midstream Partners LP.

Saddlehorn is capable of transporting 190 Mbbl/d of crude oil and condensate from the D-J and Powder River basins to storage facilities in Cushing, owned by Magellan and Plains. After a successful open season, Saddlehorn will be expanded by 100 Mbbl/d to 290 Mbbl/d. The higher capacity should be available in late 2020 with additional incremental pumping and storage.

Black Diamond has secured a 15-year oil gathering dedication from Verdad Resources, encompassing 85,000 acres and over 750 potential drilling locations in the D-J Basin in southern Weld County. The total acreage dedicated to the Black Diamond system is now 243,000 acres.

Noble Midstream operates Black Diamond, which includes a large-scale integrated crude oil gathering system in the D-J, consisting of 240 miles of pipeline in operation, 300 Mbbl/d delivery capacity and 390 Mbbl/d crude oil storage capacity. The system is connected to every major takeaway pipeline in the D-J Basin, including White Cliffs Pipeline, Saddlehorn Pipeline, Grand Mesa Pipeline and Pony Express Pipeline.

DCP Midstream

DCP Midstream has been among the nation’s top gas processors and NGL producers for over a decade. Following the price downturn several years ago, the company has focused on a “relaunch” dubbed DCP 2.0. Investing in fee-based growth projects has resulted in a 65% increase in fee-based gross margins so far this year.

The DCP 2.0 strategy uses technology to drive optimization and improve efficiencies throughout its portfolio of assets. The D-J Basin has been a standout play this year with a double-digit, year-over-year volume growth in the second quarter. This region is poised for even more growth following a long-term agreement with Western Midstream Partners to provide up to 225 million cubic feet per day (MMcf/d) of incremental processing capacity by mid- 2020, said company officials.

DCP had partnered with SemGroup Corp. on the project, but in September, SemGroup was purchased by Energy Transfer in a $5 billion deal that establishes Dallas-based Energy Transfer as a major shale oil and NGL player in the Rockies with its first infrastructure in the D-J Basin.

By adding SemGroup’s export terminal on the Houston Ship Channel, this could lead to a significant export market for D-J producers, according to published reports.

Tallgrass Energy Partners

Sept. 18 was a significant day for Tallgrass Energy LP as the Federal Energy Regulatory Commission authorized certificates for its Cheyenne Connector and REX Cheyenne Hub Enhancement projects. The Cheyenne Connector Project involves construction of a 70-mile, large-diameter interstate natural gas pipeline to transport natural gas from processing plants in the D-J Basin in Weld County to the Rockies Express Pipeline (REX) Cheyenne Hub just south of the Colorado-Wyoming border.

This would provide access to interconnected pipelines and local distribution systems at the REX Cheyenne Hub as well as interconnected systems downstream of REX that reach end users in West Coast markets, Midwest markets such as Chicago and Detroit, the Gulf Coast and Southeast. Tallgrass said the Cheyenne Connector has an estimated initial design capacity of 600 Mcf/d with potential for expansion. Precedent agreements for a combined 600 Mcf/d have already been signed by affiliates of DCP Midstream and Occidental.

The 1 Bcf/d enhancement of the REX Cheyenne Hub in Weld County includes modifications to accommodate multiple natural gas pipelines with various operating pressures in providing customers increased diversity in terms of market access. It is expected to be in-service during first-quarter 2020.

Black Hills Corp.

Rapid City, S.D.-based Black Hills Corp. has announced plans to expand its energy business with the expenditure of up to $2.5 billion over the next five years, including over $1.6 billion for natural gas utilities in the process of being consolidated in Colorado, Nebraska and Wyoming, according to Linn Evans, CEO.

Among the main components of the program is a natural gas transmission pipeline planned for central Wyoming, he said. Black Hills Gas Distribution LLC is constructing the 35-mile, 12-inch Natural Bridge Pipeline at a cost of $54.2 million. It will run from Douglas to Casper, Wyo. The company has 57,000 customers in central Wyoming. Black Hills has also won approval to combine two Colorado gas distribution utilities into Black Hills Colorado Gas Inc.

Waiting on the Permian

Bullock believes many developers are waiting for pipeline activity to finish up in the Permian before they move up into the Rockies.

“I think that’s part of it,” he said. “They will certainly get more relief which should come by first quarter of 2020. That’s reason to look elsewhere. I think there’s more political risk in the Rocky Mountain region that has a chilling effect.”

And could the national election factor into this for operators and their investors, who may be holding back on their investment, just in case?

“It’s a two-edged sword on projects that are possibly going to require significant capital past 2020. Any approvals past 2020, they probably are holding back on. On the other hand, things that they can get done through the remainder of 2019 and in 2020 in terms of decisions on capital deployed, I think they’re probably speeding those up,’’ Bullock said. Another factor slowing investment is shareholder pressure on public companies.

“Shareholders have spoken loudly that they want these public companies to return money either through dividends, buybacks or other mechanisms. For the most part through the growth stages since 2012 a good portion of the companies have not done that. They’re having to reduce their capital budgets on top of these lower prices. This is definitely having a chilling effect on investment,” he said.

_____________________________________________________________________________________________________________________________

Jeffrey Share is a Houston-based Hart Energy contributing editor specializing in midstream energy topics.

Recommended Reading

Exxon Mobil Guyana Awards Two Contracts for its Whiptail Project

2024-04-16 - Exxon Mobil Guyana awarded Strohm and TechnipFMC with contracts for its Whiptail Project located offshore in Guyana’s Stabroek Block.

Deepwater Roundup 2024: Offshore Europe, Middle East

2024-04-16 - Part three of Hart Energy’s 2024 Deepwater Roundup takes a look at Europe and the Middle East. Aphrodite, Cyprus’ first offshore project looks to come online in 2027 and Phase 2 of TPAO-operated Sakarya Field looks to come onstream the following year.

E&P Highlights: April 15, 2024

2024-04-15 - Here’s a roundup of the latest E&P headlines, including an ultra-deepwater discovery and new contract awards.

Trio Petroleum to Increase Monterey County Oil Production

2024-04-15 - Trio Petroleum’s HH-1 well in McCool Ranch and the HV-3A well in the Presidents Field collectively produce about 75 bbl/d.

Trillion Energy Begins SASB Revitalization Project

2024-04-15 - Trillion Energy reported 49 m of new gas pay will be perforated in four wells.