Learn more about Hart Energy Conferences

Get our latest conference schedules, updates and insights straight to your inbox.

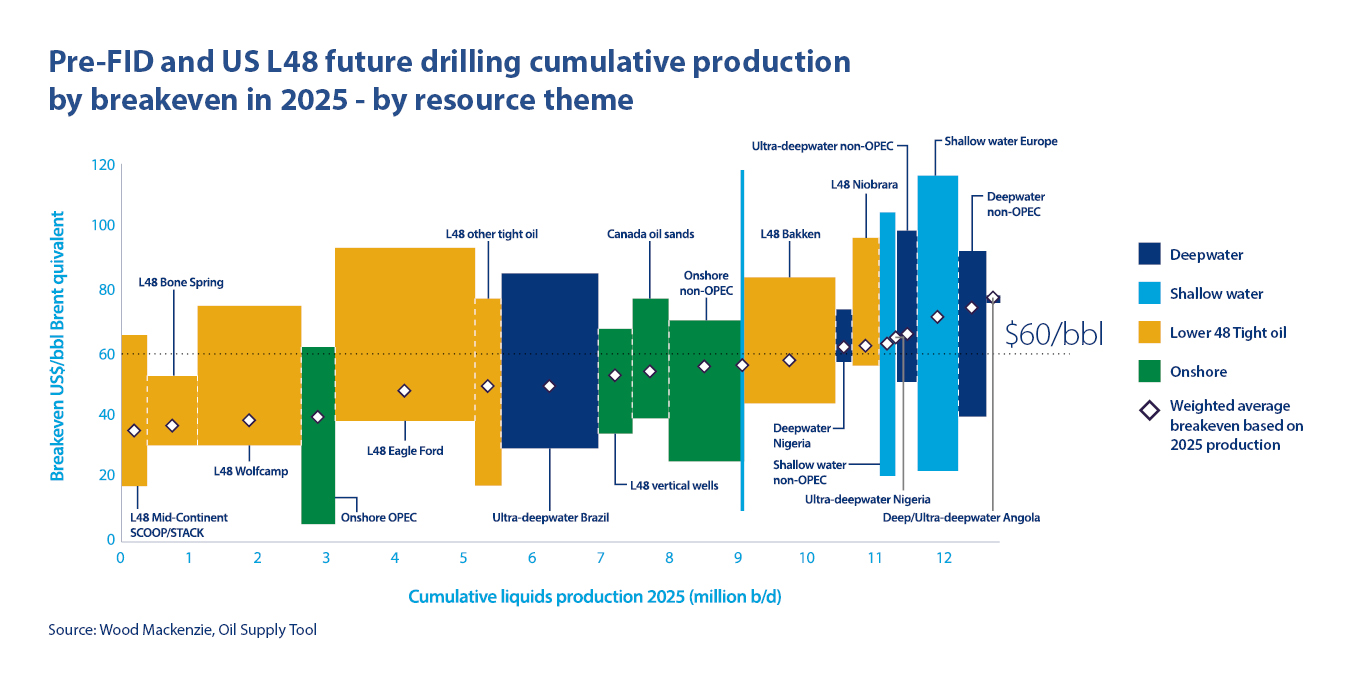

A price of $60 or less for a barrel (bbl) of Brent crude should not hinder the commerciality of most new drilling projects in U.S. tight oil plays.

That’s according to the latest study unveiled by Wood Mackenzie, which said its global oil market analysis showed that 70% of such projects and conventional oil projects in the pre-financial investment decision (pre-FID) phase are commercial at $60 oil. A year ago the firm put the number at 50%.

In the time since, oil and gas companies grappling with the aftermath of one of the industry’s worst downturns have learned to live with less. They have turned to technology and improved techniques while securing service and supply discounts, stalling projects, reducing operational costs and leaving wells uncompleted until market conditions improve to desired levels and demand growth predictions become reality.

Of the 13 MMbbl/d of new supply that could come from tight oil and conventional projects by 2025, 9 MMbbl/d is commercial at $60 oil, according to the firm.

“Global breakeven costs for these developments have fallen by US$19/bbl to the current weighted average of US$51/bbl since the peak in 2014 and by US$8/bbl over the past 12 months,” said Patrick Gibson, global oil supply research director for Wood Mackenzie.

Dominating the low-end of the cost curve is new U.S. tight oil drilling, which Wood Mackenzie said could account for 60% of the production that is commercial at $60/bbl.

The advent of tight oil, productivity improvements and cost deflation in main plays have changed the firm’s previous pre-FID outlook, Wood Mackenzie’s Harry Paton said in a video report on the firm’s research. Looking back to 2009, he said 6 MMbbl/d was commercial at $75/bbl.

“Now that number has doubled,” said Paton, research analyst for global oil supply. “Tight oil has pushed the cost curve lower, longer and flatter.”

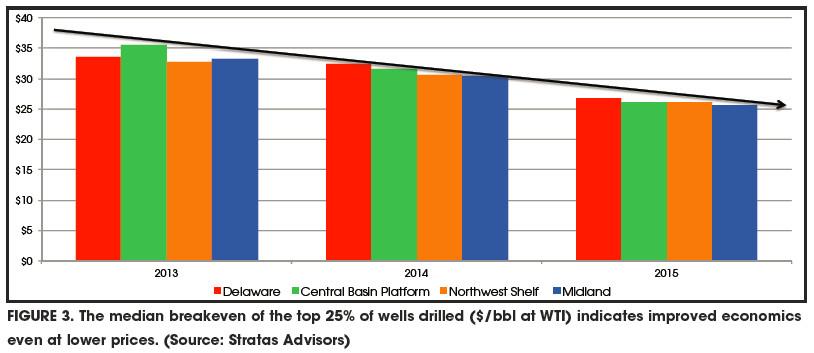

The findings could bode well for companies operating in tight oil plays such as the Eagle Ford and in the Permian Basin, which have weathered the downturn better than most, according to Stratas Advisors.

“When the median well-level economics from 6,800 wells across the basin is compared and ranked by vintage, the median breakevens have continuously trended downward since 2012,” Jessica Pair, an analyst for Stratas, said in an update on the economic reality of the Permian.

She assessed the economics using West Texas Intermediate (WTI) prices.

“Currently, the median breakeven across the basin ranges from about $54/bbl to $64/bbl. When focusing on the top 25% of these wells by economic and production performance, the median breakeven decreases to a range of about $30/bbl to $33/bbl,” she said. “Under market conditions fluctuating between $40/bbl and $48/bbl, the top 25% of wells drilled within the Permian remain economic.”

Wood Mackenzie singled out Apache Corp. (NYSE: APA), Chevron Corp. (NYSE: CVX), Continental Resources (NYSE: CLR), EOG Resources (NYSE: EOG), ExxonMobil Corp. (NYSE: XOM) and Pioneer Natural Resources Corp. (NYSE: PXD)—all major tight oil players—as potential “big winners in this dynamic.”

Companies have been focused on generating strong returns at lower oil prices. EOG, in particular, has zoned in on premium drilling and completions this year as it defines wells that generate a 30% after-tax rate of return at $40 flat oil.

RELATED: EOG: Rebuilt And Better Than Before

While the research points to a potentially promising future for U.S. tight oil, the same is not the case for some other projects. Wood Mackenzie warned that many of the major conventional projects were at risk of being stalled or canceled at about $50/bbl like the many expensive deepwater ones that have already been shelved such as offshore Angola and Nigeria.

The firm previously reported that global upstream and exploration spending has already fallen by more than $1 trillion since oil prices began to nosedive in 2014, the result of a supply-demand imbalance.

“We have seen some helpful cost deflation over the last couple of years … but overall deepwater economics are a challenge,” Paton said. “Importantly though, the majority of these projects are required to meet demand.”

There are, however, some competitive deepwater regions, he added, turning to Brazil. With “world-class projects of scale such as Libra,” Brazil has an average breakeven of $50/bbl.

Just this week, Petrobras said it brought FPSO Cidade de Saquarema onstream in the Santos Basin’s Lula Field. The Lula production system is the 10th large definitive production system operating in the pre-salt layer. Petrobras anticipates bringing its next pre-salt system, located in the Lapa Field, online in third-quarter 2016 through installation of the FPSO Cidade de Caraguatatuba.

Velda Addison can be reached at vaddison@hartenergy.com.

Recommended Reading

Seadrill Awarded $97.5 Million in Drillship Contracts

2024-01-30 - Seadrill will also resume management services for its West Auriga drillship earlier than anticipated.

TotalEnergies Starts Production at Akpo West Offshore Nigeria

2024-02-07 - Subsea tieback expected to add 14,000 bbl/d of condensate by mid-year, and up to 4 MMcm/d of gas by 2028.

Well Logging Could Get a Makeover

2024-02-27 - Aramco’s KASHF robot, expected to deploy in 2025, will be able to operate in both vertical and horizontal segments of wellbores.

Shell Brings Deepwater Rydberg Subsea Tieback Onstream

2024-02-23 - The two-well Gulf of Mexico development will send 16,000 boe/d at peak rates to the Appomattox production semisubmersible.

E&P Highlights: Feb. 26, 2024

2024-02-26 - Here’s a roundup of the latest E&P headlines, including interest in some projects changing hands and new contract awards.