They rarely dominate the headlines, and their executives tend to dodge the spotlight. But make no mistake, private E&Ps across the U.S. and in the Gulf of Mexico produce such a significant volume of oil and natural gas that the nation wouldn’t have gained its leading role in geopolitics without their supply.

Enverus analyst Justin Lepore analyzed the production of top private producers for Hart Energy’s readers and Deon Daugherty, Oil and Gas Investor’s editor-in-chief, asked Enverus’ executive director, Gibson Scott, to put it all into perspective in an exclusive interview.

Deon Daugherty: What are the key takeaways when you compare this list of the top private producers with previous years?

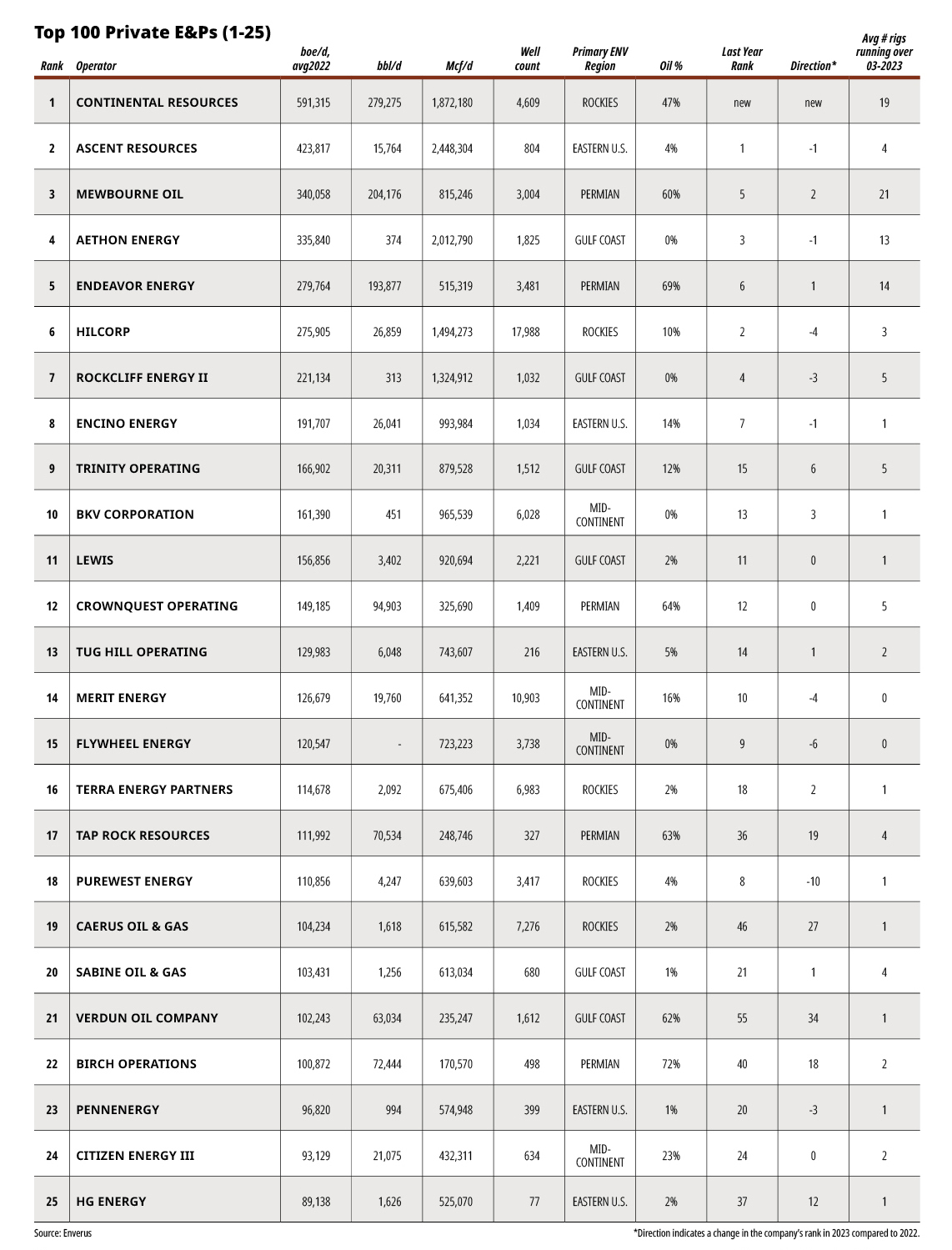

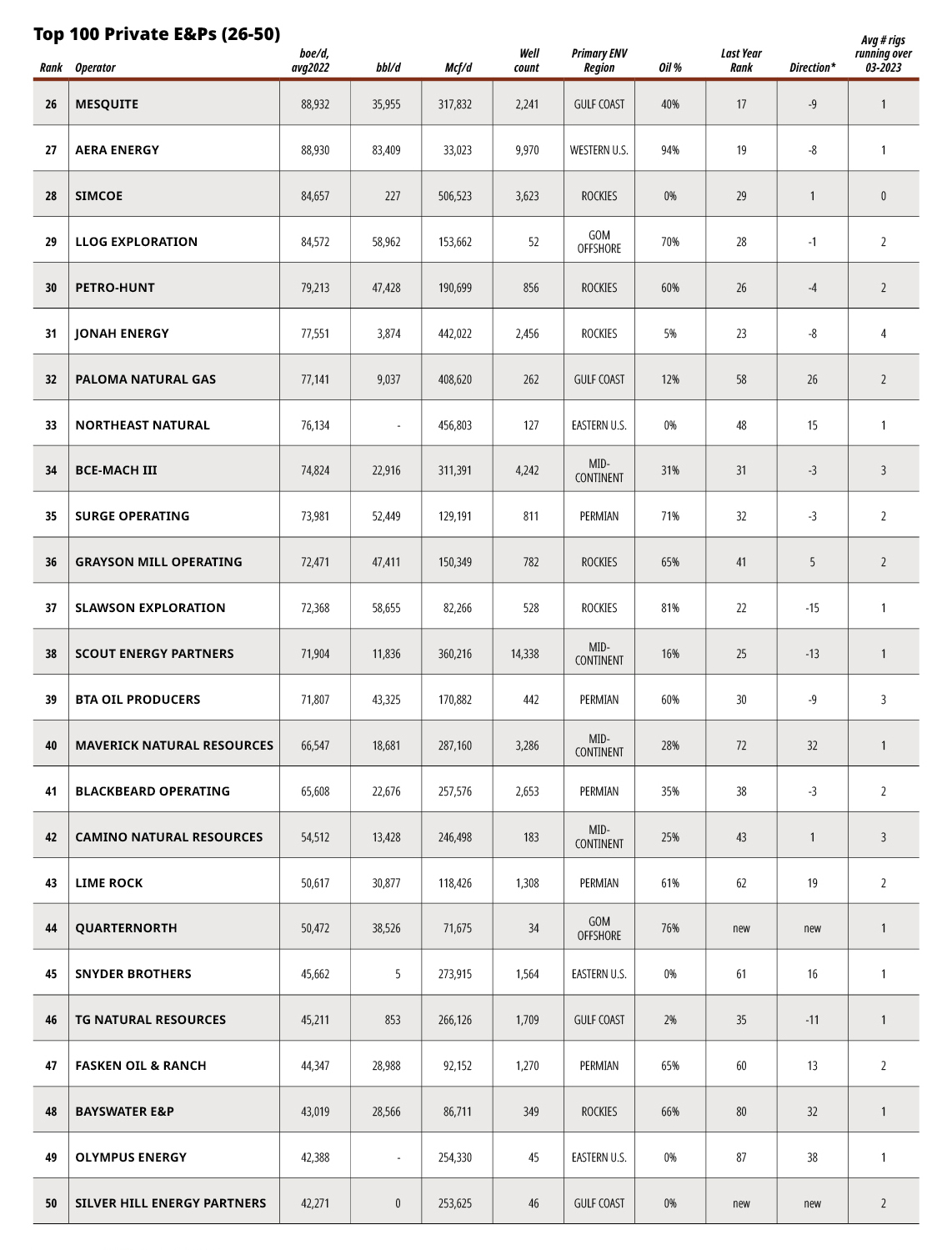

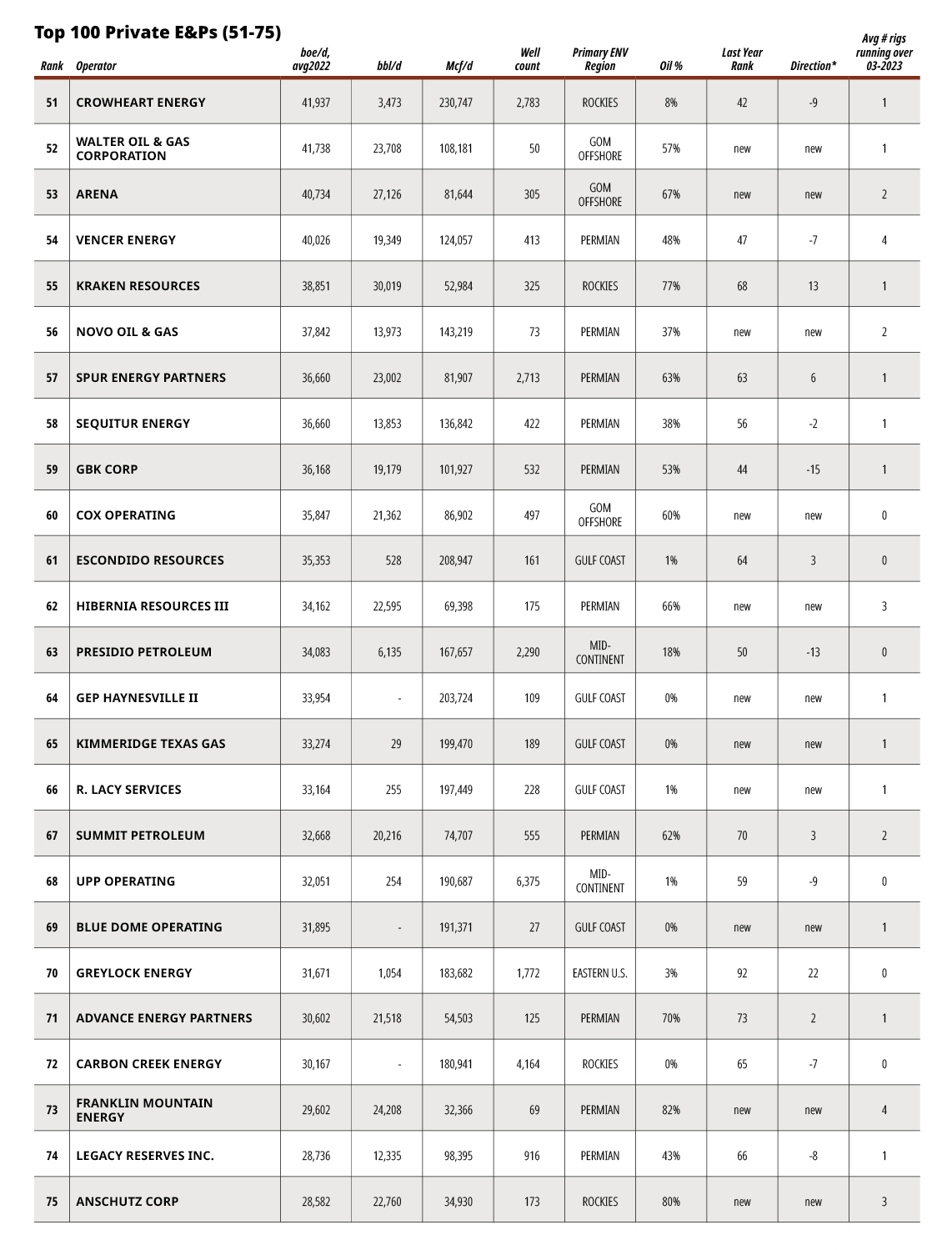

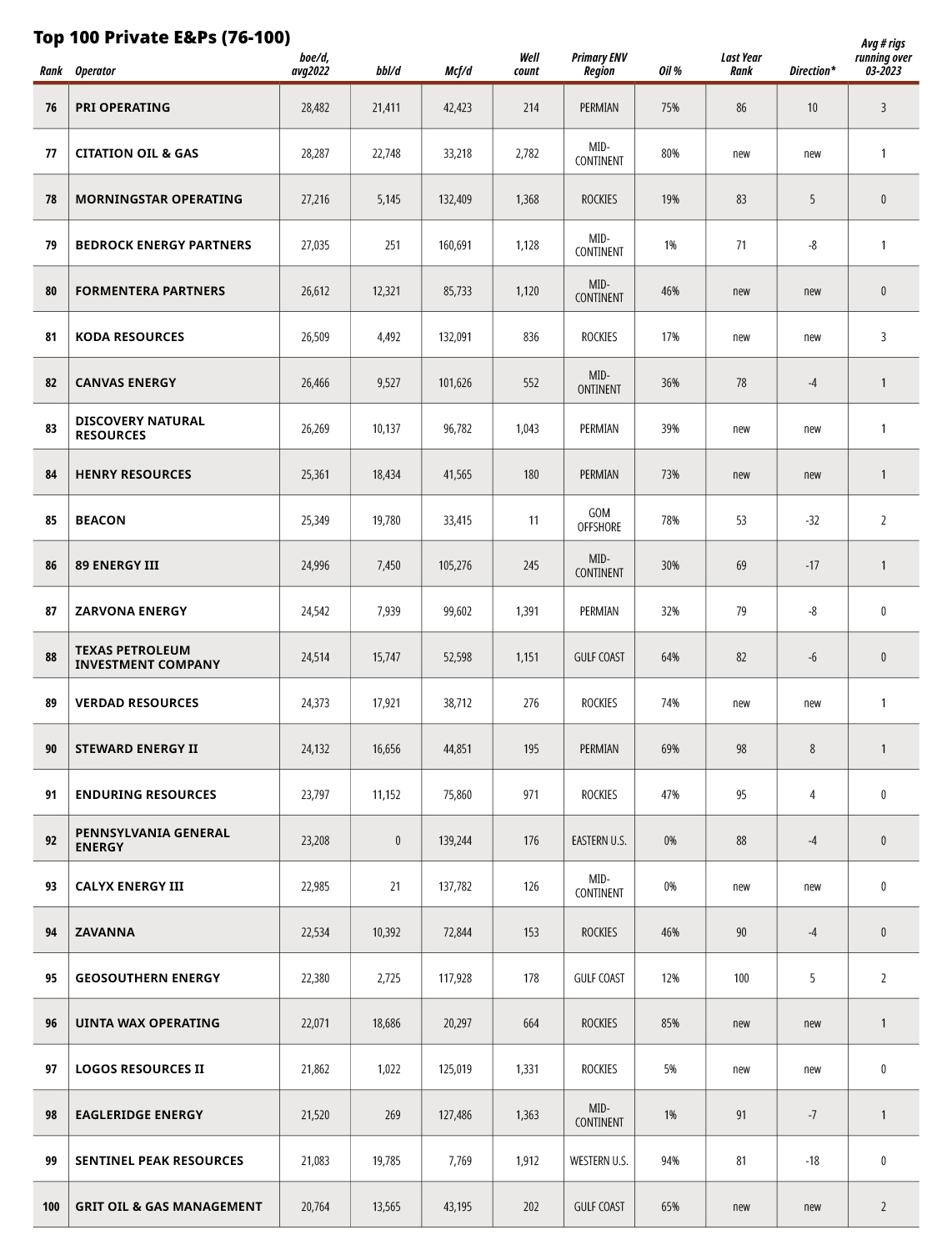

Gibson Scott: The top 100 private producers delivered 25% more production from the Lower 48 and the Gulf of Mexico in 2022 compared to 2021, or 7.8 MMboe/d compared to 6.2 MMboe/d. At the same time, total production from these regions grew by only 5%, meaning private companies gained share in the market.

Some of this is driven by the take-private of Continental Resources, now the largest private producer in our list. However, overall, we added about the same number of new private companies to our list as we lost, either as a result of changing production levels or M&A, meaning the average private company is getting larger in size—or longer in the tooth, depending on your perspective.

DD: How is the private E&P landscape changing? Given this year’s M&A activity in which large public companies are acquiring private producers, will the private space shrink considerably or do you anticipate private equity to step in with cash to develop more private producers?

GS: Although the rate of replenishment to the pool of private upstream operators is low, as private equity seeks to monetize their investments and redirect capital to other parts of the energy value chain, the rate of depletion is also low.

Fewer and fewer companies exhibit the scale, depth of inventory, base decline, ESG profile and cost basis to attract public company attention, and even fewer are likely to crystalize their value through initial public offerings. As a result, we expect the number of private companies to stay fairly consistent over the next few years, with the average private company continuing to increase in size.

DD: How has private E&Ps’ access to capital changed with ESG and other current dynamics? What is the role of private equity in the space?

GS: Although private equity capital for new upstream oil and gas start-ups has all but evaporated, there are still a large number of private equity-backed entities on our list. Like their public counterparts, many private companies have found capital discipline over the past couple years and rely much less on their investors for development or growth capex.

I suspect that a declining opportunity set for new entities, combined with less ongoing outside capital requirements, is driving less private equity investment in the space, as opposed to any ESG-driven mandate to divest from hydrocarbons. Although new start-ups are becoming more rare, private equity continues to play an important role in the space. Many PE firms provide valuable strategic advice, back-office support, or a common technology platform, like Enverus, to their portfolio companies.

DD: What trends have you noticed with regard to private E&P production? Do private operators supply the same quantity of production—35-40% is my understanding of recent years—or will large public companies increase their portion of U.S. supply?

GS: Private companies currently supply about 37% of total U.S. production. We expect this figure to continue to grow as public operators temper growth alongside spending, while private operators chase the scale necessary to make themselves more suitable acquisition candidates.

DD: What are the factors that influence private E&P growth?

GS: The introduction of new private equity-backed companies requires PE capital directed to the upstream oil and gas space, a focus we’ve seen blur over the past few years. Existing private companies may continue to invest in growth, either by reinvesting cash flow or seeking outside capital providers. However, growth is somewhat limited by dwindling inventory levels. Private operators need to balance the desire for growth and scale without burning through the remaining inventory that is so sought-after by public acquirers or public markets.

DD: How are private companies responding to volatility in commodity prices? What is the “sweet spot” for these producers?

GS: Private company activity is more sensitive to commodity prices than publics’, largely because, on average, their assets are lower quality and swing in and out of the money more often. That said, private companies typically have smaller, more flexible drilling programs and can be more responsive to changing commodity prices compared to large public operators who typically engage in longer term OFS [oilfield service] contracts.

DD: What cost drivers must they consider and do they differ from those of public companies?

GS: Small privates are more exposed to swings in the OFS spot market and do not benefit from higher negotiating power with OFS from large, steady programs.

DD: How has technology—and access to it—impacted private companies?

GS: Any technology advantages that private operators may have once enjoyed have eroded as shale has matured and the knowledge gap across all operators has narrowed.

DD: What regions have the most opportunity for private companies?

GS: Private companies played a key role in delineating new resource opportunities. While demand for new resource opportunities remains high, it is increasingly difficult to prove commerciality. Early-life plays like the Austin Chalk, and peripheral areas of non-Permian plays are conducive to resource-expansion strategies and important playgrounds for private operators.

RELATED

Top 15 Private E&Ps in the Midcontinent, Gulf Coast

Top Private E&Ps in Eastern U.S., GoM

Recommended Reading

Enbridge Advances Expansion of Permian’s Gray Oak Pipeline

2024-02-13 - In its fourth-quarter earnings call, Enbridge also said the Mainline pipeline system tolling agreement is awaiting regulatory approval from a Canadian regulatory agency.

Moda Midstream II Receives Financial Commitment for Next Round of Development

2024-03-20 - Kingwood, Texas-based Moda Midstream II announced on March 20 that it received an equity commitment from EnCap Flatrock Midstream.

NGL Growth Leads Enterprise Product Partners to Strong Fourth Quarter

2024-02-02 - Enterprise Product Partners executives are still waiting to receive final federal approval to go ahead with the company’s Sea Port Terminal Project.

Magnolia Oil & Gas Hikes Quarterly Cash Dividend by 13%

2024-02-05 - Magnolia’s dividend will rise 13% to $0.13 per share, the company said.

BP’s Kate Thomson Promoted to CFO, Joins Board

2024-02-05 - Before becoming BP’s interim CFO in September 2023, Kate Thomson served as senior vice president of finance for production and operations.