DALLAS—Public companies have set a promising stage for themselves over the next five years, S. Wil VanLoh, founder and CEO of private-equity provider Quantum Energy Partners, said March 5 to open the Energy Capital Conference.

E&Ps are entering a new stage in their development in which they extend cost cutting and efficiencies while maximizing their profits with technology, logistics and marketing, he said.

“If you’re a private operator in the room today that should scare you,” VanLoh said. “Shale 3.0 is about efficiency, it’s about manufacturing and the advantage of that often goes to the larger company that can bring economies of scale to the table.”

Shale 3.0 is what VanLoh calls the third iteration of shale phenomenon. According to VanLoh’s nomenclature, Shale 1.0 represented the E&P land grab from 2007 through the end of 2011 while Shale 2.0 was the productivity phase from 2012 through 2016. Since 2017, operators have been embarking on increased efficiency through data analytics, logistics and procurement and commodity marketing.

As they’ve become more focused on process, public companies are in the process of consolidating acreage.

“If you look at the top 10 independents in the U.S. at their current rig cadence they’ve got a 44 year inventory,” he said.

That doesn’t include potential upside — just stated locations, he said.

To entice a public buyer, private-equity companies have to offer assets that can displace a public company’s top-quartile inventory.

“That’s increasing becoming a harder thing to do in the private equity world. And in a world where public companies are going to be more and more disciplined about what they’re going to buy” he said.

Public E&Ps have also helped blocked the public-market exit ramp for private-equity companies. Years of shoddy fiscal discipline that has turned off the public markets that funded more than a trillion dollars in capital in the shale race.

“A lot of that capital was spent inefficiently, really alienating a lot of investors particularly in the public realm that have supported this industry for so long,” Van Loh said.

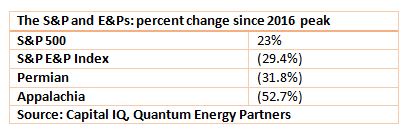

What’s resulted is “really almost a disdain almost for energy,” which frustrated investors have walked away from, VanLoh said. While the broader S&P has fared well since 2016, E&Ps in that universe continue to suffer, trailing the broader market by about 52 percentage points.

Public companies are in the process of trying to “heal that relationship” through capital discipline, returning capital to investors and reducing debt.

“That’s got pretty profound implications … for public investors but also creating opportunities for private companies to gain meaningful market share,” he said.

companies are also exploring large-scale development using pad drilling.

The public markets remain a tough environment for private companies. In 2016 and 2017, private upstream exits averaged about $6 billion to $7 billion a quarter, VanLoh said. “The last almost two years its averaged a little over $1 billion a quarter.”

Public companies are also exploring large-scale development using pad drilling.

However, even for large companies, pad development involves risk and huge capital outlays. A 24-well pad may cost as much as $300 million. Even an eight-well pad consumes the equivalent of a quarter-billion pounds of sand and 305 Olympic-sized swimming pools of water.

That makes logistics and procurement even more important to those companies. Public E&Ps are also increasingly relying on data analytics, robotics and commodity marketing. Embracing technology could and other efficiencies could save companies $8 to $10 per barrel of oil.

Even getting products to market has given public companies an advantage, with some prominent Permian Basin companies able to export their oil and NGLs.

“There was a point last year at which there was a $15 to $20 delta between what companies really on top of the marketing side of their business [earned] and what private operators were getting”

Private companies will be challenged to keep up while still making themselves attractive to would-be buyers.

“Logistics and procurement are a huge part of this business going forward,” he said.

Ultimately, that will mean private operators face a significant strategic shift in how they do business, one in which they hold land for perhaps twice as long as they did leading up to 2016 and focus more on cash flow metrics than the net asset value (NAV) of undrilled locations.

Private operators have responded, increasing rig counts at a faster pace than publics and now operate 37% of rigs compared to about 30% during the past several years, VanLoh said.

With among the best breakevens production costs in the world, VanLoh said the U.S. shale revolution has largely been won. In retrospect, that may have been the easy part.

Recommended Reading

Energy Transition in Motion (Week of March 22, 2024)

2024-03-22 - Here is a look at some of this week’s renewable energy news, including a new modeling tool for superhot rock.

Tax Credit’s Silence on Blue Hydrogen Adds Uncertainty

2024-01-31 - Proposed rules for the 45V hydrogen production tax credit leave blue hydrogen up in the air, but producers planning to use natural gas with carbon capture and storage have options.

DOE Considers Technip, LanzaTech For $200MM ‘Breakthrough’ Technology Award

2024-03-25 - The U.S. Department of Energy funding will be used to develop technology that turns CO2 into sustainable ethylene.

CEO: Linde Not Affected by Latest US Green Subsidies Package Updates

2024-02-07 - Linde CEO Sanjiv Lamba on Feb. 6 said recent updates to U.S. Inflation Reduction Act subsidies for clean energy projects will not affect the company's current projects in the United States.

Exclusive: ‘Reality Has Hit,’ NatGas Not Just a Bridge Fuel, Landrieu Says

2024-04-11 - The Biden administration's LNG pause is "disappointing" and natural gas is a "solution to energy woes," co-chairs for Natural Allies for a Clean Energy Future Senator Mary Landrieu and Congressman Kendrick Meek told Hart Energy's Jordan Blum at CERAWeek by S&P Global.