The histrionics surrounding TransCanada Corp.’s proposed project equate to a footnote in the story of cross-border trade that brings a net average of 2.6 million barrels per day (bbl/d) of crude oil and 14 billion cubic feet per day (Bcf/d) of gas into the U.S., much of it from western Canada.

The commercial energy bonds linking the U.S. and Canada have experienced a 59% increase in U.S. crude oil imports in the past 10 years, according to the U.S. Energy Information Administration (EIA), during a time when imports from most other major suppliers have declined. This development results in part from the increase in domestic production from uncon- ventional plays as well as the simple economics of purchasing from a neighbor.

Hydrocarbons in the Western Canadian Sedimentary Basin (WCSB) are mostly packed into Devonian layers of between 368 million and 413 million years old. Oil exploration began in Alberta in 1883, some 32 years after the country’s first crude came bubbling up near Black Creek, Ontario. Prior to World War II, though, only Turner Valley, which established Calgary, Alberta, as the country’s oil and gas capital, could be considered a major field.

Then the war—and gasoline rationing—ended in 1945 and the search began in earnest for resources around the continent to support a developing “American Graffiti”-style culture of driving, driving and driving.

In 1947, the Leduc No. 1 well, about 50 miles south of Edmonton, Alberta, began flowing at 5,066 feet and a new era of western Canadian oil and gas preeminence was born.

Promise of LNG

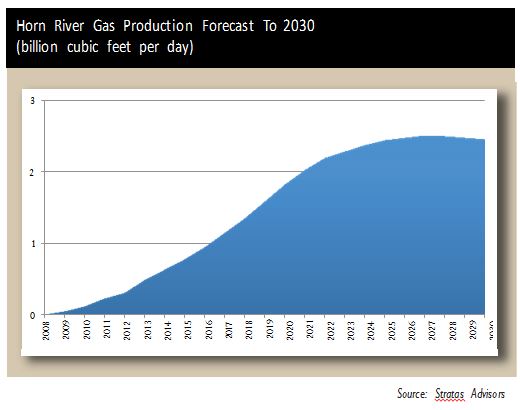

Canada trails only the U.S., Russia, Iran and Qatar in global production of natural gas, most of it from the WCSB and its gas- rich Montney and Horn River unconventional plays. In 2013, the country flowed 2.8 trillion cubic feet (Tcf) south to the U.S., its only gas trading partner, the EIA reported. That’s down from a peak of 3.8 Tcf in 2007, and that total is expected to continue to drop as U.S. gas production continues to rise amid sluggish demand.

Among the major gas movers are TransCanada Corp., which operates 42,100 miles of lines; and Spectra Energy Corp., which moves 2.9 Bcf/d on its western Canada-based system. Both have project proposals that hinge on LNG exports.

TransCanada’s Prince Rupert Gas Transmission Project would take gas 466 miles from Fort St. John to Port Edward, British Columbia. British Columbia’s provincial government certified the project for approval last November. Spectra’s Westcoast Connector Gas Transmission Project, which it is proposing with the BG Group, would connect northeast British Columbia to the proposed LNG export facility near Prince Rupert. That project was also certified by the provincial government in November.

“Should these terminal projects and their associated supply pipeline projects come to fruition,” said a report by Stratas Advisors, a Hart Energy company, “much of the regional gas production will be expected to move west to the new demand centers.”

The oil-price link

Stratas notes that many LNG price contracts are linked to the market price of oil, which has suffered a steep decline. In response, British Columbia’s provincial government is considering implementation of a sweetened tax incentive program to encourage final investment decisions on LNG facilities. The new rules would allow builders to deduct capital costs at an upwardly adjusted rate, allowing them to recover their costs more quickly.

“The revised tax policy should lower the bar for entry in the LNG export sec- tor and make Canadian LNG terminal projects more competitive with those proposed for and currently under construction in Australia and the United States,” Stratas said.

Stratas expects at least three major pipeline projects associated with proposed LNG export facilities to be built and commence operations in the next three to four years, resulting in a total natural gas takeaway capacity of just over 4 Bcf/d.

The industry needs a break for this sector to move forward. Plans for seven LNG import terminals have been canceled or suspended as supply fundamentals shifted. The exception is the Repsol-Irving Oil Canaport regasi- fication terminal, which began operations in 2009 with a capacity of 1.2 Bcf/d.

Kitimat LNG, originally proposed as an import terminal, has lurched forward in development as an export terminal and is expected to initially process 1.3 Bcf/d of shale gas produced in British Columbia. Apache Corp. sold its 50% stake in the project to Adelaide, Australia-based Woodside Petroleum Ltd., along with related upstream acreage in the Horn River and Liard natural gas shale plays. Chevron, the other partner in the project, announced in January that it would cut its global LNG budget by 20% to $8 billion. Kitimat LNG and Shell’s LNG Canada project are not eligible for British Columbia tax incentives, at least not yet, the Vancouver Sun reported.

Demand for NGL

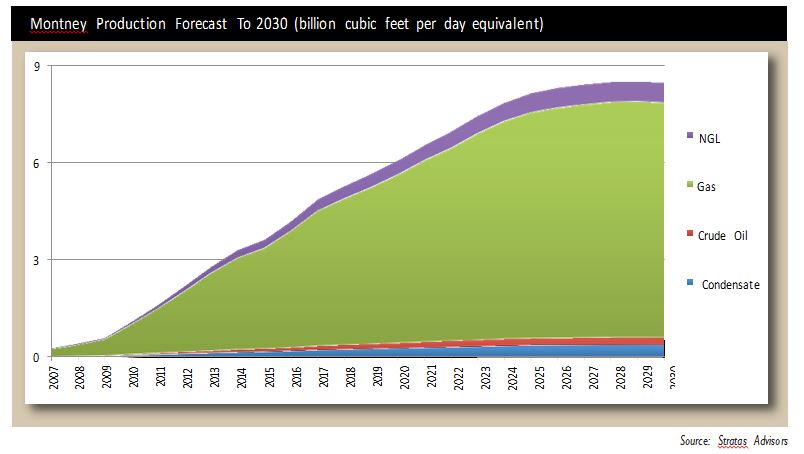

In all, 23 gas liquefaction and export facilities have applied to Canada’s National Energy Board (NEB) for licenses to export gas. It is unlikely that all will be built, especially in this energy commodity environment, and the combined capacity of these plans would total more than 45 Bcf/d, according to a report by Gas Processing Management Inc. (GPMi) and Ziff Energy, a division of Solomon Associates LLC. The WCSB currently produces 14 Bcf/d, so sustained output would need to more than triple.

But the potential from attempting these projects will result in a significant increase in NGL production from the Montney and Duvernay plays, the GPMi/Ziff Energy researchers believe. When combined with existing demand for liquids in Canada and the U.S., they conclude that:

• In producing areas, there will be sig- nificant development of gas-gathering pipelines and new or expanded field processing facilities with NGL recovery; existing facilities will be retrofitted to recover additional liquids in areas with high NGL content;

• Existing NGL facilities will be ex- panded, including gathering, transportation and processing systems (pipelines, fractionation, storage);

• The increased output will create the potential for construction of new facilities;

• There will be increased demand for NGL stemming from the need to increase the heating value of LNG to make it acceptable for export to Asia—this would be done within producing areas, at the inlets to LNG interconnect pipelines or plants or at delivery from tankers (Asian markets require gas to be in the 1,100 Btu per cubic foot (Btu/cf) range and the heat content of LNG ranges from 985 Btu/cf to 1,050 Btu/cf);

• Western Canadian NGL producers will need to find additional markets; and

• Increased production of C5+ from the Montney and Duvernay plays will contribute to the supply-demand balance for C5+ required for oil sands diluents.

NGL development

The GPMi-Ziff Energy team discerned a complex challenge for the midstream in development of NGL in western Canada, noting how industry’s default approach is to focus on a particular project—be it a pipeline, process- ing plant or gathering system—to meet the needs of producers and generate revenue.

“This generally will result in uncoordinated development and potentially increased cycle times, overbuild of capacity and overinvestment of capital,” the researchers wrote. GPMi-Ziff Energy suggested that thought be given to debottlenecking and expansion of existing pipelines, and integrating development to decrease operating expenses and limit capital investment.

Stratas envisions Pembina Pipeline Corp. as playing a key role, particularly its C$220 million (US$176 million) Northeast British Columbia (NEBC) Expansion project.

“The development of Pembina’s NGL infrastructure network in northwest Canada should be the greatest growth driver of pipeline infrastructure for the transmission of NGL over the forecast period [to 2018],” the analysts wrote.

Profitable processing

Three major new natural gas processing projects appeared on western Canada’s horizon in late 2014:

• Birchcliff Energy Ltd.’s Pouce Coupe South plant’s Phase IV expansion will bolster capacity by 60 million cubic feet per day (MMcf/d), or 33%;

• Pembina Pipeline Corp.’s Musreau III expansion will add 100 MMcf/d of natural gas processing capacity and 3,000 bbl/d of NGL extraction; and

• Construction of Keyera Corp.’s Zeta Creek Gas Plant will provide 54 MMcf/d of capacity.

Stratas crunched numbers of projected capacity last December and found an additional 1.54 Bcf/d in incremental gas processing capacity for the province to come online by year-end 2017. The analysts’ latest forecast in late February, which included these three projects, pumped up that projection by 14% for a total additional capacity of just over 1.75 Bcf/d. The new infrastructure will help alleviate constraints for producers in the region.

“In the fourth quarter, several of our facilities, including Rimbey, Strachan, Nordegg River, Simonette, Minnehik Buck Lake, Pembina North and Brazeau North were operating at or close to their effective capacities,” Brad Lock, Keyera’s senior vice presi- dent for gathering and processing, told analysts during the company’s call covering fourth-quarter 2014.

“Overall, gross processing throughput in the fourth quarter was 1.6 Bcf/d, up 10% in the third quarter of 2014, and 22% from the fourth quarter of 2013.” For all of 2014, that translated into a 39% jump in operating margin for Keyera’s gathering and processing division over 2013 for a record C$218 million (US$174.4 million).

Oil sands demands

Keyera also made strides in its liquids business unit, with operating margin leaping 53% to C$189 million (US$150 million) in 2014 over 2013’s results. Growth in demand from oil sands producers led the company to diversify its service offerings, adding two rail and truck terminals in 2014. Another, the Josephburg rail terminal, is expected to be operational by the middle of this year.

“This terminal is a critical piece of infrastructure for our customers, as it will provide additional propane egress from western Canada,” Dean Setoguchi, senior vice president for the liquids unit, told analysts. The conversion of Kinder Morgan Inc.’s Cochin Pipeline from southbound propane to northbound condensate complicated the market in 2014, Setoguchi said, forcing producers to rely more on rail and truck to export to the U.S. Midwest and put more into storage, according to the EIA.

Kinder Morgan reversed Cochin to move abundant U.S. light condensate, produced by the shale plays, to Canada for use as a diluent for ultraheavy oil produced by the Canadian oil sands.

But the need for more storage works for Keyera, too.

To address the continued demand for dealing with storage, we recently completed construction on our fourth brine pond,” Setoguchi said. “Our 13th underground storage cavern is nearing completion and is expected to be in service by mid-2015, with washing of the 14th cavern currently underway. The next phase of our storage capacity expansion is progressing, as we recently completed drilling the well bore for our 15th storage cavern and washing is expected to commence midyear.”

Completed conduits

One of the most significant recent events for western Canadian oil was the completion of Enbridge’s 593-mile, $2.8 billion Flanagan South Pipeline, which is able to move up to 600,000 bbl/d from the Flanagan, Ill., hub to Cushing, Okla.; and Enterprise Product Partners LP’s looped Seaway Pipeline, with 450,000 bbl/d capacity from Cushing to the Jones Creek terminal near Freeport, Texas, on the Gulf Coast.

“Make no mistake about it: Canadian crude is in the game here on the Gulf Coast, and we will compete for space against waterborne imports,” Enbridge President and CEO Al Monaco said during a ceremony in Texas to mark the completion of the system.

“Canadian crude in the Gulf means energy security for North America. And when supply and demand are con- nected with the lowest-cost transportation by pipelines, that can only mean one thing—it’s good for consumers.”

Enbridge isn’t done. The Calgary-based company is in the midst of a C$34 billion (US$27.2 billion) infrastructure investment program.

“With Flanagan South and Seaway Twin now in service and the recent NEB decision on Line 9, we provided our shippers with 1.3 million bbl/d of low-cost access to attractive new markets with another 400,000 bbl/d on track for completion this year,” Monaco told analysts during the company’s conference call in early 2015.

“These are very good accomplishments in a tough permitting and regulatory environment.”

Commodity prices

The stubborn persistence of low energy commodity prices does not appear to worry Enbridge, either.

“We don’t expect that the current oil price environment will have much effect on us at all in the near and medium term and likely little effect in the longer term as well,” Guy Jarvis, president of the company’s liquids pipelines unit told analysts. “In fact, this is actually a conservative portrayal in that we assume three of the four new pipelines go ahead and are in serv- ice by 2020.”

Aux Sable Canada, a joint venture of Enbridge and Calgary-based Veresen Inc., recently completed its Channahon, Ill., NGL Extraction & Fractionation Facilities, about 50 miles southwest of Chicago. Fed by the Alliance Pipeline system, the facility’s capacity of 2.1 Bcf/d and 107,000 bbl/d of NGL products originate in western Canada’s Duvernay play. The company has announced an expansion of the fractionation capacity by an incremental 24,500 bbl/d that is expected to be online in mid-2016.

Recommended Reading

To Dawson: EOG, SM Energy, More Aim to Push Midland Heat Map North

2024-02-22 - SM Energy joined Birch Operations, EOG Resources and Callon Petroleum in applying the newest D&C intel to areas north of Midland and Martin counties.

CEO: Continental Adds Midland Basin Acreage, Explores Woodford, Barnett

2024-04-11 - Continental Resources is adding leases in Midland and Ector counties, Texas, as the private E&P hunts for drilling locations to explore. Continental is also testing deeper Barnett and Woodford intervals across its Permian footprint, CEO Doug Lawler said in an exclusive interview.

TotalEnergies Starts Production at Akpo West Offshore Nigeria

2024-02-07 - Subsea tieback expected to add 14,000 bbl/d of condensate by mid-year, and up to 4 MMcm/d of gas by 2028.

E&P Highlights: Feb. 5, 2024

2024-02-05 - Here’s a roundup of the latest E&P headlines, including an update on Enauta’s Atlanta Phase 1 project.

CNOOC’s Suizhong 36-1/Luda 5-2 Starts Production Offshore China

2024-02-05 - CNOOC plans 118 development wells in the shallow water project in the Bohai Sea — the largest secondary development and adjustment project offshore China.